By Patrick Hubert, Senior Lead SI Publications, SI Solutions

Since 2015, a growing fleet of hydrogen taxis has clocked up more than 6 million km in the Paris area, transporting over 800,000 passengers. The electric vehicles’ livery is unmistakable, with a clouds-on-blue-sky design catching the eye.

Even though it trades under the “Hype” name, its partners and backers are multinational industrialists (e.g. Air Liquide, Hyundai, Toyota, Total Energies) or finance heavyweights (CDC, France’s largest institutional investor Caisse des Dépôts).

Having acquired a taxi competitor a few months ago, it is converting its 600 cabs-strong [1] and growing what is already the world’s largest hydrogen taxi company.

Scaling Up

These multinational backers are members of the Hydrogen Council (HC) launched in 2017, which now gathers over 120 companies from diverse sectors – from utilities, the transport sector, energy and engineering companies to chemical producers, finance and more – “all committed to scaling up the hydrogen value chain to contribute to a clean and diversified energy system”[2].

Fighting ever more disrupting climate change requires mankind to bring greenhouse gas (GHG) emissions to zero, compelling us all to find alternatives for the ubiquitous fossil fuels.

For many needs, solutions have emerged and their deployment is exponential (e.g. renewable energies, electric mobility, battery storage). However, there are also some cases where hydrogen, despite challenges to overcome, could be the best bet.

Storage Challenge

Hydrogen as an energy carrier or chemical element is not new: the most abundant element in the universe, it was discovered in the 18th century. However, in its pure H2 form it is relatively rare and is not as easily stored and transported as most fossil fuels.

Hence, the latter beat hydrogen hands down as long as convenience and ease of use prevailed: H2 uses were confined to limited use-cases, such as space (energy for satellites via fuel cells[3], electrolysers and solar panels) and -overwhelmingly- to specific industrial petrochemical applications.

Only when GHG emissions became an issue did H2 emerge as a possible energy carrier: hydrogen fuel cells, though a prominent investment theme after the 1997 Kyoto Protocol, have been out of favour until fairly recently, with the creation of the HC.

As the Council requires commitments at the CEO level, their combined efforts are bearing fruits and 2021 could be seen as seminal: with Government commitments to deep decarbonisation gathering pace in the runup to COP26[4], the hydrogen investment pipeline had grown to $500 billion by July.

Investment Wave

In just the first half of last year, 131 large-scale projects were announced globally, bringing the total to 359[5]. Europe is leading, with investments of $130bn, but other regions are catching up and China has emerged as a serious hydrogen contender with over 50 projects, ushering in its announcement of net-zero emissions by 2060.

Concurrently, even though the segment softened in the wake of higher energy prices during H2 2021, the stock performance of hydrogen pure players has been impressive since 2020, whetting investors’ appetite for H2 IPOs (some infamous, like Nikola) which are expanding the visibility and breadth of quoted hydrogen securities.

Not everybody is jumping on the H2 bandwagon, and some of the doubters’ arguments are quite reasonable. The most contentious issue is how H2 is obtained: even though “green” molecules can be prised from water through electrolysis (using renewable electricity), 90+% of hydrogen today comes from cracking fossil fuels, generating CO2.

Skeptics Abound

Critics point out that many fossil fuel companies are backing hydrogen, seeing it as a way to extend the use of their proven reserves through reformation (producing H2 but also greenhouse gases) alongside the capture and storage of the associated carbon.

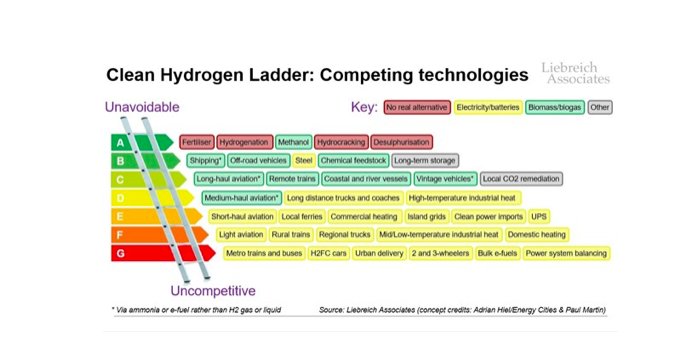

Efficiency is also a concern. Seasoned zero-emission energy observer Michael Liebreich, for instance, uses a “Clean Hydrogen Ladder” to illustrate and examine some of the potential H2 applications, ranking them from “Unavoidable” to “Uncompetitive”. He pits hydrogen against competing alternatives, like batteries for transport or biomass for chemical feedstock, and rates the use cases from A to G (like appliances).

