The global P&C side of the insurance industry has reported a significant boost in premiums, and the growing calls to insure climate-related risk are partly to blame. The resulting jump in insurance costs for policyholders is an issue that lawmakers are taking steps to address.

By: Vasiliki Farmaki, CFA, OTHR, Equity Research Analyst and Esther Baroudy, CFA, Portfolio Manager

Lawmakers may need to take further actions as extreme weather events are expected to occur with greater intensity. The rise in insurance costs is a problem with knock-on effects across real estate, banking, and other industries.

Girding for Stronger Storms

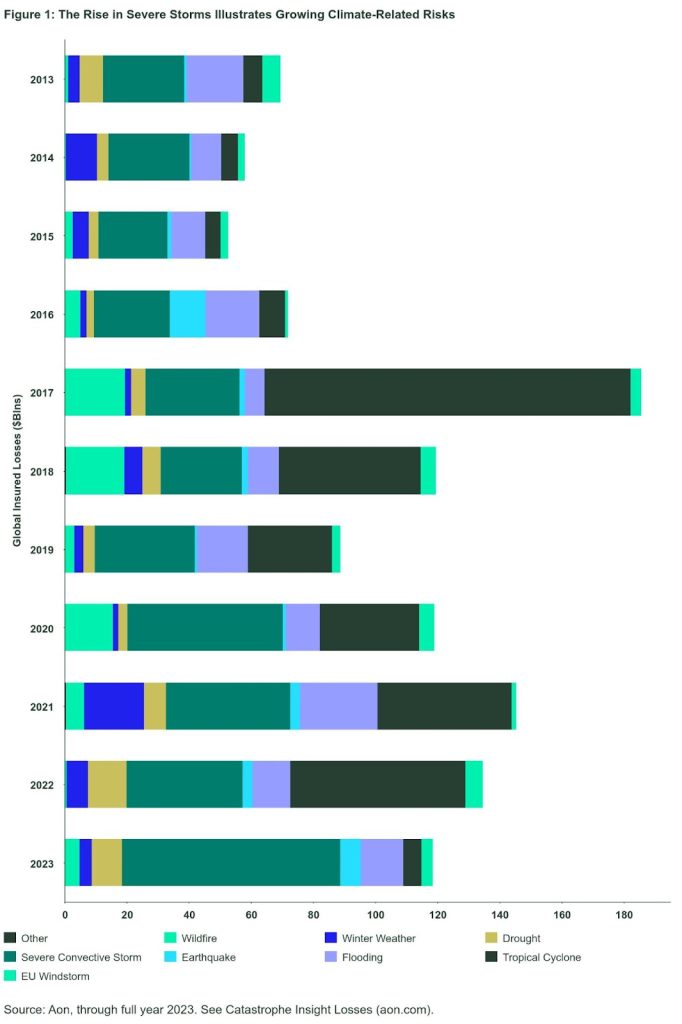

Extreme weather events continue to increase in frequency and severity, reflecting changes in climate over the last two decades. As a result, the insurance industry has experienced a rise in catastrophe losses. In 2023, 28 weather and climate disasters with losses exceeding $1 billion each affected the US, with a combined total cost of $93 billion. Only one other year (2017) has had more billion-dollar disasters in the first six months (Figure 1).1

- Climate experts are forecasting a further uptick in severe weather events. Munich Re climate research has forecast approximately 23 named cyclones in the tropical North Atlantic for the 2024 season. This is significantly higher than the long-term average of 12 named storms.2

- Zurich Insurance has ranked extreme weather events as the top global risk (ranked by severity) in the next decade.

