By:

Simona M Mocuta, Chief Economist

Amy Le, CFA, Investment Strategist

Krishna Bhimavarapu, Economist

Two marquee macro reports this week—payrolls and the CPI—offered mixed signals on the economy. Our call for three Fed cuts this year stands. Mixed data signals continue around the globe.

US: Mixed data should not preclude rate cuts

It is rare that the two marquee macro reports for the US economy—the employment and inflation data—are released in the same week. They were this week, and, at least on the surface, offered divergent signals on the state of the economy and the desired monetary policy path.

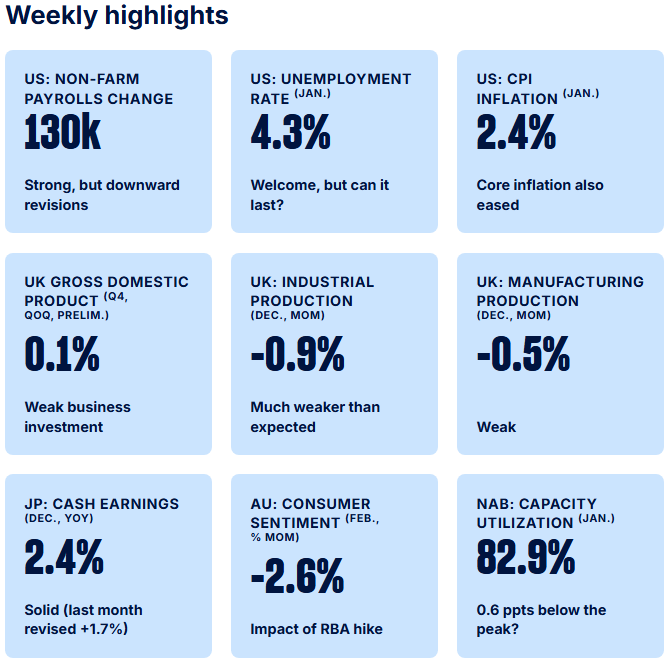

On one hand, the payrolls data was a clear upside surprise, coming in at 130k versus 65k expected. The unemployment rate ticked down a tenth to 4.3%, a five-month low and the underemployment rate dipped sharply to a six-month low of 8.0%. The hours worked and wages rebounded sequentially (MoM) after unusually weak December readings.

But these headline positive surprises were accompanied by yet another set of major downward revisions to the employment trajectory over the prior year, with employment at end-2025 roughly one million lower than prior estimates. To us, this is the bigger story, though we do not want to dismiss the stronger January data out of hand. Time will tell whether a genuine rebound in employment growth is possible, but we are a little suspicious of the big jump in healthcare/social assistance.

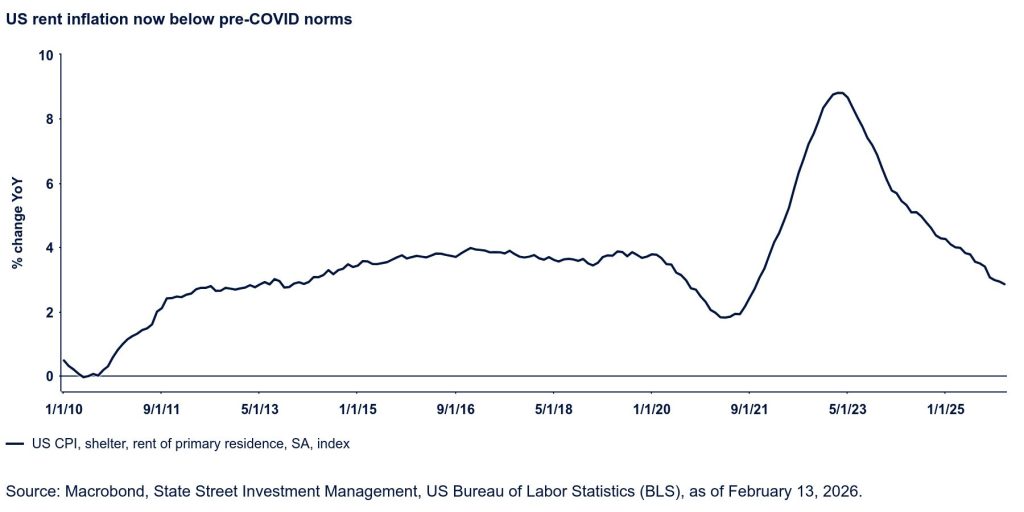

The market reaction to the employment report was, unsurprisingly, hawkish, with 10-year yields moving higher and odds of a June rate cut retreating. That didn’t last long, however. The inflation update on Friday showed fairly tepid price pressures, especially in the important shelter component, so the week ended on a dovish tone. Headline inflation eased three tenths to 2.4% YoY, a tenth more than anticipated; core inflation eased one tenth to 2.5% YoY. For the headline, this was the lowest level since May; for core, since March 2021!

