By: Scott Helfstein

The progression from one economic era to the next usually brings a healthy mix of excitement and opportunity along with uncertainty and risk.1 New industries emerge, different market leaders rise, and “unknown unknowns” multiply. As the Information Age morphs into the Automation Age, some market truisms that pass as common knowledge may not apply, requiring a keen perspective on how elements from different eras fit together to hint at what is to come.

The Information Age refers to a period that started in the mid-1990s, when better access to information spurred new business models and led to greater efficiencies, but people still made the decisions and completed tasks. Over time, though, it seems as though more advanced robotics and AI technologies could one day complete manual and cognitive tasks with minimal or no human support.

And these are the early days of that transition. Not everything will change, but innovation in automation may well touch every corner of the economy, and potentially drive improved profitability that propels market valuations higher. Automation is also likely to bring new efficiencies to industries that were not primary beneficiaries of the Information Age.

Key Takeaways

- New economic eras are usually preceded by turbulent innovation booms that require meaningful and risky investments. Eventually, these investments typically result in greater capital efficiency and new business models.

- The Information Age changed personal and commercial interaction forever, but the benefits of an increasingly networked world were concentrated.

- Conversely, automation can drive meaningful improvements in profitability across a broad set of industries.

- The recent margin expansion in large caps may just be the beginning of an extended cycle that drives valuations higher as companies refashion themselves through automation.

Innovation Booms in the Modern Economic Era

We define an innovation boom as a period where U.S. research and development (R&D) spending growth was above trend for multiple years. Since 1960, there have been three such periods.2 The first coincided with industrial adoption of the mainframe computer in the 1960s, the second was the rollout of the PC in the mid-1980s, and the third was the commercial use of the internet in the late 1990s.

In each of these periods, corporate investment increased sharply but capital efficiency based on incremental net income per dollar of capital expenditure declined.3 In other words, companies committed capital to adopt new technologies, but they didn’t realize the benefits immediately. The returns came in the decades that followed as companies began to generate greater income per dollar of capex. Each innovation boom generated a meaningful, and in most cases, lasting improvement in capital efficiency. The Information Age delivered that grandest improvement of the modern economic era.

Au Revoir, Information Age, Thanks for the Data

If there is one year that proved pivotal to launching the Information Age, many would point to 1995. Intensifying competition shortened the semiconductor upgrade cycle to two years from three, reducing prices and increasing demand.4 From 1990 to 1995, computer hardware prices declined 16% while sales increased by 22%. From 1996 to 2000, prices fell by an additional 32%, but output made up for it growing by 39%. Software prices declined modestly, but sales growth nearly doubled from 12% to 21% in the same period. The internet also reached a milestone that year as the server count crossed 50,000.5

