Industrial firms are the lifeblood of the economy. Manufacturing accounts for 20% of U.S. capital investment, 60% of exports, and 70% of research and development spending.1 For such an important economic role, the sector’s outlook has vital implications for portfolio positioning.

While declining growth prospects are unfavorable for cyclical stocks, over time, investors could find bright spots in emerging themes. Years of underinvestment in infrastructure and a focus on factory productivity could deliver the long-awaited U.S. industrial renaissance.

Key Takeaways:

- A potential recession is negative for Industrials, stressing the need for increased productivity.

- The use of robotics and automation coupled with infrastructure spending could bolster a modern industrial revolution.

- Although structural drivers are intact, current market uncertainty warrants downside protection.

Industrials Lag, But Watch Spending Intentions

The industrial sector had an impressive run during the second half of 2022, aided by the passage of the U.S. Inflation Reduction Act. Spending appropriations on clean energy and infrastructure fueled investor optimism, but the sector’s rally was short lived. Industrials have since lagged the S&P 500 index by roughly -720 basis points (bps) this year as of May 16, 2023, driven by weakness in machinery, aerospace, and defense stocks.2 Performance dispersion increased in March around the time of the regional banking crisis.

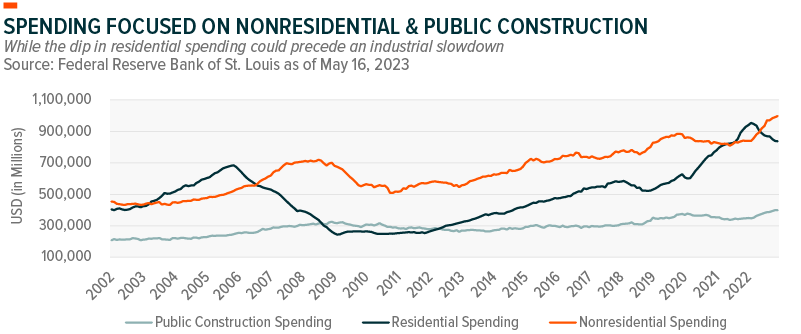

Underperformance could reflect growing recession concerns. Historically, lower residential spending, accounting for nearly half of the construction market, preceded industrial contractions.3 The residential space is more sensitive to interest rates, so the reduction in housing affordability shifted spending toward nonresidential construction.

On a positive note, public construction spending, which is less cyclical than private spending, could gradually increase as clean energy and infrastructure projects materialize. Stimulus spending during a recession could also be a tailwind for some industrial stocks.

An Upcycle in “Smart Manufacturing”

Beyond a possible recession, the next turnaround for industrials could be powered by digitization. Enter the new era of “smart manufacturing.”

Most manufacturers surveyed by Deloitte plan to increase operational efficiencies over the next 12 months using new technology. Robotics, automation, and internet of things (IoT) were the top three technologies favored by respondents.4

The use of “smart manufacturing” could provide substantial improvements in sustainability, factory output, and labor productivity – potentially boosting earnings. In the meantime, late cycle dynamics could merit defensive positioning.

