By Steven Levine, Senior Market Analyst at Interactive Brokers

Two aerospace-related firms hit the radar recently with new investment-grade corporate debt offerings, while the sector undergoes financial and existential uncertainties in the wake of the Covid-19 pandemic.

U.S.-based Raytheon Technologies Corp (RTX) and Honeywell International (HON) each entered the primary market with fresh corporate debt issuance, amid commercial aerospace supply disruptions and potential defense spending headwinds.

Both companies have witnessed a precipitous drop in the value of their stock to date in 2020, as wreckage from the coronavirus crisis, and other adverse impacts, have generally battered their financial health.

Risks Ahead

Raytheon Technologies, for example, which has proposed at least US$500m worth of new 10-year and 30-year fixed-rate bonds, has contended with a recent slew of risks to its commercial aerospace operations, including virus-inflicted reductions in air travel and aircraft demand.

The company said it expects to use the net proceeds from the bond sale for general corporate purposes, including the repayment of outstanding indebtedness.

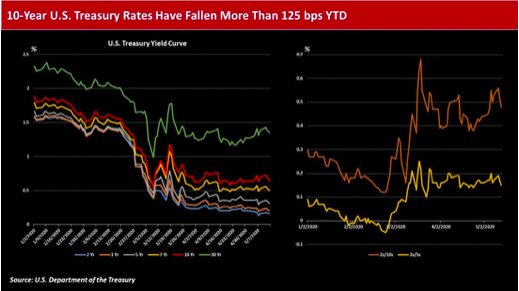

The yield on the 10-year U.S. Treasury note was last bid at around 0.61% intraday Thursday, a 4-basis point drop from the prior day, and roughly 127 bps since the start of the year.

Debt Pressures

S&P Global Ratings, which assigned an ‘A-‘ issue-level rating to the firm’s proposed unsecured notes, noted that Raytheon Technologies aims to exchange the new bonds for an estimated US$9.2bn worth of outstanding debt issued by its subsidiaries Goodrich Corp., Rockwell Collins, and Raytheon Co.

The new notes will mirror the principal amount, interest rate, and maturity date of the notes they are being exchanged for, while covering all of Raytheon Technologies’ subsidiaries’ debt – with the exception of US$1bn worth of Raytheon notes due in October 2020.

S&P in early April had upgraded Raytheon Technologies by one notch to ‘A-’ from ‘BBB+’ following its all-stock merger with United Technologies and spun-off entities Otis Worldwide and Carrier Global.

The combination propelled Raytheon Technologies to become the world’s third-largest aerospace and defense (A&D) company behind Boeing (NYSE: BA) and Airbus (OTCMKTS: EADSY), as well as the largest tier one commercial aerospace supplier, and second-largest U.S. defense contractor behind Lockheed Martin (NYSE: LMT).

However, more recently, S&P lowered its outlook on the firm to negative from stable, amid the likely impact on its commercial aerospace business from the pandemic-induced decline in air travel and aircraft demand.

Lowered Expectations

While Raytheon Technologies has focused on cost savings of around US$2bn and cuts to cash spending of about US$4bn to offset the lower demand and impact on operations, S&P analysts Christopher Denicolo and Richard Federico said they lowered their expectations for funds from operations (FFO) to debt to 23%-27% in 2020 and 30%-35% in 2021, from 30%-35% and 35%-40%, respectively.

However, they added that “there is still significant uncertainty regarding how low air travel will go and how long it will take to recover.”

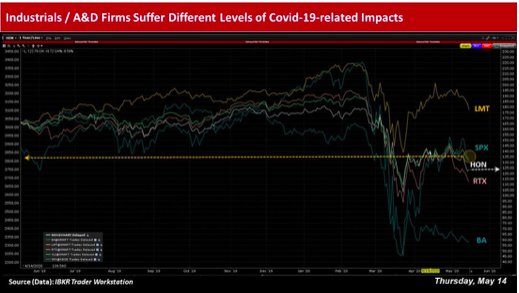

Shares of Raytheon Technologies have plunged nearly 42% year-to-date in 2020 and were last trading down more than 2% to around US$52.56 intraday Thursday.

Honeywell’s Outlook

Meanwhile, Charlotte, North Carolina-headquartered Honeywell was also set to sell at least US$500m worth of ‘A’-rated, 5-, 10- and 30-year bonds, amid the still ultra-low U.S. interest rate landscape.

The company said it intends to use the net proceeds from the offering for general corporate purposes, and after completion of the sale, it aims to permanently reduce its undrawn commitments under its Delayed Draw Term Loan Agreement, which it initiated in late March, by an amount equal to the aggregate principal of the issuance.

While many of Honeywell’s first quarter of 2020 financial metrics met or exceeded management’s targets – US$2.21 EPS, 3% operating profit growth, 2% segment profit growth, and 140 bps of segment margin expansion – the firm’s sales fell 5%, or 4% organically.

Honeywell CEO Darius Adamczyk said that as the Covid-19 pandemic “rapidly escalated and the global economy deteriorated, we faced headwinds across our businesses, including rapid changes in our supply chain, constraints at customer sites, and significant impacts on the commercial aerospace and oil and gas end markets.”

Due to the evolving nature of the novel coronavirus crisis and related supply chain and market disruptions, Honeywell, like most companies, suspended its full-year financial guidance until the economic impact from the virus stabilizes.

Honeywell also expects ongoing top-line challenges due to the current market conditions, particularly in the aerospace and oil and gas sectors.

The company’s stock has also staged a massive drop of -33.5% year-to-date, and was last up around 1.42% to US$123.50, according to the IBKR Trader Workstation.

Threats & Affordability

Investors eyeing the A&D industry will also likely be monitoring how government spending may change in the wake of the pandemic.

Mckinsey analyst John Dowdy noted that two factors have historically had the most influence on defense spending: threats and affordability – and both will “come into play in the aftermath of the coronavirus pandemic as governments calibrate the relative importance of the threats they face against their new economic realities.”

He continued that “scenarios suggest that the economic impact of the Covid-19 pandemic could exceed anything experienced since World War II.

“If historic trends repeat, governments are likely to curtail defense spending to fund other priorities. But with government debt at high levels, there is less money to go around. Together, these forces may put many countries on the brink of a deficit-driven defense downturn.”

Dowdy added that from 2008 to mid-2017, global government debt more than doubled to reach almost US$60tn, despite deleveraging expectations in the aftermath of the financial crisis. As a result, countries now face “greater financial constraints because they have less dry powder than they did in 2008.”

Photo Credit: Jorge Láscar via Flickr Creative Commons

DISCLOSURE: INTERACTIVE BROKERS

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.