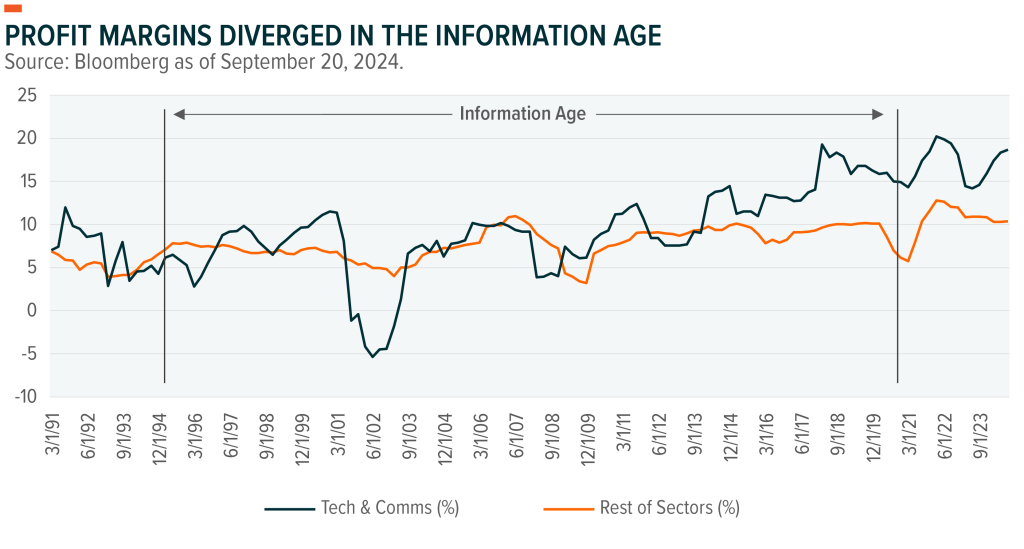

Internet evangelicals predicted that the internet would change everything, and in time it did, but the abundance of information presented a problem.6 Finding relevant information was difficult in the early days. Platforms for accessing, searching, creating, and sharing content became more important than ever. The Netscape and IE browsers, Google search, the Microsoft suite, and then Facebook’s user pages became the toll-takers of the information economy. Other companies adopted the technology to improve processes and drive sales through customer engagement, but the Tech and Communications sectors provided the essential access and tools. Except for the dotcom bust, the profit margins in those sectors outpaced companies across the rest of the economy from 1995 onward.7

The Tech and Communications sectors had an important force working in their favor: network effects.8 Typically, producing more goods, or increasing supply, drives down price, which happened to the semiconductor industry in the 1990s as capacity improved. The opposite was true for the major Tech and Communications companies.9 Like the telephone network, the more people that used the internet, a content platform, or a sharing site, the more valuable the service became. Also, these services could add additional customers at very low incremental costs.

So, prices were sticky while the costs of adding another customer or supplying additional services were small. The indexed growth rate of income relative sales for Tech and Communications sectors grew much faster than the rest of the economy, resulting in today’s mega-cap tech companies and current market concentration.10

Aside from improved profitability across much of the economy, the Information Age dawned asset-light business models through smartphones, gaming, social media, streaming, and ridesharing. With so many tools and access to so many customers, companies could scale with lower start-up costs and less infrastructure.11 Capital expenditure slowed meaningfully in the aughts and teens as the returns to capital investment declined, but that trend reversed in 2020. Income growth relative to sales slowed for the Tech and Communications sectors, but other sectors broke out of a 25-year hibernation and began operating more efficiently.

Hail to the Automation Age, We’re Ready to Get Schooled

Ultimately, the beginning of the Automation Age may well have been 2020, hastened by the pandemic and related effects, among other factors. COVID forced companies to invest in technologies that helped operate safely and more efficiently given labor uncertainty, input shortages, price increases, and supply chain challenges.12 Companies began using algorithms to optimize systems and incorporated robotics where it made sense. Meanwhile, the cost and constraints of implementing these technologies declined.