Markets Becoming Uninsurable

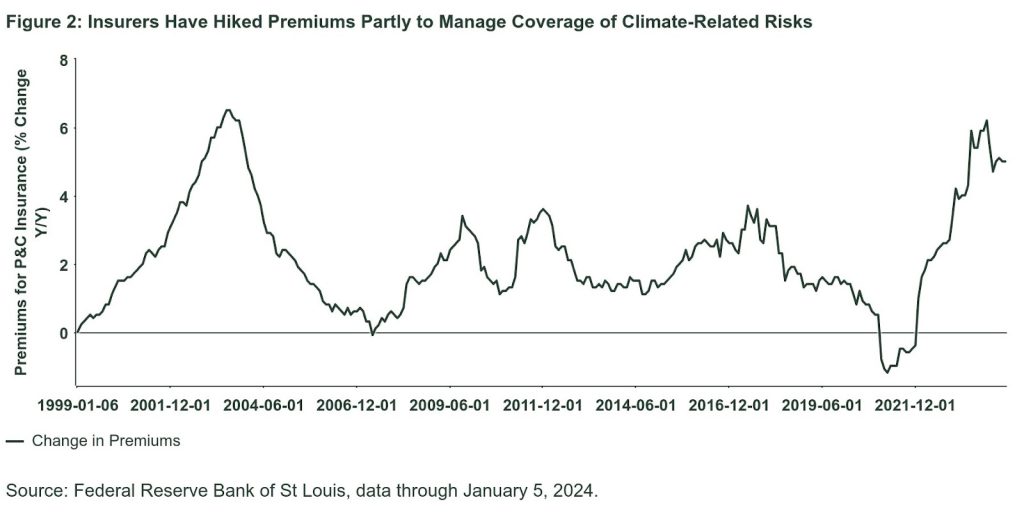

Insurers have reacted to the implications of severe weather events by lifting premiums (Figure 2). In the US, insurers have also reduced or eliminated the capacity they offer in states that are more significantly exposed to climate-related events and where pricing has not been adequate to cover expected claims. Consequently, home and business owners in some markets are no longer able to buy private insurance.

A New Regulatory Focus

Climate change has traditionally been considered to be a medium-to long-term risk from a supervisory perspective for insurers’ financial stability. Nonetheless, the increasing severity of weather events has brought the issue into more immediate focus for the regulators, insurance, and financial sector companies.

A surge in costs of insurance for policyholders, which can lead to certain markets becoming prohibitively expensive for building or inhabiting, could unleash a wide range of economic impacts. For example, builders must now pay special attention to whether their properties will be insurable in the future, and citizens must rethink whether to live in certain coastal communities.

Supervisors in both the US and Europe are conducting stress tests to assess the financial system’s resilience to potential physical and transitional risks from climate change. Regulators in Europe are exploring means of embedding climate risks into financial models, systems, processes, and policies.

Central Banks Weigh In on Climate-Related Insurance Risks

Central banks’ financial stress models have moved from looking at typical business cycles to integrating climate-related risks over longer-term horizons.

The European Central Bank (ECB) has identified climate-related risks as a key driver in the SSM4 Risk Map for the euro area banking system. The ECB is of the view that institutions should take a strategic, forward-looking and comprehensive approach to considering climate-related and environmental risks.

The ECB climate stress test for financial institutions also assesses the impact of climate-related risks on the profitability and solvency of corporations. Mitigants and amplifiers of climate risks are also accounted for, as both could impact insurance coverage and premium costs (Figure 3).

Figure 3: Schematic Overview of Climate Risk Transmission to Firms Through Credit Risk

The Bank of England’s Climate Biennial Exploratory Scenario (CBES) in 2021 found that households and businesses that are likely to be impacted by physical climate-related risks could face insurance challenges and concluded:

- Policymakers may need to address the availability and affordability of insurance.

- Climate change itself might result in serious macroprudential implications; for example, corporate or household failure to obtain or repay loans.

