By:

Simona M Mocuta, Chief Economist

Amy Le, CFA, Investment Strategist

Krishna Bhimavarapu, Economist

Softer US payrolls, slowing UK activity, and resilient Japan business sentiment dominated the week. Lower oil prices and easing inflation concerns also reduced Fed hike fears.

US: A reminder and more data questions

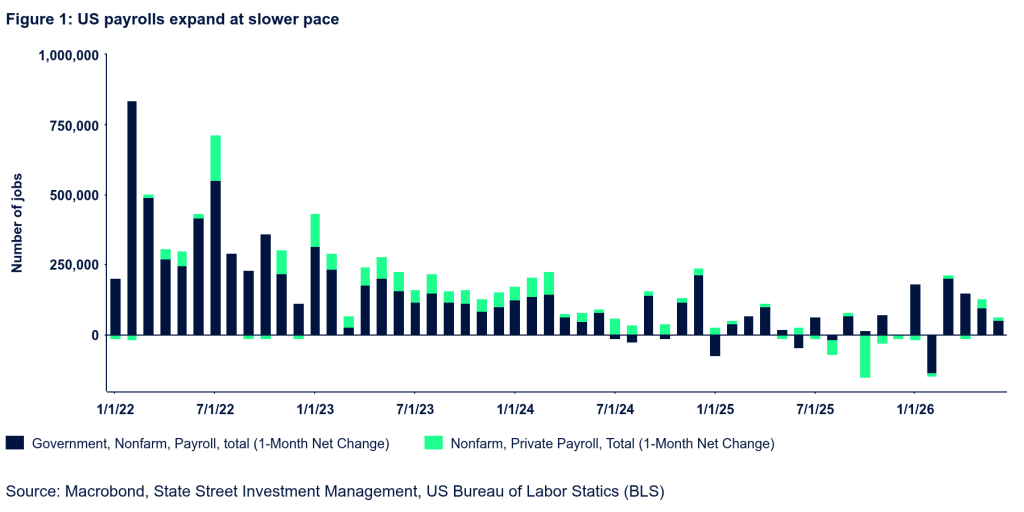

We’ve spent much of the last couple of months highlighting the contradictory signals from different parts of the labor market, arguing that while the narrative of labor market stabilization is well supported, the narrative of a sustained reacceleration was not yet so.

The June employment report demonstrated why. The economy added 57k in June, which was about half the expected number. The bigger caveat, however, was the 74k downward revision to the prior two months. In other words, the level of employment at the end of June was lower than we previously believed it to be at the end of May. Even so, the unemployment rate eased one tenth to 4.2%. This reflected an unusually sharp decline in the labor force participation rate, which retreated three tenths to 61.5%. The participation rate is down a full percentage point since September. The steep retreat in June reflected a 507k plunge in employment (as reported in the household survey) and a 213k plunge in unemployment, lowering the labor force by 720k. This is quite extraordinary and hard to explain. The prime age labor force participation rate plunged by 0.6 percentage points (ppt), the single largest monthly decline since January 1968 (outside of Covid). The suddenness and the magnitude of the move do not come across as credible, so, once again, we’ll need to await further details.

There were only two notable details in June’s sector distribution of job gains. Firstly, there was a 61k decline in leisure and hospitality employment, which makes sense given that surging travel costs likely hampered demand temporarily. It would not be surprising to see a rebound here in coming months. Secondly, the strength in state and local government employment that appeared so stark and so surprising last month has largely faded on account of big downward revisions and a soft print for June itself. This seems reasonable as well. Here, there is little reason to anticipate much of an improvement going forward.

Wage inflation remains contained, with total average hourly earnings inflation down a tenth to 3.4% YoY, the lowest since May 2021. This detail, in particular, should be reassuring to the FOMC. We maintain the recently revised call of a Fed on hold this year (previously we expected two cuts). Market expectations have turned a little less hawkish, but investors still price more than one full hike in 2026.

