By: Jose Torres, Senior Economist

Markets are rebounding following last Friday’s turbulence as Wall Street looks to Fed rate cuts for enthusiasm ahead of critical economic data later this week. Participants anticipate around 75 basis points of reductions this year, with this month’s meeting potentially featuring a super-sized 50, especially if tomorrow’s benchmark revisions for nonfarm payrolls shaves a million workers off the count. Meanwhile, significant PPI and CPI inflation figures will be released on Wednesday and Thursday. Both publications are poised to influence the central bank’s pace down the monetary policy stairs. A heavy subtraction from the worker roster alongside a downside miss on the CPI is likely to raise the odds of a half-percent to a coin-flip. The increased prospects of financial accommodation amidst expanding economic conditions have stoked bullishness among investors that are scooping up stocks in all the major benchmarks and in most of the offensive sectors. Treasuries are additionally catching bids as the yield curve descends in bull flattening fashion led by the long end. The commodity complex is advancing ex lumber while bitcoins and forecast contracts also attract buyers. Conversely, the greenback is retreating on lighter domestic borrowing costs, and volatility protection instruments are experiencing weaker demand.

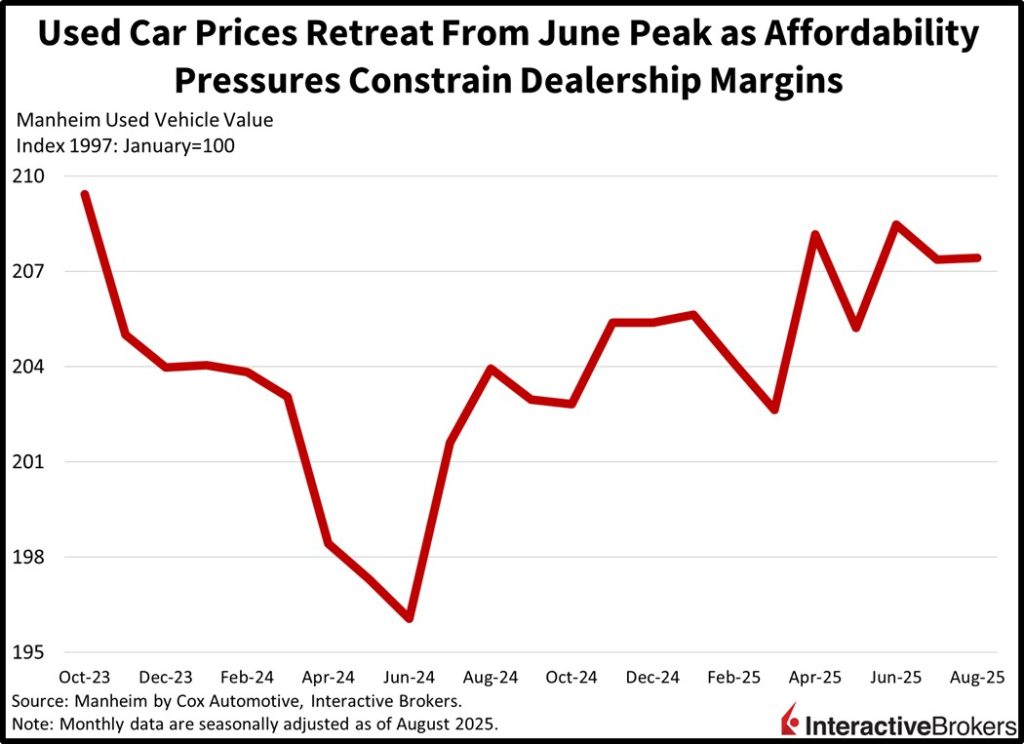

Used Vehicle Price Gains Ease

This morning’s economic calendar was quiet, but Treasuries and inflation expectations received an assist from decelerating automobile prices. Today’s update to the Manheim Used-Vehicle Value Index reflected flat charges on a month-over-month (m/m) basis amidst a 1.7% year-over-year (y/y) cost increase. August’s results compare to July’s 0.5% m/m decline and 2.9% y/y climb. Across categories, EVs, luxury and SUVs saw costs advance 4.6%, 2.3% and 1.3% y/y, while the compact and mid-size segments experienced retreats of 3.5% and 2%. Sales were strong last month; however, affordability pressures amongst consumers driven by elevated loan rates constrained dealership margins.

