Author: Brad Pappas, Rocky Mountain Humane Investing

Author: Brad Pappas, Rocky Mountain Humane Investing

Covestor model: RHMI Evergreen

The August to October time period was turbulent for markets and assets around the world. What resembled an ordinary market correction took a turn for the worse in August when the U.S. political leadership revealed itself to be incapable of compromise and the vested interests of each party took priority over the needs of the country. Long gone are the days when Tip O’Neal and Ronald Reagan would cut a reasonable deal over drinks and poker. The ensuing political chaos of the debt negotiations caused confidence to take a beating and our leadership doesn’t seem to understand that confidence in the economy can be as important as policy.

I took major steps in August through September to diversify assets and limit equity risk. While stocks were showing initial signs of weakness, the Gold exchange traded fund (GLD), which had been in a flat trading range, made a tremendous leap to $184. Our purchases of GLD in mid-July were primarily in the $155 area, which was the approximate breakout price.

Gold offers an alternative to the major currencies of the world, which are in a race to devalue in an attempt to boost their economies by making their goods cheaper for purchase and make their national debts easier to pay off.

Countries with debt issues that print more dollars in an effort to pay off the debt run the risk of inflation and the after effects of devaluation. But it’s no coincidence that the countries which are able to print money have withstood the shock of the crisis the best, while countries that cannot (Greece, for example) are suffering the most.

I believe the correlation between the price of Gold and deficit spending in the US and the world is very tight, and I intend to hold on to our Gold position for quite a while – or until interest rates on U.S. Treasuries become very attractive.

By September my portfolio had less than 50% exposure to US equities, as my primary concern was for preservation of capital should the European situation completely unravel. I must admit to having very little faith in the world’s political leadership, which contributed to my defensive posture for the past three months.

Meanwhile in the U.S., there was a growing mistrust for the state of the economy and fear was commonplace that we were entering or had already entered into another recession. Just as in 2009, the fears of recession were overblown and the current data does not support the recession case. While there appears little doubt that many countries in Europe are already in a recession, there is a very good chance the U.S. will avoid one within the next six months.

The problem with investing in an attempt to avoid a disaster is that so few truly materialize as expected. The vested interests of the majority usually find a solution to preserve themselves, although there may be quite a few guns pointed at their heads. Investors seeing the potential for collapse with vivid memories of 2008 adjust their risk exposure to reflect the potential for calamity. However in a high majority of the cases the disaster does not materialize. But is it worth taking the precaution? I would still say yes, since there can always be a time later on to invest. The price you pay is lost performance should the event not occur – but that’s secondary to an actual major loss in my opinion.

This is not to say the Euro situation will never devolve. It may devolve over time, but just not a time when everyone is expecting it to. Hence I posted on the RMHI blog (October 13th) that I was becoming very nervous about the high levels of cash we had in client accounts. With headline news consistently negative on virtually a daily basis, combined with a disproportionate percentage of investors betting on continued downside along with reduce risk of a recession, I felt that by mid- October it was appropriate to increase our exposure to U.S. equities.

It’s my firm view that deployment of capital should be based on facts with very little, if any emotion involved. Emotions come naturally to investing but they should always be held at bay. The decision in mid- October to deploy capital was based on the following facts:

1. U.S corporate earnings for 2012 are not in a freefall. Despite all the negative headlines and hysteria whipped up by the media earnings expectations for the S&P 500 for 2012 are barely moving lower and yields of low grade corporate debt have moved just modestly higher. It’s rare to have a bear market for stocks without a sharp decline in corporate earnings. The last time this happened was in 1987 when bond prices were falling sharply. However after the ‘87 crash the market was net positive a year later.

The psychology of the markets and economies frequently resemble a pendulum and at points of extreme it’s generally wise to consider being contrary to popular opinion. Gerald Loeb once said: “Knowing what everyone else knows is not worth knowing.” Experts are frequently wrong, even with mass consensus. I consider equity prices as cheap now as they were in March 2009.

