By; By Lee Clements, head of Applied SI, Global Investment Research, FTSE Russell

In March, the UN held its first water conference in 50 years, underlining the importance of this vital resource to health, social development and even economic growth. The conference culminated in the adoption of the Water Action Agenda, a “milestone” action plan containing almost 700 commitments to protect “humanity’s most precious global common good”.

General Assembly President Csaba Kõrösi said the $300 billion in pledges made to buoy the agenda has the potential of unlocking at least $1 trillion of socioeconomic and eco-system gains [1]. Mobilizing capital to address the challenge of providing clean water, cleaning up wastewater and maintaining the health of rivers, lakes & oceans (which is both vital for biodiversity and challenging as climate change impacts natural water cycles) is vital to everyone in both developed and developing markets.

Given the enormous demand for capital, it’s fortunate that the water has proven to be a solid investment: the small, but growing, water investment sector in the global equity market has outperformed the broader market over the last 10 years.

Despite this performance, investment in new water infrastructure is lagging other sectors. The total value of water and sewage projects and deals in 2022 was only $41 billion compared to $441 billion in mining, oil & gas and petrochemicals, according to data from Refinitiv Infrastructure 360. This new water infrastructure is needed to address a double challenge of aging infrastructure in the developed market, much of which is more than 50 years old [2] and providing much needed new water infrastructure to billions in the developing market. It is estimated that the latter, linked to SDG 6, will cost $114 billion per year by 2030[3][4]. The good news is that with investor focus and economic solutions such levels of mobilization of capital is possible, the total value of renewable energy projects and deals in 2022 was $655 billion, according to data from Refinitiv Infrastructure 360. Whilst there is still a long way to go on mitigating climate change, the success in mobilizing capital and at least partially integrating its consideration into economic models can be seen as a model for water (and other areas such as biodiversity can follow). Often the needs of these different environmental issues can be addressed by the same solutions.

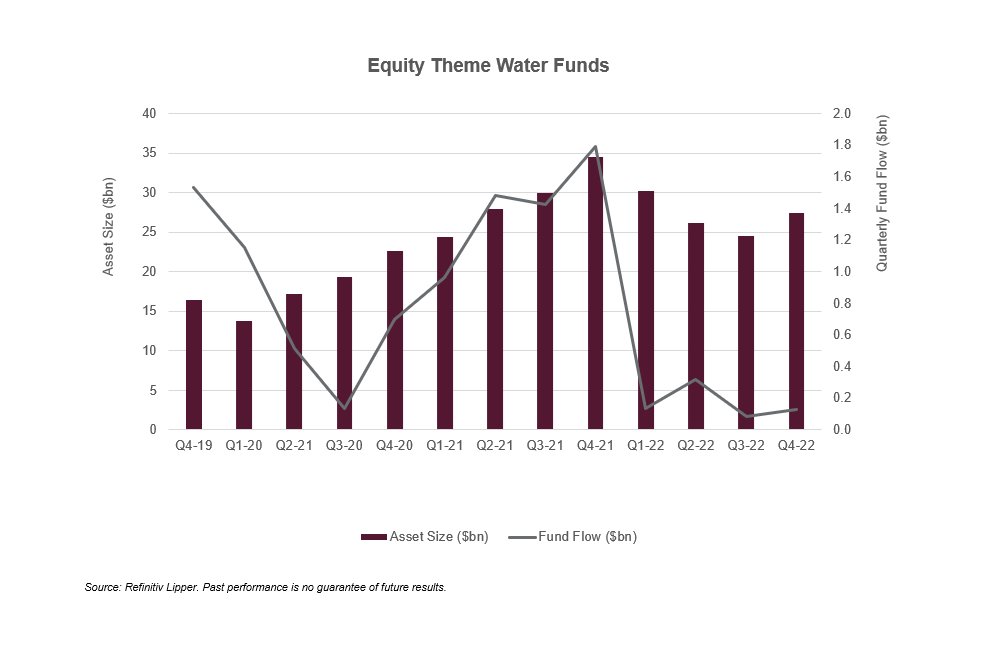

One positive aspect of investment in water is that it is already a small, but acknowledged investment sector, which has seen growing assets. The Equity Theme Water segment of investment funds now stands at more than $28 billion in assets, according to data from Refinitiv Lipper, having grown from $16 billion at the end of 2019.

