By Catherine Yoshimoto, director, product management

Among the pandemic’s countless impacts, soaring lumber prices is one where both investors and consumers are still feeling the ripple effects. Supply constraints combined with rising demand have sent lumber prices skyrocketing over the past year, ultimately impacting housing and construction prices.

But while there’s been much press surrounding how these prices have been passed to consumers, little attention has been paid to the very beginning of the supply chain—where the timber is being harvested. Timber REITs own and operate land that’s used for timber production and harvesting, and our analysis shows that they’ve benefited considerably from the lumber price surge.

Perfect Storm

The onset of the pandemic triggered widespread business closures—and lumber mills were not spared. Even when business resumed, some mills weren’t able to operate at full capacity amid COVID-19 safety concerns. And many didn’t ramp up production as they anticipated the pandemic crisis could weaken demand.

However, what they didn’t expect—and what actually happened—was the opposite outcome: housing demand boomed in the economic recovery. The monetary policy response to the pandemic resulted in low interest rates for home buyers. And as more of the pandemic-weary fled urban environments, housing demand exploded—as did home remodeling projects for the housebound masses.

An already reduced lumber supply fell short of this rising demand, and the imbalance has resulted in a headline-grabbing jump in prices. In the period from March 31, 2020 to April 30, 2021, lumber prices rose by a staggering 394%.[1] These higher costs were passed to home construction, and ultimately to new home prices—where in April 2021 lumber price increases added an estimated $36,000 to the cost of an average new home.[2]

Timber REITs

What’s been bad for the consumer has been good for Timber REITs

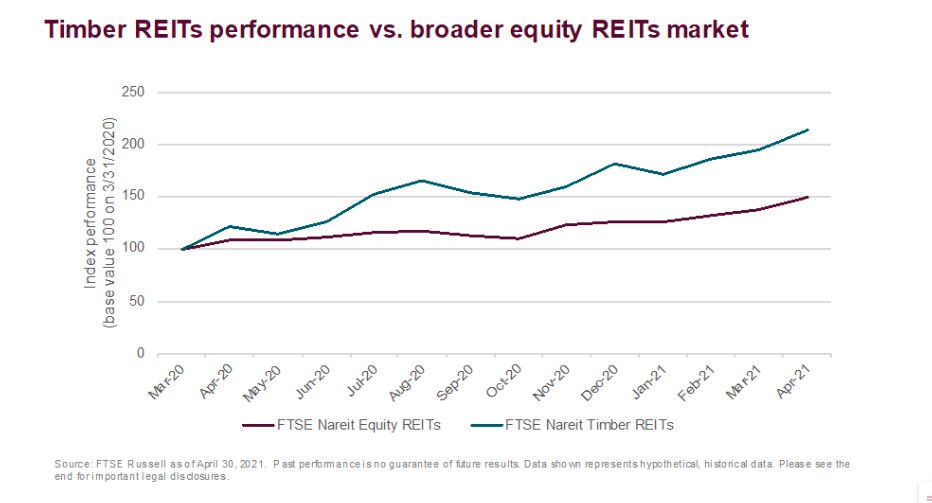

While the lumber price surge has meant higher costs for the end consumer, it’s been a boon for the other end of the supply chain. A closer look at our FTSE Nareit Timber REIT Index reveals that Timber REITs—which own the land where trees are grown and harvested—have materially outperformed the broader equity REIT market over the past year.

As shown below, since March 2020, the FTSE Nareit Timber REIT Index has outpaced the FTSE Nareit Equity REITs Index—which excludes Timber REITs—by a wide margin.

Big Picture

If housing and construction demand should stay on its trajectory and the lumber industry continues its scramble to address supply shortages, upward pressure on lumber prices could persist.

And like many trends set in motion by the pandemic, there are winners and losers, some of which might be less obvious than others—underscoring the importance of looking across the entirety of the supply chain for investment opportunity.

This post first appeared on June 14 on the FTSE Russell blog.

Photo Credit: in hiatus via Flickr Creative Commons

FOOTNOTES

[1] Source: NASDAQ as of April 30, 2021

[2] Source: The National Association of Home Builders, April 2021

DISCLOSURES

© 2021 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”). The LSE Group includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE Global Debt Capital Markets Inc. and FTSE Global Debt Capital Markets Limited (together, “FTSE Canada”), (4) MTSNext Limited (“MTSNext”), (5) Mergent, Inc. (“Mergent”), (6) FTSE Fixed Income LLC (“FTSE FI”), (7) The Yield Book Inc (“YB”) and (8) Beyond Ratings S.A.S. (“BR”). All rights reserved.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “MTS®”, “FTSE4Good®”, “ICB®”, “Mergent®”, “The Yield Book®”, “Beyond Ratings®” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of the LSE Group or their respective licensors and are owned, or used under licence, by FTSE, Russell, MTSNext, FTSE Canada, Mergent, FTSE FI, YB or BR. FTSE International Limited is authorised and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back- tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

The FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property. The FTSE Nareit Timber REITs Index is a free-float adjusted, market capitalization-weighted index of wood products. Investors can’t invest directly in indexes.

This publication may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.