By:

Kevin Flanagan, Head of Investment and Fixed Income Strategy

- Treasury markets have rapidly repriced toward a higher-for-longer Fed outlook, with the 10-year Treasury yield climbing to 4.60% and fed funds futures now fully pricing in a rate hike by March 2027 after previously expecting multiple cuts.

- As inflation pressures, stronger labor data and geopolitical risks fuel the “inflation trade,” investors may want to reduce duration exposure and prepare for additional volatility across fixed income markets.

How many headlines can a bond investor handle at one time? Let’s see, at the present time, the money and bond markets have been juggling ongoing Middle East headlines, a return of inflation (both headline & core), better than expected jobs reports, new Treasury coupon auctions, etc., etc.

Or better yet, how would you like to become the new Fed Chair right about now? That’s the situation new Fed Chairman Kevin Warsh finds himself in. Indeed, Warsh now enters the Eccles Building (Fed Headquarters) as the new leader, while also having a former Fed Chair, a.k.a. Jay Powell still sitting on the Federal Open Market Committee (FOMC) as an automatic voting member due to his retained stance as a Fed Governor.

In terms of upcoming monetary policy, as we have written in a series of Warsh-related blogs this year, the new Chairman will follow the data, and at this point in time, that data is pointing to a Fed that appears to be done cutting rates, and is on hold for the rest of 2026.

I still don’t think the Fed is close to a rate hike, but for the upcoming June FOMC meeting, a shift in the language of the policy statement from an easing bias to one of a ‘balanced’ outlook seems to be the most likely scenario. However, the fed funds futures market has now fully priced in a rate hike for March 2027, a remarkable shift from its pre-war status of discounting almost three rate cuts for the same timeframe.

The Inflation Trade

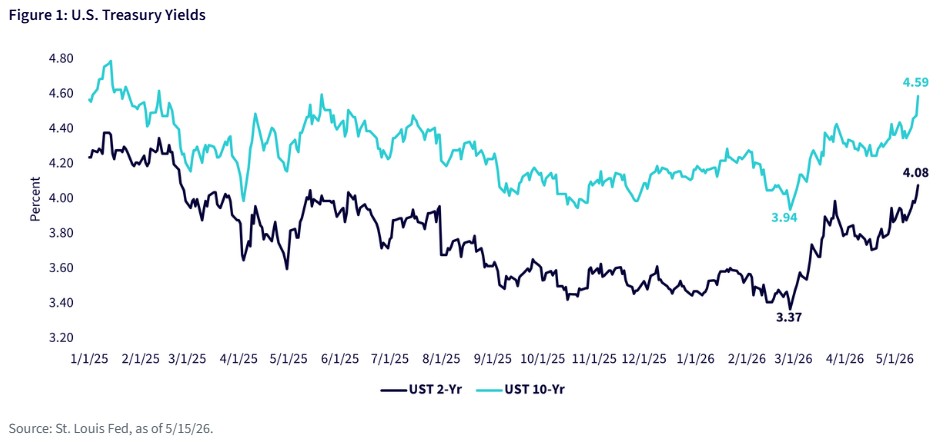

The U.S. Treasury (UST) market has also shifted into a different mindset. Indeed, the ‘inflation trade’ has taken hold, whereby yield levels across the fixed coupon maturity spectrum have risen in a rather visible fashion since the end of February (see graph). Here’s some highlights:

- The UST 10-year yield has increased by about 65 basis points (bps) during this timeframe.

- As of this writing, the yield had jumped to 4.60%, the highest reading since early 2025.

- Technical analysis, such as one-year Fibonacci retracement levels, are being tested, with a breakthrough putting 4.80% potentially in play.

- The UST 2-year yield has surged over 70bp from its pre-war low.

- It has pierced the 4% threshold and is also at its highest reading since early 2025.

- At its current level of 4.08%, the two-year has now also priced in a Fed rate hike.

Solution

So, how can a bond investor combat the ‘inflation trade’? Answer: the time-tested barbell strategy.

Originally posted on May 20, 2026. Read more on WisdomTree blog.

PHOTO CREDIT: https://www.shutterstock.com/g/ungvar

VIA SHUTTERSTOCK

DISCLOSURES:

There are risks associated with investing, including possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

You cannot invest directly in an index.

Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, real estate, currency, fixed income and alternative investments include additional risks. Due to the investment strategy of certain Funds, they may make higher capital gain distributions than other ETFs. Please see prospectus for discussion of risks.