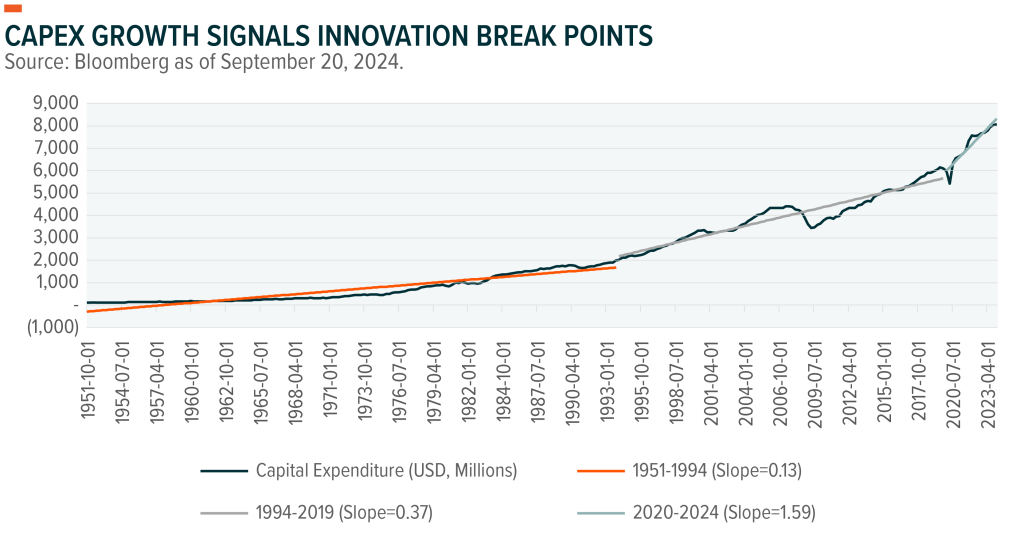

Discontinuous jumps in capital expenditure help pinpoint periods of transition. For example, corporate investment surged in 1995, with average U.S. capital expenditure tripling from of $130 million per quarter to $370 million.13 Years later, pandemic challenges and new productive, cost-effective technologies produced the biggest surge in capital expenditure growth since 1990, growing by 10% for 10 straight quarters from 2020 through 2023. This surge in activity produced another inflection point in 2020 with capital expenditure growth quadrupling to $1.59 billion.

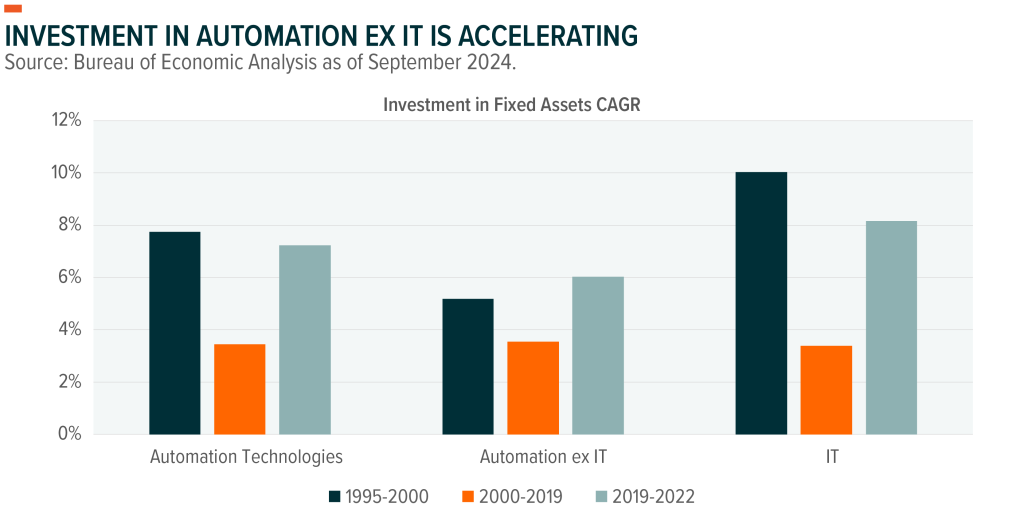

Spending on automation technologies (including IT) surged from 1995 to 2000, when the compounded annual growth rate reached almost 8%.14 That number dropped meaningfully over the next 20 years, with investment growing only 4% annually. A resurgence began in 2020, with annual spending accelerating to 7% through Q2 2024. IT investment grew at almost 10% from 1995 to 2000, meaningfully faster than automation in goods and services. That relationship has now reversed. IT spend grew faster than automation the past four years but remains below the 1990s peak. Automation ex IT investment, however, is hitting a new high.15 IT spending is critical to automation, especially considering AI adoption, but pure automation investment growth is notable.

Automation’s benefits are likely to be distributed more broadly across the economy. The companies that struggled to improve profit margins from 2014 to 2019 are now leading the way.16 For example, goods providers like Consumer Durables & Apparel along with Household & Personal Care Products are gaining efficacy by automating physical tasks through robotics and experimenting with AI platforms that allow users to try products virtually. Service providers, like the Insurance and Commercial & Professional Services, can improve margins by automating cognitive tasks with algorithms and AI. Leadership in margin expansion has almost flipped in only four years, likely indicating rapid adoption of the new technologies in unexpected places.