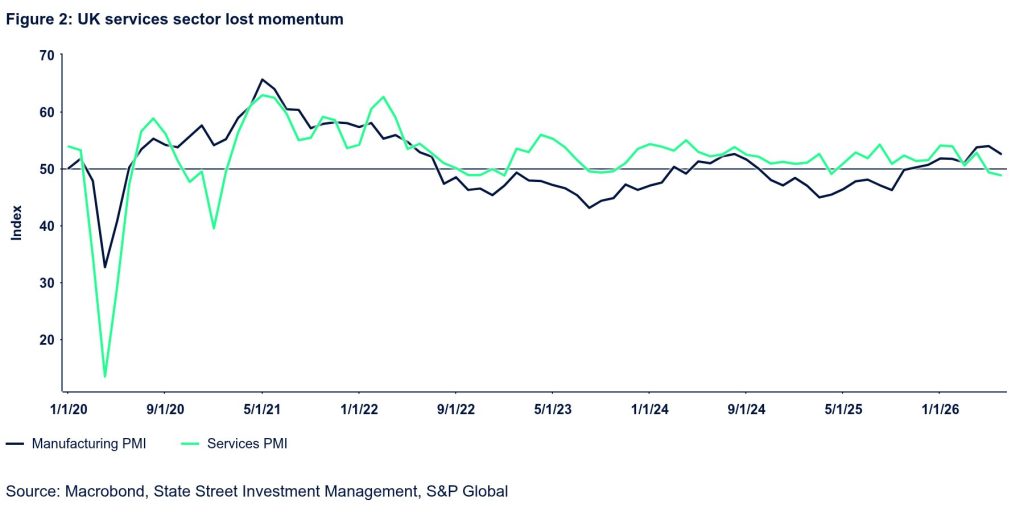

UK: Economy losing steam

The composite PMI indicated a slight downturn in economic activity for June, slipping to 49.3, the weakest reading since April 2025. This decline was largely attributed to reduced momentum within the services sector. Notably, the S&P Global services PMI fell to 48.8 in June from 49.3 in May, as businesses highlighted how rising energy costs were curbing consumer spending and prompting investors to adopt a cautious stance in the face of ongoing geopolitical uncertainty.

After a strong start to the year, the UK economy is now showing signs of losing steam. GDP contracted by 0.1% in April, signaling a slowdown despite the relief of lower energy prices. Looking ahead, growth prospects remain subdued for the remainder of 2026, with household incomes under strain, financial conditions still restrictive, and fiscal policy remaining tight.

Meanwhile, at the ECB’s Sintra Forum, Bailey’s dovish remarks further reduced the likelihood of an imminent rate hike. Although decreasing energy prices are helping to ease input costs and temper price rises, concerns linger regarding possible secondary inflation effects. Against this backdrop, we expect that the BoE’s policy rate will be maintained at 3.75% for the rest of the year, reflecting a cautious approach as the economy navigates ongoing challenges.

Japan: Momentum

The Bank of Japan’s Q2 Tankan Survey reinforced the view that business sentiment remains resilient. The headline all-firms diffusion index held steady at 18, close to its highest level since 1991. Strength was broad-based: the large manufacturers’ index rose five points to 22, its strongest reading in decades, while the large non-manufacturers’ index increased two points to 37, continuing to outperform the manufacturing sector. Small businesses also surprised to the upside, with sentiment jumping five points to 9.

Capital expenditure plans, however, continue to send mixed signals. Among large firms, FY2026 capex intentions were revised up by one percentage point to 11.5%, suggesting investment appetite remains intact. In contrast, small firms cut their spending plans sharply, with their capex estimate falling 3.8 percentage points to -8.3%. This divergence reinforces concerns highlighted in our latest outlook that investment momentum remains heavily concentrated among larger corporates. At the margin, we still expect capital expenditures to resume as geopolitical uncertainty eases more.

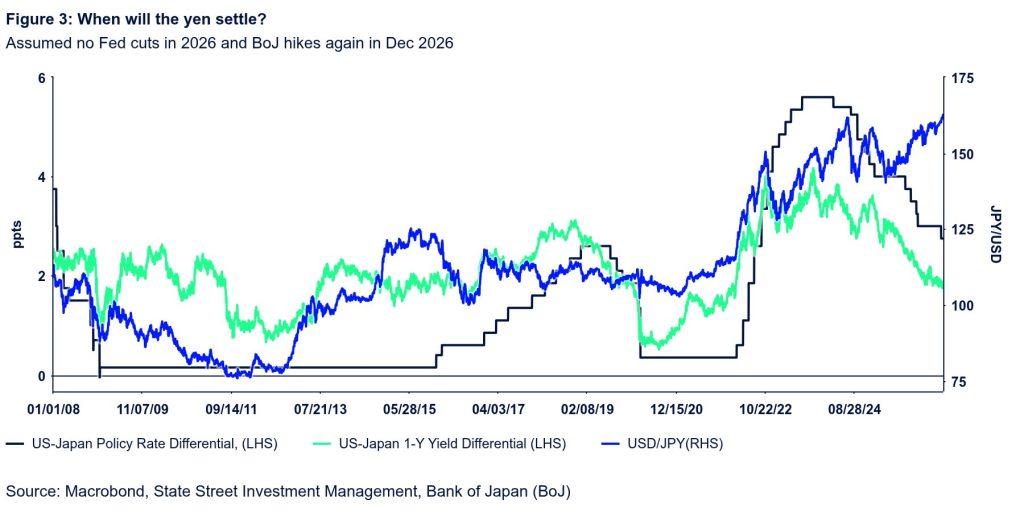

Separately, markets were unsettled by the government’s draft growth strategy released this week. While the language was subtle, the guidance appeared to encourage the BoJ to align monetary policy more closely with the government’s objective of achieving a “strong economy.” Investors interpreted this as a potential challenge to central bank independence, adding further pressure on the yen.

As a result, the currency weakened beyond ¥162 per US dollar, its softest level since the 1980s. Although a slightly weaker-than-expected US payrolls report provided some temporary support, the broader drivers weighing on the yen remain in place and are likely to keep depreciation pressures elevated in the near term.

Originally posted on July 6, 2026 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/Maksim+Labkousky

VIA SHUTTERSTOCK

DISCLOSURES

Marketing Communication

State Street Global Advisors (SSGA) is now State Street Investment Management. Please go to statestreet.com/investment-management for more information.

State Street Global Advisors Worldwide Entities

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

The views expressed in this material are the views of SSGA Economics Team through the period ended July 06, 2026, and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

{kind=link}