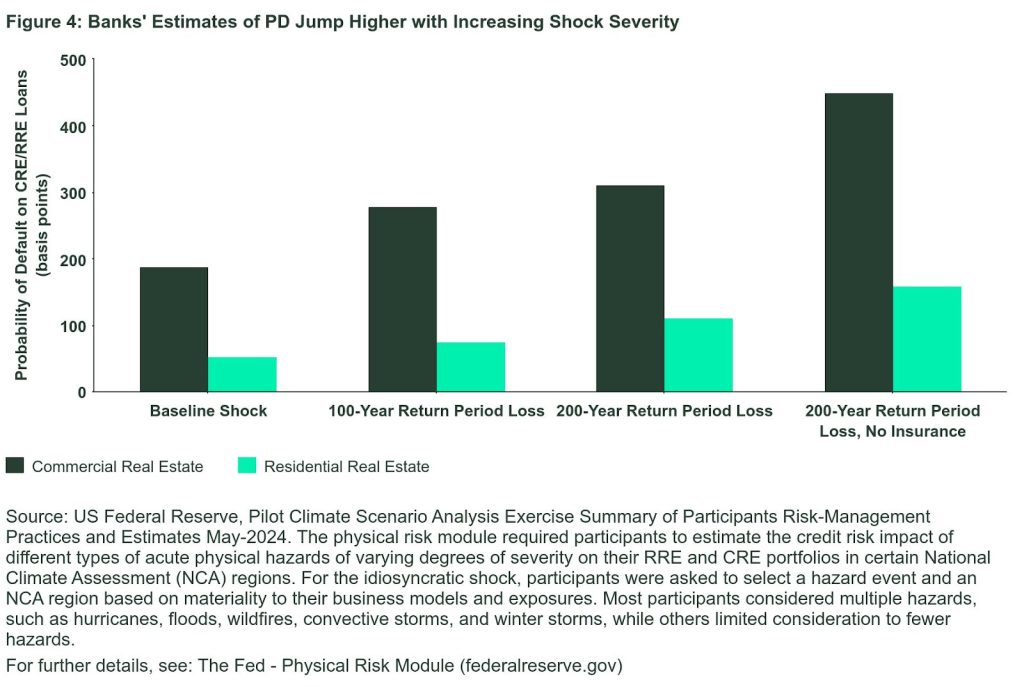

The Federal Reserve conducted a Pilot Climate Scenario Analysis (CSA) exercise in 2023 to learn about large banking organizations’ climate risk-management practices and challenges. The objective was to enhance the ability of large banking organizations and supervisors to identify and estimate climate-related financial risk.5 Participants named: Bank of America Corporation; Citigroup Inc; The Goldman Sachs Group, Inc.; JPMorgan Chase & Co.; Morgan Stanley; and Wells Fargo & Company.

In this exercise, “participants highlighted the important role that insurance plays in mitigating the risks of climate change for consumers, businesses, and banks. They noted the need to monitor changes across the insurance industry, including changes in insurance costs over time, and the impacts of those changes on consumers and businesses in specific markets and segments.”

A lack of comprehensive and consistent data related to “building characteristics, insurance coverage, and counterparties’” plans to manage climate-related risks was also highlighted.6 Participants’ probability of default estimates are in shown Figure 4.

The Bottom Line

Insurers face a difficult challenge to price their premiums appropriately for risk in order to remain solvent, to continue to offer competitive pricing, and also to avoid moral hazard from the customer side. Insurance premium pricing goes through cycles. However, upward pressure on pricing will persist in the longer-term if climate-related risks continue to build.

The sharp increase in insurance premiums can be a catalyst for:

- Households failing to insure their properties. Policymakers would then need to escalate their efforts to close the protection gap, but such measures have their own limitations.

- Households lacking protection during extreme weather, then defaulting on mortgages and loans in areas severely affected by weather-related events.

- In addition, banks might face having to make increased provisions for potential loan losses alongside contending with a rise in climate-related defaults. Extreme weather could also affect certain financial markets, e.g., agricultural commodity futures.

The rising cost of insurance premiums due to climate-related risk therefore has the potential to pose a new type of systemic risk for the financial system. Regulators are clearly concerned and more data is needed for the extent of the risks to be properly assessed by the rest of the financial industry.

Future costs associated with climate-related risks will likely have a material impact on the insurance industry. For this and other reasons, such as regulatory changes, decarbonization efforts, and reputational concerns for companies, investors should look to incorporate climate-related risks into their longer-term investment outlook.

Originally Posted July 26th, 2024, SSGA

PHOTO CREDIT:https://www.shutterstock.com/g/Sepp+photography

Via SHUTTERSTOCK

Footnotes

12023 was second only to 2021 for total damage costs through the first half of any year since the 1980 Hurricane Costs (noaa.gov).

2Long-term average based on storms over the period between 1950 and 2023.

3Allstate 2024 Proxy Statement

4Single Supervisory Mechanism; the SSM places significant banks in participating countries under the direct supervision of the European Central Bank (ECB).

5Pilot Climate Scenario Analysis Exercise, Summary of Participants’ Risk-Management Practices and Estimates, May 2024; https://www.federalreserve.gov/publications/files/csa-exercise-summary-20240509.pdf.

6See Pilot Climate Scenario Analysis Exercise, Summary of Participants’ Risk-Management Practices and Estimates, May 2024, Executive Summary.

Disclosure

Marketing Communication

State Street Global Advisors Worldwide Entities

The information provided does not constitute investment advice as such term is defined under the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell any investment. It does not take into account any investor’s or potential investor’s particular investment objectives, strategies, tax status, risk appetite or investment horizon. If you require investment advice you should consult your tax and financial or other professional advisor.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without State Street Global Advisors’ express written consent.

The returns on a portfolio of securities which exclude companies that do not meet the portfolio’s specified sustainable investment criteria may trail the returns on a portfolio of securities which include such companies. A portfolio’s sustainable investment criteria may result in the portfolio investing in industry sectors or securities which underperform the market as a whole.

Investing involves risk including the risk of loss of principal.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the appropriate EU regulator) who are deemed both knowledgeable and experienced in matters relating to investments.

The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

{kind=link}