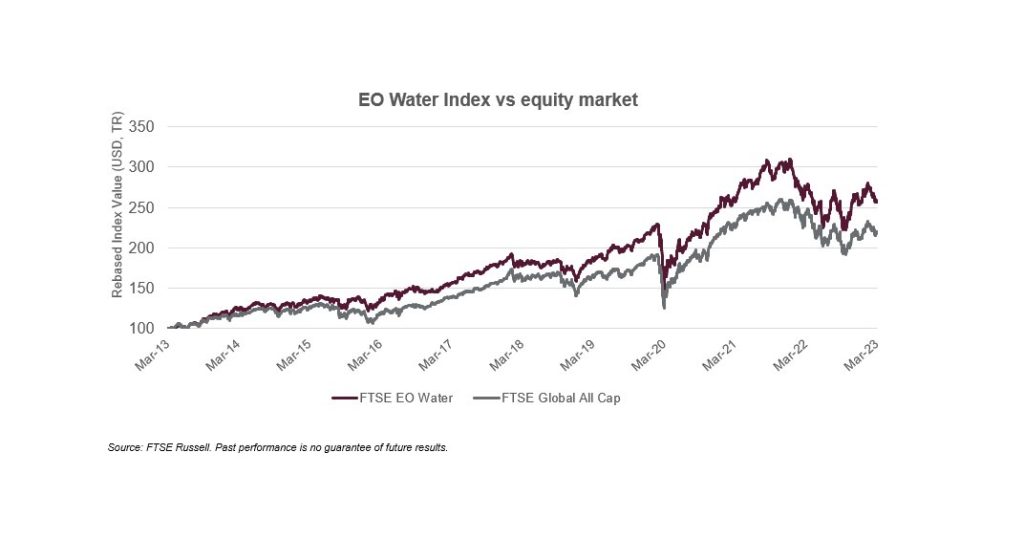

Another positive aspect is that whilst it is a small segment [5], it has a range of fascinating companies from water utilities to infrastructure developers and water technology manufacturers and has been a strong long-term performer versus the broader equity markets [6]. Over 10 years it has outperformed by 38%, whilst having a very similar level of volatility to the overall market.

Following the UN conference, given the vital need for investment, government funding pledges and the returns made by water investors who have already taken the plunge, hopefully we will see increasing flows (pardon the pun) into the water sector.

There is a long way to go. Whilst many people have gained access to safe drinking water and sanitation over the last 50 years there still remains a large gap to achieving the 2030 UN Sustainable Development Goal (SDG 6) of providing access to all. As of 2020, some 2 billion people still lacked safe drinking water in their homes and around one-third of people did not have basic hand washing facilities at home. The challenge is particularly acute in low-income countries, with an estimated 70% of the population of sub-Saharan Africa lacking safe drinking water services. Around half of the of the world’s population is already at risk of severe water scarcity for at least some of the year, according to the UN IPCC, with this figure likely to increase with the effects of climate change.[7]

For more information on sustainable investment Subscribe to our blog.

Originally Posted April 5th, 2023, FTSE Russell

PHOTO CREDIT: https://www.shutterstock.com/g/ladik

Via SHUTTERSTOCK

Footnotes:

[1] New agenda sets sail with bold action as UN Water Conference closes | UN News

[2] US water infrastructure: Making funding count | McKinsey

[3] Financing SDG 6 | Water.org

[5] FTSE Environmental Opportunities Water Technology Index (“EO Water”), made up of companies with >20% revenue exposure to the water sector, had 65 constituents with $207bn market cap at 28/2/23

[6] FTSE Environmental Opportunities Water Technology vs FTSE Global All Cap Index, USD Total Return 22/3/2013 to 24/3/2023

[7] The world faces a water crisis — 4 powerful charts show how (nature.com)

Disclosure:

© 2023 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”). The LSE Group includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE Global Debt Capital Markets Inc. and FTSE Global Debt Capital Markets Limited (together, “FTSE Canada”), (4) FTSE Fixed Income Europe Limited (“FTSE FI Europe”), (5) FTSE Fixed Income LLC (“FTSE FI”), (6) The Yield Book Inc (“YB”) and (7) Beyond Ratings S.A.S. (“BR”). All rights reserved.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, YB and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “FTSE4Good®”, “ICB®”, “The Yield Book®”, “Beyond Ratings®” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of the LSE Group or their respective licensors and are owned, or used under license, by FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, YB or BR. FTSE International Limited is authorized and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analyzing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing in this document should be taken as constituting financial or investment advice. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any representation regarding the advisability of investing in any asset or whether such investment creates any legal or compliance risks for the investor. A decision to invest in any such asset should not be made in reliance on any information herein. Indexes cannot be invested in directly. Inclusion of an asset in an index is not a recommendation to buy, sell or hold that asset nor confirmation that any particular investor may lawfully buy, sell or hold the asset or an index containing the asset. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back-tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

This document may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.

No part of this information may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of the applicable member of the LSE Group. Use and distribution of the LSE Group data requires a license from FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, YB, BR and/or their respective licensors.

The FTSE Global All Cap Index is a market-capitalization weighted index representing the performance of large, mid and small cap companies in Developed and Emerging markets. FTSE Environmental Opportunities Water Technology Index (“EO Water”), made up of companies with >20% revenue exposure to the water sector, had 65 constituents with $207bn market cap at 28/2/23 You cannot invest directly in an index.