Effective capital deployment is likely a critical differentiator as companies explore ways to integrate AI and robotics. An arms race is underway, and markets are taking note. Prior to the recent capital expenditure blitz, valuations seemed relatively agnostic to returns on invested capital (ROIC), but current data signals a potential sea change.17 Companies that are delivering higher ROIC are, on average, commanding higher valuations. In 2019, many of the cloud and service tech platforms were investing significant capital but weren’t generating tangible returns. A byproduct of the market selloffs in 2022 has been greater capital discipline. Growth companies are more profitable than ever before, while value company capital expenditure has simultaneously reached record levels.18

Preparing for the Automation Revolution

John Deere is synonymous with tractors and one of the leading companies in both agriculture and construction equipment. But what many investors may not know, is that Deere is arguably the leading autonomous vehicle company. Self-driving tractors operate across the U.S. agricultural territories, seeding, tilling, sampling, and harvesting 24–7. Supporting these efforts is a fleet of drones that take scans of the crops to determine whether they are at optimal yield. Tying these systems together is a network of proprietary satellites.19 That begs the question whether Deere is a tractor company or a technology that happens to make tractors.

A company like Deere offers a glimpse of the economic future. Industries and companies that seem removed from innovation and technology are embracing a new reality: adapt or die. For companies that can improve profitability by successfully implementing new tools and processes, higher valuations in the coming years are possible, which could propel market values higher as businesses finds ways to generate cash more efficiently.20

The adoption of AI and automation technology will not be a linear process. The exchange of one era for another is rarely smooth, with unforeseen obstacles likely.21 Investment in technology stalled after the mainframe rollout in the 1960s because of the hyper inflation of the 1970s. The Information Age stumbled when expectations ran ahead of reality and the dotcom bubble burst in 2000, sapping technology investment for much of the decade. Eventually, innovation won out.

Three categories are likely to monetize automation technology over different time horizons:

- Hardware

- Software

- Adopters

We expect hardware companies to realize the benefits of the Automation Age first, as they provide the systems on which automation is built. The success of semiconductor companies like Nvidia and the mega-cap companies’ investments in data centers to become the hyperscalers of the next era are the prime early examples.22

Beyond semiconductors, robotics manufacturers have a unique opportunity as the conduits to automate physical activities. For years, most industrial robots were caged up in auto plants and then gradually worked their way into logistics and distribution centers. Now, robots are turning up in operating rooms, on construction sites, and in restaurants.23

While investment in data centers has surged, there is still much more development ahead. Data storage and processing needs are expected to more than double from 17 gigawatts (GW) in 2022 to 35 GW in 2030.24 Machines will produce most of the storable data in the form of output, such as AI generated answers or pictures as well as logs from robots and production systems.

Internet of Things (IoT) devices are another hardware component that could monetize on increased automation. These companies help to connect hardware systems through wiring, circuitry, and wireless technology while also providing the sensors that help translate the physical world into machine readable data.25 The hardware buildout can also benefit commodities such as copper, which is critical to wiring facilities.

After hardware, we expect software and service providers to monetize automation and AI, including AI as a service, which offers tremendous growth opportunities. Currently, most of the publicly available AI systems deliver a conversational experience through breadth rather than depth of intelligence, opening the door to specialized services in fields that require greater complexity and accuracy.26 Platforms that focus on servicing different corporate departments, such as sales, finance, or HR, are likely to emerge. While many of the tools under development are not ready to act on insights, they can help inform decision-makers, which could prove quite profitable over time as the business models take shape.

The third monetization category is the one that John Deere falls into. The adopters that leverage new technology to lower costs and generate new sources of revenue may ultimately be the biggest beneficiaries of the automation revolution. The industry group profit margin expansion analysis above showed how this shift may be manifesting in areas that investors haven’t thought about.

In modern times, industries like construction, infrastructure, agriculture, and materials have not necessarily been viewed as hotbeds of innovation, with people and mature machinery working side by side in largely unchanged roles for generations now. Human-robot collaboration may not change at the core, but the range of tasks machines can carry out is expanding, which could lead to faster, safer, and cheaper outputs while freeing workers to engage more complicated, knowledge-based activities. Construction robots, for example, can excavate, weld, and lay brick.27 Engineering firms have long used software to aid design. AI can not only help them build more efficient structures but can now also help develop new materials that reduce costs and improve structural integrity.28

Healthcare is likely to benefit from greater automation. Already, image recognition software used in cancer detection can identify malignant cell growth months before a human could spot a problem.29 AI has mapped 6 million protein structures in just three years, a significant improvement over prior research approaches.30 Automation technologies can drive efficiency in every area from hospital management to drug discovery and surgical outcomes to preventative care. The healthcare space is heavily regulated, so there will likely be a lag in implementation, but the opportunities are significant.

