“If we don’t change the direction we are headed, we will end up where we are going.” — Jodi Picoult

The markets zagged and zigged dramatically during the quarter and ended about where they began at the beginning of the year.

In my opinion, for the first half of the quarter, fear dominated market sentiment. Oil prices plunged to their lowest level in more than a decade, equity markets around the globe dropped into correction territory, US interest rates plunged, credit spreads widened and volatility increased markedly.

Daily declines of 1% or more in equity markets sapped investor morale. Risk was “off.”

February 11 marked the low point with the S&P 500 off 10.5% for the year, the worst start to a year ever recorded.

Bounce Back

For the rest of the quarter, risk was “on.” I believe markets recognized that oil prices were not going to zero, US GDP was not dipping into recession, earnings were OK and equities were pretty attractive from a valuation perspective.

By the end of the quarter, the S&P 500 had rallied 12% to return 1.3% for the quarter, oil prices rallied nearly 50% to end the quarter at $37/bbl and the benchmark ten year Treasury yield recovered modestly to end the quarter at 1.78%.

Dovish Fed

Weak global economies and muted growth in the US led the Fed to leave interest rates unchanged after the December 2015 increase.

The Fed’s dovish comments spurred a rapid decline in interest rate expectations and the dollar weakened against a basket of foreign currencies by more than 5% from the end of January.

Market expectations of inflation remain at 1.5% while wages rose 2.3% from the previous year and unemployment ticked up to 5.0%.

With inflation tamed, unemployment low and a slowly growing economy, in my view, the accommodative policy of the Fed can best be explained by concerns about overseas economies where the news is bleak.

Election Theatrics

Political uncertainty in the Presidential race appears to be somewhat lower than at the beginning of the year but has by no means disappeared, further contributing to market fears.

Central Bank policies overseas remain stimulative, with the Bank of Japan joining European markets to offer bonds (including ten year notes) at negative interest rates.

Nearly $7 trillion in government debt now yields less than 0%, which may be unprecedented. The European Central Bank also announced new measures to address deflation and foster economic growth, with little measurable impact on a weakening economy.

Default Worries

Fears in the banking sector on potential defaults related to energy loans contributed to this negative sentiment, while terrorism in Belgium and the UK vote in June on exiting the European Union (Brexit) create additional geopolitical uncertainty.

In my opinion, Europe and Japan do not appear to have the near-term ability to change economic direction.

Markets around the globe were in correction territory (off -10% or more) by the middle of February.

In the US, the S&P was down more than -10%, developed markets were off nearly -13%, emerging markets were down more than -10%.

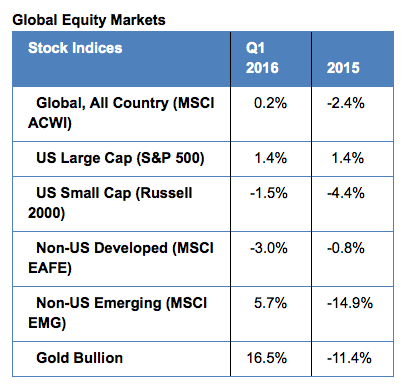

The pain was widespread and deep. By the end of the quarter, US markets (S&P) rallied more than 12% to end the quarter up 1.4%, emerging markets (MSCI) rallied 20% to end up 5.7% and developed markets (MSCI) rallied 10% to end the quarter down -3.0%.

Real estate (REITs) returned positive 5.0%, benefiting from lower interest rates. MLPs remained on a downward trajectory, off -6.0%, with the Alerian MLP index off nearly 40% of its value since the beginning of 2015.

Gold rallied during the first half of the quarter and maintained its gains, up 15.9% for the year to date, after a poor (-10.6%) 2015.

International Markets

Overseas, developed markets in Europe (-2.5%) were harmed by financial sector and consumer weakness despite monetary stimulus. Sectors and countries dependent upon Chinese trade were also weak.

Japanese equities were down -6.5% in dollar terms and down -12.6% when priced in yen. Canadian equities (up 11.3%) were buoyed by a stronger loonie and higher commodity prices.

Emerging markets were buoyed by a weakening dollar and recovering oil prices after a terrible 2015. Latin American countries rallied 19% for the quarter while China and India lagged, off -4.8% and -2.5% respectively.

Fixed Income

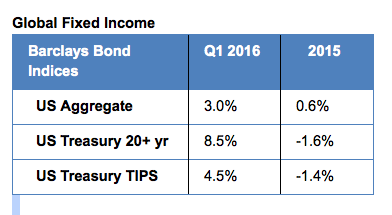

Bonds performed well for the quarter with the Barclays US Aggregate Bond Index returning 3.0% for the quarter. US Treasuries posted their best first quarter return since 2008 as yields dropped nearly 50 bps (0.50%) from year-end in a volatile quarter. The Barclays US Treasury Index returned 3.2% for the quarter.

Investment-grade and high-yield corporate bonds see-sawed, drastically underperforming in January and early February before rebounding with oil and stocks through quarter-end.

Investment-grade corporate bonds hurt by worries over persistent low-/negative-interest rates, outperformed like-duration Treasuries by 70 bps for the quarter as the Barclays Credit Index returned 3.9%.

High Yields

High Yields moved with equities and returned while Industrials, buoyed by a rebound in commodity prices, outperformed by 70 bps.

The Barclays High Yield Liquid Index returned 3.7% for the quarter, even though it was down -5% through February 11th.

Credit option spreads remained unchanged (1.7%) for the quarter, while hitting spreads on February 11 (2.2%) not seen since June 2012. US TIPs returned 4.5%, reflecting their longer duration and increased inflation expectations.

Macro View

I believe that if the trends continue, stabilization in the equity markets, oil’s rebound and the weakening dollar should provide a needed lift to US consumer sentiment and to US corporate earnings in sectors such as energy.

If this boost to corporate earnings translates to higher inflation and somewhat higher GDP, then the current low unemployment and good consumer demand for autos and housing may also continue.

In my opinion, this should give the Federal Reserve ammunition to raise rates again, which it is desperate to do, thereby helping certain financial sectors such as regional banks.

In my view, oil’s rebound and the dollar’s fall, if continued, will also give certain emerging markets economies some breathing room.

It is not surprising that Canada, Russia and Brazil were top performers in the first quarter.

Eurozone

Troubling news for the global equity investor is the expected drop in forecast GDP in the Eurozone to 1.4% from 1.7% and Japan’s inability to inflate its way out of a decades-long economic malaise.

While non-US valuations are somewhat cheaper than in the US, we are not favorable towards non-US developed equity markets. Non-US bonds, on the other hand, are somewhat more interesting than previously.

We use currency-hedged non-US bonds to reduce volatility in non-US fixed income due to currency exposures.

Summary

If we don’t change direction, we’ll wind up where we’re going. Rapidly changing financial markets anticipate changes in economies that happen only slowly.

Thus, we observe volatility in financial markets when very little is actually changing in the world economy. While markets are rational and self-clearing, they frequently over-react to short-term phenomena due to investor behavior and sentiment.

We submit that the first quarter of 2016 is a good example of this short-termism. The woes and angst of February turned into complacency by March’s end.

We look to broad diversification in asset classes and categories and a longer-term outlook for markets to temper our reactions to sudden changes. Over the very long term, we believe that this approach will result in arriving safely at our end destination.

Photo Credit: Pacheo via Flickr Creative Commons

{kind=link}