As the US moves into the third year of a presidential term, we typically get a rally to prepare the public to support the party in power.

If we look at the recent companies that have gone public, Beyond Meat (BYND) in my view stands out as the poster child for the year. After coming public at $25 per share, the stock hit a high of $200 and has since come down from that lofty height.

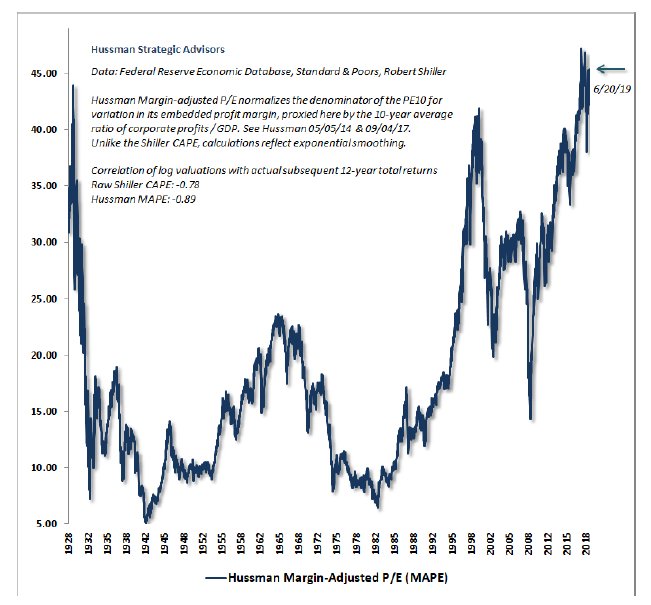

In the last 6 months we have seen the worst December stock market ever and the best June since 1938. We need to look under the covers to make some sense of the current environment.

Trade Wars

Let’s look at what valuations are telling us, comment on the trade wars, and discuss the implications of rate cuts by the Federal Reserve (Fed).

Stock markets hate uncertainty. In my opinion, there is certainly a case to be made that trade relations between the US and other countries have been uneven.

In China, for example, US companies have prohibitive barriers to entry. And when they do gain access to Chinese markets, a technology transfer is usually part of the price.

Yet the speed and number of tariffs now being proposed have investors concerned about the impact to future corporate profits.

Volatility Spike

This concern has shown itself in the amount of volatility that we have experienced over the past year and a half. We have had the worst December ever and the best June ever.

Yet the stock market is largely in the same place it was at the end of September 2018.

Fed Rate Cuts

As the third quarter begins, market watchers are keenly anticipating a rate cut at the next Fed meeting at the end of July.

For the past couple months a rate cut has been factored in by the financial markets. The only question today is only how big the cut will be.

The importance of a rate cut stance by the Fed is that this typically signals a weakening economy. A weakening economy then leads to a downturn in the stock market and possibly a recession.

Stay Cautious

Stock markets often cheer the first rate cut by the Fed. History shows, however, that the stock market begins to turn down over subsequent months. These are historical observations and do not guarantee that a downturn necessarily must happen.

What they do say, however, is that a downturn is likely over the coming year. We will therefore remain cautious in our risk management and keep our eyes open for signs that a downturn has begun.

Gold was up about 9% in the second quarter, meanwhile the gold miners fund (GDX) rose about 14%. This strength has continued into the 3rd quarter.

Inflation

In my opinion, the strength we are seeing in this sector is presaging the coming of inflation. Part of this inflationary tendency will likely be spurred by the upcoming rate cut by the Fed. Rate cuts usually weaken the US dollar.

When the dollar weakens imports become more expensive. Likewise all those commodities (such as oil and copper) that are priced in US dollars will likely also see a rise in their prices.

When we see the recent cover of Businessweek calling for the death of Inflation you can count on one thing. That is, that the public widely believes that inflation is no longer a threat to the economy. It’s these type of magazine covers with a broad appeal that make for good contrarian signals.

Contrarian Signal

What we are seeing in the price of gold and the Businessweek magazine cover hint at coming inflation.

For investors as well as savers, and especially retirees, inflation is a four letter word. Inflation can have a large impact on what we can purchase with our dollars.

Should inflation begin to now take hold we will begin to reposition the portfolios to emphasize investments that protect against the effects of inflation. In the meantime we will look to continue to participate in the move up in stocks.

Photo Credit: bryan via Flickr Creative Commons

Disclosure: Certain of the information contained in this article is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. These statements are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. The author believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.