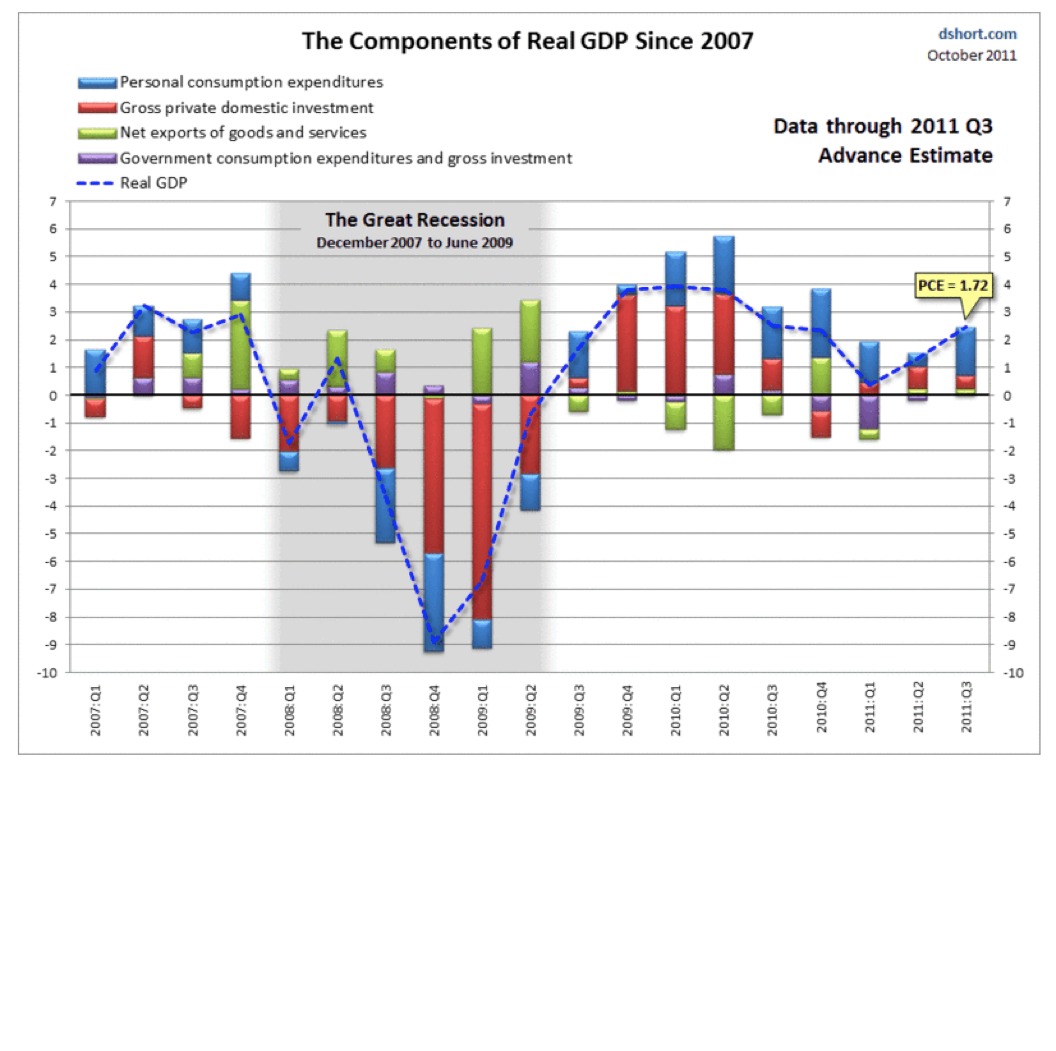

See chart: Components of Real GDP Since 2007 (source: dshort.com)

As the chart details, GDP growth was 2.5% in the last quarter, not a freefall.

2. Market Seasonality: The November to May time period is the most profitable seasonal period for the stock market.

The seasonal aspects of the markets were brought to light decades ago by Yale Hirsch of the Stock Trader’s Almanac. The chart is courtesy of Investech Research and goes back 50 years.

Put another way, since 1950 there have been 15 October to the end of December periods in the third year of a Presidential term. In those 15 years, only two had negative returns in the October/December time period and those two were minimal. The average loss was 2.7% while the average gain was 5.1%. What I find interesting is that normally the 3rd year of a Presidential term is very good with the median gain of 16.3%. Only one year aside from 2011 had a negative return and that was 1987. The return to year end for 1987 was 15.3%, which was the largest return to year end.

Finally, there was the mid-October buying panic. The S&P 500 experienced an 11.4% gain in only 5 trading days, which was very unusual. Since 1950 there have been only 16 other similar buying panics. Of the 16 there was only 1 loss (2001) and 1 break-even (2002), the remaining 14 instances resulted in profits by the end of the year. (Source: Laszlo Birinyi)

3. Investor Sentiment was extremely negative. No surprise here, considering the trailing three months, but that’s to be expected after a significant pullback.

In late September the American Association of Individual Investors polled their members and respondents expecting a higher stock market over the next six months dropped to 25% while those expecting a decline rose to 48%. Both numbers were on par with March 2009 readings.

* * *

It has been a very frustrating year, as our big margin of performance in excess of the S&P 500 for the year has been nil.

If this past year showed any flaws in the model, it was that our hedging strategy (which is based on earnings) did not react in time to the August decline. The August decline was primarily caused by a lack of confidence created by the budget impasse between Republicans and Democrats.

One last thought: I receive many calls from potential investors who are wary of investing but admit to the need to do something with their money other than earning 0% interest. So, when is the right time to invest in our current environment?

Almost three months ago the market reached a point (only to be known in hindsight) of maximum downside momentum. Since that point in time, we’ve gradually moved higher, and those investors with the steadiest of nerves who were willing to reject the potential for European economic collapse have been paid the biggest rewards since risk of this collapse have eased.

Next are the investors who believe that the current recession fears are exaggerated, which is more or less where I am as an investment advisor. Our purchases have been made after the European collapse fears have eased, yet before thoughts of a slow growth economy and no recession have become commonplace.

But if you want even more certainty, then I really have no answers for you other than you will likely be buying near a market top. You will be buying when prices are even higher and reward is even less. If you want perfection – a.k.a. no risk, no potential for Euro default or US recession – then expect to buy at the top. This will be when investor confidence is at an extreme and the best investors will be selling or cutting back positions.

I believe the S&P 500 has the potential to run another 7% to 10%, or back to the highs of last summer by early 2012, perhaps February. 1400 on the S&P 500 would still only be 13 times 2012 earnings of $105 (the current estimate is $108). As a benchmark, the 50 year average for the S&P 500 around 15 times current year earnings, hence equities are pretty cheap right now.

Investors must learn to balance the need for return and the compatible degree of risk and eliminate the “I’ll invest when the world is not quite so insane.” If you consider that the world is generally insane, at least in part, virtually all the time you’ll have no perfect moment. Waiting for no risk is a surefire way to find yourself near a market top, when the next issue for markets to contend with arises.

And there always is a new issue.

All the best to everyone,

Brad Pappas

{kind=link}

{kind=link}