Reflecting on how the pandemic has impacted US real estate investments this past year, global index provider FTSE Russell and Nareit hosted a virtual panel to better understand today’s listed real estate market and what may lie ahead as the industry adjusts to the short and potentially longer term impacts of COVID-19.

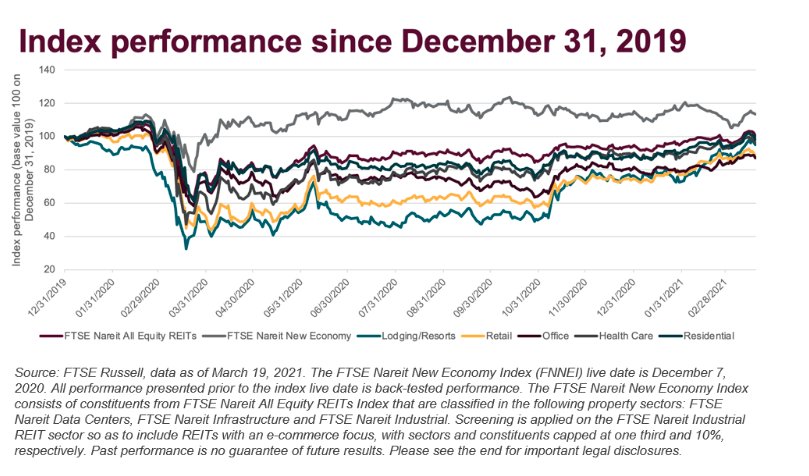

Recent data from FTSE Russell shows the index performance since December 31, 2019, with an uptick in October 2020.

Exposure Risk

Highlighting the macro outlook, experts from LaSalle Investment Management, Brookfield Asset Management and Nareit discussed various topics, including investors’ view of exposure to traditional REITs and “newer” ones (noting whether it influences public vs. private considerations), ESG integration and how the phenomenon of remote work impacts commercial real estate demand.

Key takeaways from the session included:

Bernhard Krieg, Portfolio Manager, Brookfield Asset Management:

“Investing in real estate securities can be an attractive sector going forward, not only for the short-term dislocation but also because we’re starting a new cycle, lending itself to tremendous opportunity. Real estate more broadly, but also real estate securities, is driven by long and steady upcycles. We’re seeing rents grow, occupancies increase, and eventually more supply will level things off.”

Calvin Schnure, SVP, Research & Economic Analysis, Nareit:

“I don’t foresee risk of inflation. Rather, we’re likely to see continued low interest rates which are very favorable for commercial real estate. As expected, the macro fundamentals are improving which will further drive demand over the next 12 months.”

Lisa Kaufman, CEO, LaSalle Investment Management:

“There’s been a trend in both private and public real estate markets for investors looking for exposure outside the four major sectors of Office, Retail, Multifamily and Industrial. We’re seeing growing interest in niche sectors like cell towers, data centers, storage and healthcare, as a lot of these specialty sectors have delivered better and more resilient growth through the last cycle. Many of those sectors have acyclical or sometimes even countercyclical demand drivers which provides good diversification for investors and allows them to play some of the secular shifts happening.”

This post first appeared on April 12 on the FTSE Russell Blog.

Photo Credit: Andreas Riemenschneider via Flickr Creative Commons

© 2021 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”). The LSE Group includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE Global Debt Capital Markets Inc. and FTSE Global Debt Capital Markets Limited (together, “FTSE Canada”), (4) MTSNext Limited (“MTSNext”), (5) Mergent, Inc. (“Mergent”), (6) FTSE Fixed Income LLC (“FTSE FI”), (7) The Yield Book Inc (“YB”) and (8) Beyond Ratings S.A.S. (“BR”). All rights reserved.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “MTS®”, “FTSE4Good®”, “ICB®”, “Mergent®”, “The Yield Book®”, “Beyond Ratings®” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of the LSE Group or their respective licensors and are owned, or used under licence, by FTSE, Russell, MTSNext, FTSE Canada, Mergent, FTSE FI, YB or BR. FTSE International Limited is authorised and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

The FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property. The FTSE Nareit New Economy Index consists of constituents from FTSE Nareit All Equity REITs Index that are classified in the following property sectors; FTSE Nareit Data Centers, FTSE Nareit Infrastructure and FTSE Nareit Industrial.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back- tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

This publication may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.

No part of this information may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of the applicable member of the LSE Group. Use and distribution of the LSE Group data requires a licence from FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and/or their respective licensors.

{kind=link}