This improvement reflects steady easing in shelter inflation, which more than offsets recent increases in core goods inflation. Given current market indicators of rent inflation, it is reasonable to anticipate further gentle easing in rent inflation over the next few months. Our end-of-year core-PCE forecast sits at 2.3% YoY in Q4, a little below the Fed’s 2.5% projection.

UK: Growth slows at end 2025

The economy recorded a 0.1% expansion in the fourth quarter, resulting in an annual growth rate of 1.3% last year, in line with our projections.

Notably, business investment and construction declined markedly during the last part of the year. The decrease in business investment was influenced largely by fluctuations in car production, which were linked to a significant cyberattack at the end of the third quarter. These factors compounded broader uncertainties preceding the Budget and subdued business confidence. The decline in construction activity underscores the continuing effects of earlier interest rate hikes by the Bank of England.

Looking ahead, our analysis indicates that economic conditions in 2026 may be somewhat less robust than those anticipated for 2025. Real disposable income growth is expected to remain largely stable. Inflation is forecasted to decrease markedly and sustain this lower level throughout the year. Nevertheless, wage growth is experiencing a notable slowdown.

Business confidence remains low, likely limiting investment, but rising lending growth suggests conditions may improve by mid-year. Government spending will be more restrictive compared with 2025. Recent surveys show the labor market is still fragile. We forecast 0.9% GDP growth in 2026.

The latest GDP data likely won’t impact the Bank of England, which has already noted weak Q4 results. If slow job growth and falling wages persist, we expect that rate cuts will happen in March and June.

Australia: Hike jitters

The Reserve Bank of Australia’s (RBA) hike last week and guidance that another remains possible is weighing on consumer sentiment. Consumer sentiment fell for a third consecutive month in February, declining 2.6% MoM to 90.5. While we expected sentiment to weaken, the deterioration was larger than anticipated.

The decline was broad-based. The sharpest falls were in “time to buy a dwelling” (-6.3%) and “time to buy a major household item” (-5.6%), alongside weaker perceptions of family finances (-4.7%) and future economic conditions (-2.5%). Mortgage rate expectations surged 16.1%, with Westpac noting that 80% of consumers now expect mortgage rates to rise over the next year. The survey provider also highlighted that the RBA’s rate hike “dented attitudes” toward purchases and “has put renewed pressure on finances.” The survey highlights clear downside risks to our 2.5% GDP growth forecast for this year.

Household spending data reinforce the mixed outlook. Spending fell 0.4% MoM in December following a stronger increase in November. As a result, Q4 household spending rose 0.9% QoQ. This provides some near-term support to GDP growth, but it is also likely to reinforce the RBA’s hawkish bias.

In contrast, business conditions are showing signs of softening. The NAB Business Survey for January showed conditions easing by 3 points to 7, the lowest level since July 2025. The decline was driven by weaker trading conditions (-6 points), profitability (-3 points), and a modest fall in capacity utilization (-0.2 percentage points). Notably, inflation-related indicators fell to new post-pandemic lows. Labor costs declined 50 basis points to 1.3% QoQ, while final product prices fell 30 basis points to 0.5% QoQ. Retail prices eased 20 basis points to 0.3% QoQ, and purchase costs declined by a similar margin to 1.1% QoQ. Finally, forward orders rose 3 points to +2, but stock of inventory fell 12 pts to -1. The average of the difference in the last three months was negative (as was the case in the last two years), indicating that demand expectations ran ahead of realized demand.

Overall, this week’s data releases underwhelmed expectations. Consumer sentiment has taken a clear hit from the RBA’s rate hike and forward guidance, while business conditions and inflation pressures are easing. Looking ahead to next week, we expect the unemployment rate to rise by 10 basis points to 4.2%.

Originally posted on February 16, 2026 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/nastudios

VIA SHUTTERSTOCK

DISCLOSURES

Marketing Communication

State Street Global Advisors (SSGA) is now State Street Investment Management. Please go to statestreet.com/investment-management for more information.

State Street Global Advisors Worldwide Entities

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of SSGA Economics Team through the period ended February 13 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.