He concludes that H2 is needed for fertilisers or desulphurisation, and probably steelmaking and long-term energy storage. However, for other applications like ground transportation or heating, he favours alternatives.

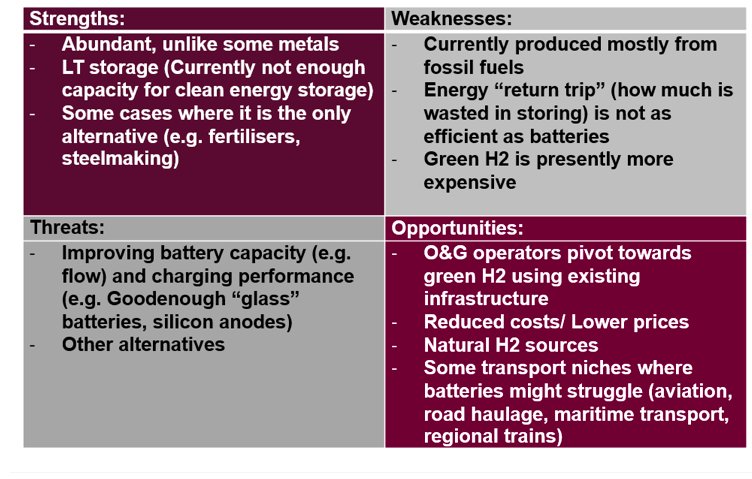

Taking all these pros and cons into account, a first-pass SWOT analysis could yield the following results:

Energy Transition

After many false starts and in spite of its detractors’ reservations, H2 could yet play more than a niche rolein the energy transition:

– While the fossil fuels heydays are over and decarbonisation is accelerating, the oil & gas majors know that hydrogens require infrastructure compatible with their culture and asset base (Hydrogen ‘A Huge Opportunity’ To Replace Fossil Fuels, Says U.S. Energy Secretary);

– Increased investments and government commitments are likely to prime the H2 sector in the same way they did in the solar energy segment, which saw the MWh price divided by 30 from 2000 to 2020 as solar modules and systems production volumes shot up : this time, the West intends to stay in the lead and, regardless, those investments are likely to make hydrogen competitive within 10 years (e.g. US Hydrogen Shot);[6]

– [Even if alternative technologies, such as batteries, achieved overall superior performance, better products often fail to fulfill their market potential: mankind is far from fully rational;]

– Green hydrogen, according to an International Energy Agency (IEA) forecast, has the potential to fulfill 17% of the global energy demand by 2050, leading to some contenders setting ambitious goals for themselves in the field: by 2030, Chile aims to become the world’s leading and cheapest green hydrogen producer[7]; Australia and Namibia have also been mentioned.

Green H2 should obviously be the favoured option in the context of zero-emission energy transition, and it is worthwhile noting that the IEA consistently underestimated the growth potential of solar energy throughout the 2000-2020 period: a similar underrating of the potential disruptive capacity for hydrogen should not be discounted.

Overall, despite some overt hype and a currently well-placed competition, is hydrogen finally an investment idea whose time has come?

This post first appeared on February 7 on the FTSE Russell blog.

Photo Credit: European Space Agency via Flickr Creative Commons

Footnotes

[1]A catalyst for change: How Parisian taxi firm Hype is creating supply and demand to build the hydrogen economy (h2-view.com)

[2] Op.cit. Hydrogen Council

[3] Fuel cells recombine pure hydrogen gas with oxygen from the air, producing electric power, water and heat.

[4]H2 was retained as one of the four items on the COP26 “Breakthrough Agenda”: COP26 World Leaders Summit- Statement on the Breakthrough Agenda – UN Climate Change Conference (COP26) at the SEC – Glasgow 2021 (ukcop26.org)

[5]Hydrogen Investment Pipeline Grows To $500 Billion In Response To Government Commitments To Deep Decarbonisation – Hydrogen Council

[6]The initiative seeks to reduce the cost of clean hydrogen by 80% to $1 per 1 kilogram in 1 decade (“1 1 1”)

[7]H2 Magallanes Project, Minister Jobet Announces New Green Hydrogen Project in Chile, up to 8 GW of Electrolysis Capacity – Hydrogen Central (hydrogen-central.com)

DISCLOSURE

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back- tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

This publication may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.

No part of this information may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of the applicable member of the LSE Group. Use and distribution of the LSE Group data requires a licence from FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and/or their respective licensors.