Lastly, the defense industry is a potential rapid adopter of new automation technologies. Large equipment platforms like carriers, tanks, bombers, and missile systems traditionally capture most of the defense spending, but there are early examples of change. The conflict in Ukraine has been dubbed the first drone war, and tech companies have flocked into the war zone to test new AI capabilities.31 The U.S. Department of Defense has supported ongoing efforts to identify off-the-shelf and small-scale platforms like aerial or terrestrial drones that could be deployed at scale.32 This transformation will be a long-term effort, but with increased global military competition, the defense industry is likely to remain on the cutting edge of automation.

Originally posted on October 1, 2024 on Global X blog

PHOTO CREDIT: https://www.shutterstock.com/g/PopTika

VIA SHUTTERSTOCK

Footnotes

1. Atkinson, Robert D. (2005). The Past and Future of America’s Economy: Long Waves of Innovation that Power Cycles of Growth. Edward Elgar Publishing.

2. National Center for Science and Engineering Statistics. U.S. gross domestic product and R&D. Retrieved on September 25, 2024. https://ncses.nsf.gov/data-collections/national-patterns/2021-2022#data.

3. Global X analysis with information derived from: Bloomberg L.P. (n.d.) [Data set]. Retrieved on September 25, 2024.

4. Jorgenson, D. W. (Fall 2001). U.S. Economic Growth in the Information Age. Issues in Science and Technology. https://issues.org/jorgenson/.

5. National Academies Press. (2001). Physics in a New Era. https://nap.nationalacademies.org/read/10118/chapter/12#133

6. Elon University. (2024). Brief Biographies of Early ’90s People. Imaging the Internet: A History and Forecast. https://www.elon.edu/u/imagining/time-capsule/early-90s/brief-biographies/.

7. Global X analysis with information derived from: Bloomberg L.P. (n.d.) [Data set]. Retrieved on September 25, 2024.

8. Katz, M.L. and Shapiro, C. (1994). Systems competition and network effects. Vol. 8, No. 4. https://pubs.aeaweb.org/doi/pdf/10.1257%2Fjep.8.2.93.

9. Global X analysis with information derived from: Bloomberg L.P. (n.d.) [Data set]. Retrieved on September 25, 2024.

10. Ibid.

11. Ibid.

12. Nostrand, E. V. (2024, June 12). U.S. Business Investment in the Post-COVID Expansion. U.S. Department of the Treasury. https://home.treasury.gov/news/featured-stories/us-business-investment-in-the-post-covid-expansion.

13. FRED Economic Data. All Sectors; Total Capital Expenditures, Transactions. St. Louis Federal Reserve. Retrieved on September 25, 2024. https://fred.stlouisfed.org/series/BOGZ1FA895050005Q.

14. Bureau of Economic Analysis. (2023, November 3). Investment in Private Fixed Assets, Equipment, Structures, and Intellectual Property Products by Type. https://www.bea.gov/itable/fixed-assets.

15. Ibid.

16. Global X analysis with information derived from: Bloomberg L.P. (n.d.) [Data set]. Retrieved on September 25, 2024.

17. Ibid.

18. Ibid.

19. Mody, S. (2023, January 3). Why Deere thinks satellites are the next big technology to invest in. CNBC. https://www.cnbc.com/2023/01/03/why-john-deere-is-looking-for-a-satellite-partner.html.

20. Helfstein, S. (2024, June 18). Inflection Points at Mid-Year: Favorable Winds, Choppy Seas. Global X. https://www.globalxetfs.com/inflection-points-at-mid-year-favorable-winds-choppy-seas/.

21. Atkinson, Robert D. (2005). The Past and Future of America’s Economy: Long Waves of Innovation that Power Cycles of Growth. Edward Elgar Publishing.