Positioning in the Current Environment

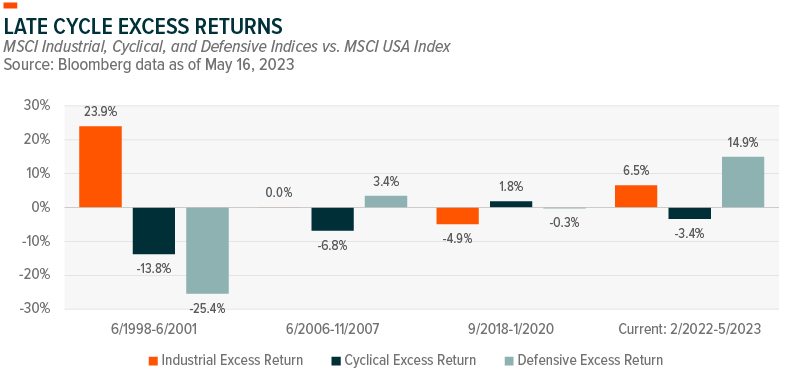

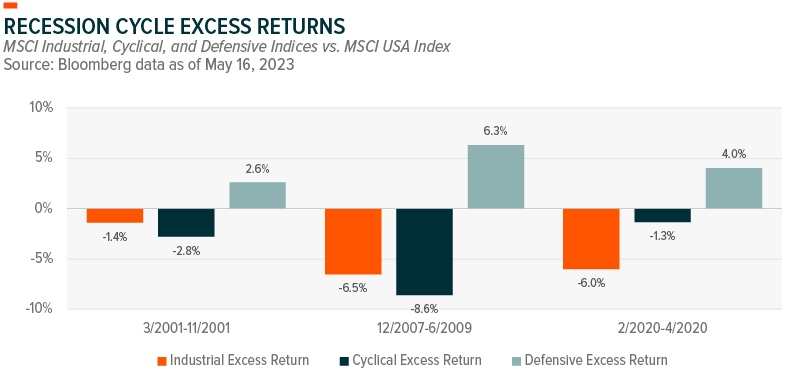

Market uncertainty will likely weigh on industrials, especially if the U.S. enters a recession. Historically, cyclical stocks, particularly industrials, underperform the broader market during recessions. However, the sector’s relative performance is typically mixed during late cycle phases.

Economic growth can remain positive during late cycles, albeit near peak expansion. As demand remains robust, the supply of goods and services is slow to adjust to an eventual late cycle slowdown. Rising prices are a consequence of a supply/demand mismatch, providing a sweet spot for some Energy, Materials, and Industrial firms, typically during the first stage of a late cycle peak.

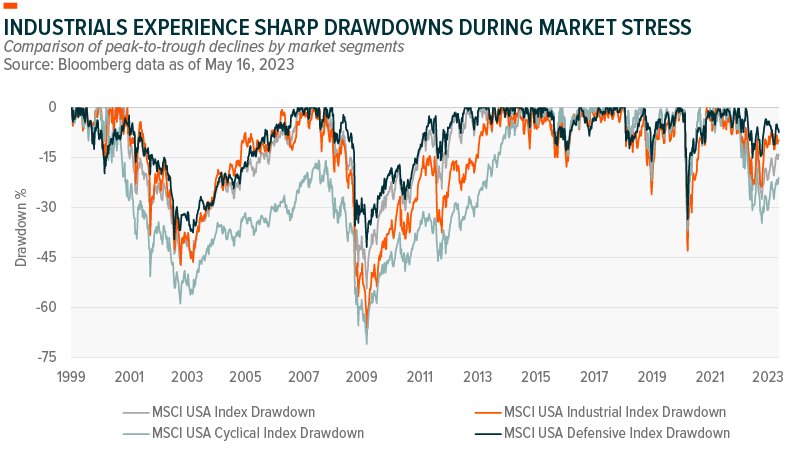

The late cycle launch was on full display in 2022 as commodities rallied and industrials had periods of outperformance. But the rally diminished. So far, Industrials and other cyclical sectors have experienced drawdowns of roughly -30% since peak performance in 2021, which is still above the -40% drawdown in 2020 and -70% in 2009, according to Bloomberg data as of May 16, 2023.

Maintaining flexibility is important during cycle shifts. Recessions warrant downside protection, while cyclical sectors and themes can provide diversification benefits over the long term. Our sector views table below provides more detail on positioning.

Footnotes:

1) McKinsey & Company, Delivering the U.S. Manufacturing Renaissance, August 29, 2022

2) Bloomberg data as of May 16, 2023

3) World Construction Network, U.S. Residential Construction Weakness Bears Down on Construction Spending, February 6, 2023

4) Deloitte, 2023 Manufacturing Industry Outlook, September 15, 2022

5) CNBC, ‘Once-in-a-generation’ Prescription Drug Pricing Reform Could be Coming, July 29, 2022

This post first appeared on May 30th, 2023 on the GlobalX blog

PHOTO CREDIT:https://www.shutterstock.com/g/Piscine

Via SHUTTERSTOCK

DISCLOSURE

Investing involves risk, including the possible loss of principal. Diversification does not ensure a profit nor guarantee against a loss.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information is not intended to be individual or personalized investment or tax advice and should not be used for trading purposes. Please consult a financial advisor or tax professional for more information regarding your investment and/or tax situation. Investors cannot invest directly in indexes. The MSCI USA Index is designed to measure the performance of the large and mid cap segments of the US market. The MSCI USA Cyclical index is designed to reflect the performance of the opportunity set of global cyclical companies across various GICS® sectors. The MSCI USA Industrials Index is designed to capture large and mid cap segments of the US equity universe. The MSCI USA Defensive index is designed to reflect the performance of the opportunity set of global defensive companies across various GICS® sectors. The S&P 500 Total Return Index includes 500 leading U.S. companies and captures approximately 80% coverage of available market capitalization. Investors cannot invest directly into indexes.