Payroll Revision and Price Indices Will Be Critical this Week

With a pivotal week of data and a critical interest rate decision in only nine days, we are anxiously awaiting updates on employment while the Bureau of Labor Statistics and the Federal Reserve face unprecedented scrutiny. A heavy downward adjustment to total nonfarm payrolls, which is anticipated, would strengthen the argument that the central bank has been far too late in reducing its benchmark, since hiring levels have been much softer than we all expected. Meanwhile, the White House is almost certainly not going to remain quiet against such a potential backdrop and will probably raise its pressure on the monetary authority to ease financial conditions. But the Producer and Consumer Price Indices (PPI & CPI) are also going to hold weight, although job market health is currently the priority. And as we encounter a plethora of important economic data, bond vigilantes and fixed-income investors alike will have their views heard loud and clear as the Treasury gears up for offerings of 3-, 10- and 30-year notes and bonds from Tuesday to Thursday. Fed independence, deficits, inflation expectations and growth prospects will be top of mind for auction participants as we progress through a few eventful trading sessions.

International Roundup

China’s Trade Surplus Grows

China’s export growth rate in August fell more than 50% y/y, but imports also weakened, and the country’s trade surplus grew m/m. In August, the value of products shipped abroad exceeded the total price tag of items purchased from foreign providers by $103.3 billion. That was up from $98.2 billion in July, and it surpassed the economist consensus estimate of $99.4 billion. Also last month, products sold to foreign markets were 4.4% higher than in the year ago period, a noticeable deceleration from the 7.2% y/y growth rate in July. Economists expected a 5% jump. Meanwhile, imports grew 1.3%, considerably below the 3% estimate and July’s 4.1% rate.

Also in August, a global shift in the country’s trading continued following President Donald Trump’s efforts to accelerate the trend of onshoring manufacturing by implementing tariffs. Exports to the US sank 33% m/m while imports from the world’s largest economy contracted 16%. Conversely, the value of shipments for Southeast Asia customers and the European Union grew approximately 23% and 10%, respectively.

Economic Anxiety Weighs On European Investors

Anxieties about the overall economy caused investor sentiment among capital market participants in the eurozone to drop with the September Sentix Investor Confidence index moving from -3.7 to -9.2, considerably worse than the -2.2 anticipated by the economist consensus.

Views for both the coming months and current conditions weakened, falling from 6 and -13 to 0.8 and -18.8. The weakness was particularly acute in Germany, the eurozone’s largest economy, with a 9.4 points decline to –22.1.

Japan PM Steps Down

Japan Prime Minister Shigeru Ishiba has resigned less than one-year after accepting the leadership role. His support weakened after his party, the Liberal Democratic Party, had disappointing results in a July election after having dominated politics for many years. In resigning, Ishiba said he made the decision to avoid dividing his party. The resignation comes shortly after Japan finalized an agreement with the US that involves the western trading partner imposing a 15% import levy on the country’s products. Ishiba will remain in the position until his party selects a new leader.

Sentiment Regarding Japan’s Economic Improves

Japan’s survey of sentiment among services providers, such as barbers, restaurants, and taxi drivers, depicted improving conditions in July.

The Economy Watchers Current Index climbed from 45.2 in June to 46.7, exceeding the economist consensus estimate of 45.6. It was the highest result since the February 10 print of 48.6. In another matter, the total value of outstanding loans from Japan’s bank increased 3.6% y/y in August. Economists expected the rate of increase to remain unchanged from July’s 3.2%.

Originally posted on September 8, 2025 on Traders’ Insight blog

PHOTO CREDIT: https://www.shutterstock.com/g/Rodworksgh

VIA SHUTTERSTOCK

DISCLOSURES

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}

{kind=link}