22. Tsoneva, T. and Affleck, J. (2024, July 17). Decoding Data Centers: Opportunities, risks and investment strategies. CBRE. https://www.cbreim.com/insights/articles/decoding-data-centers#:~:text=Hyperscale%3A%20These%20high%20capacity%20data,well%20as%20their%20pricing%20demands..

23. Grandey, A. A. and Morris, K. (2023, March 22). Robots Are Changing the Face of Customer Service. Harvard Business Review. https://hbr.org/2023/03/robots-are-changing-the-face-of-customer-service.

24. McKinsey & Co. (2024, September 17). How data centers and the energy sector can sate AI’s hunger for power. https://www.mckinsey.com/industries/private-capital/our-insights/how-data-centers-and-the-energy-sector-can-sate-ais-hunger-for-power#. Orcutt, M. (2013, January 9). Humans Generate Most of the World’s Data, but Machines Are Catching Up. MIT Technology Review. https://www.technologyreview.com/2013/01/09/180578/consumers-generate-most-of-the-worlds-data-but-machines-are-catching-up/#:~:text=Uncategorized-,Humans%20Generate%20Most%20of%20the%20World’s%20Data%2C%20but%20Machines%20Are,quickly%20enlarge%20it%20even%20further.

25. Vena, M. (2024, May 9). The Internet Of Things Market Grows Up. Forbes. https://www.forbes.com/councils/forbestechcouncil/2024/05/09/the-internet-of-things-market-grows-up/.

26. Nature. (2024, March 6). Editorial: Why scientists trust AI too much – and what to do about it. Vol. 627. https://www.nature.com/articles/d41586-024-00639-y. Heffernan, D. (2024, September 26). Marr, B. (2024, May 20). The Crucial Difference Between AI And AGI. Forbes. https://www.forbes.com/sites/bernardmarr/2024/05/20/the-crucial-difference-between-ai-and-agi/.

27. Cemex Ventures. (2024, February 5). How construction robotics is going to change the industry forever. https://www.cemexventures.com/how-construction-robotics-is-going-to-change-the-industry-forever/

28. Wang, X. Q. et al. (2023, June 7). Artificial-intelligence-led revolution of construction materials: From molecules to Industry 4.0. Matter. Vol. 6, No. 6. https://www.sciencedirect.com/science/article/pii/S2590238523002023.

29. Kleinman, Z. (2024, March 20). NHS AI test spots tiny cancers missed by doctors. BBC News. https://www.bbc.com/news/technology-68607059. Boyle, P. (2024, March 28). Is it cancer? Artificial intelligence helps doctors get a clearer picture. AAMC. https://www.aamc.org/news/it-cancer-artificial-intelligence-helps-doctors-get-clearer-picture.

30. Service, R. F. (2024, May 8). Powerful new AI software maps virtually any protein interaction in minutes. Science. https://www.science.org/content/article/powerful-new-ai-software-maps-virtually-any-protein-interaction-minutes.

31. Cropsey, S. (2024, March 14). Drone Warfare in Ukraine: Historical Context and Implications for the Future. Hoover Institution. https://www.hoover.org/research/drone-warfare-ukraine-historical-context-and-implications-future#:~:text=The%20Ukraine%20War%20has%20been,the%20future%20of%20military%20power.

32. Albon, C. (2024, August 16). Defense Science Board calls for greater commercial space tech adoption. DefenseNews. https://www.defensenews.com/space/2024/08/16/defense-science-board-calls-for-greater-commercial-space-tech-adoption/. Hacker, T. ( 2024, March 6). How the Army Can Close Its Dangerous-And Growing-Small Drone Gap. The Modern War Institute at West Point. https://mwi.westpoint.edu/how-the-us-army-can-close-its-dangerous-and-growing-small-drone-gap/.

DISCLOSURES:

Information provided by Global X Management Company LLC.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information is not intended to be individual or personalized investment advice and should not be used for trading purposes. Please consult a financial advisor or tax professional for more information regarding your investment and/or tax situation.

Investing involves risk, including the possible loss of principal. Diversification does not ensure a profit or guarantee against a loss. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles, or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments may be subject to higher volatility. There are additional risks associated with investing in Gold and the Gold exploration industry.