By Yilin Zhang, sustainable investment manager

The United States’ stance in addressing the climate crisis shifted dramatically in 2021 as the incoming President Joe Biden immediately rejoined the Paris Accord, issued an Executive Order on Climate-Related Financial Risk, and secured a bi-partisan Infrastructure Plan with a focus on low-carbon infrastructure and transportation.

But the direction of travel of the US has been green for longer than casual observers might think. The US remains the second largest emitter of greenhouse gases but we calculate that it is also the largest market in the global green economy with over $3 trillion of revenues generated from green products and services.

Green Bonds

This is a cross asset story. For example, from a fixed income perspective, during the first half of 2021, Green bond issuance totaled US$259.3 billion, nearly three times first half 2020 levels and all-time first half record.

Mergers & Acquisitions activity involving sustainable companies totaled US$84.3 billion during the first half of 2021, 13% of mergers or acquisitions and 68% of the total value of these deals were US based.

But from an equity perspective where the trend is most pronounced, and where green economy outperformance is most striking.

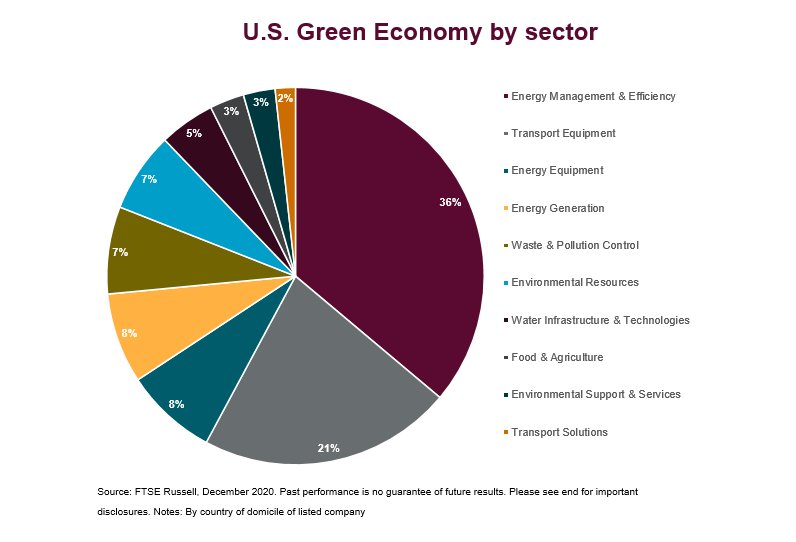

Green Sectors

Our FTSE Russell’s Green Revenues 2.0 data model looks at over 98% of the global public equity market, identifies companies with green products and services, and classifies them across 10 green sectors, 64 subsectors, and 133 micro sectors focusing on the whole value chain of the green economy.

This analysis reveals a US green economy, which is the world’s largest but relatively concentrated in the Energy Management & Efficiency sector.

This sector, comprising of companies that provide energy efficient IT products and services such as cloud computing, drives almost 40% of the US green economy.

The size of the second largest sector, Transport Equipment, has grown significantly in recent years driven by the expanding global market for hydrogen-powered, electric and hybrid road vehicles.

Infrastructure Bill

The $1.2 trillion bipartisan infrastructure bill passed by the Senate on August 10, 2021 focuses on transforming investment in healthy and sustainable transportation options, including the largest federal investment in public transit in history.

This includes electrifying buses and railways and building infrastructure for electric vehicles. Currently, the Transport Solutions sector makes up only 2% of the US green economy and is likely to grow boosted by the Infrastructure Bill spending, as well as other green activities including clean water infrastructure and renewable and alternative energy.

Investors tracking the US green story over the past five years have been rewarded. The US green economy has outperformed the US equity market as a whole, as well as more carbon intensive sectors.

This post first appeared on September 21 on the FTSE-Russell blog.

Photo Credit: Chris Jones via Flickr Creative Commons

Disclosure

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back- tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

This publication may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.

{kind=link}

{kind=link}