“Stocks look expensive. What shall I do?”

Given that the US stock market is entering the 7th year of a bull market, (now the 3rd longest in US history) this is the most frequently asked question we hear from clients.

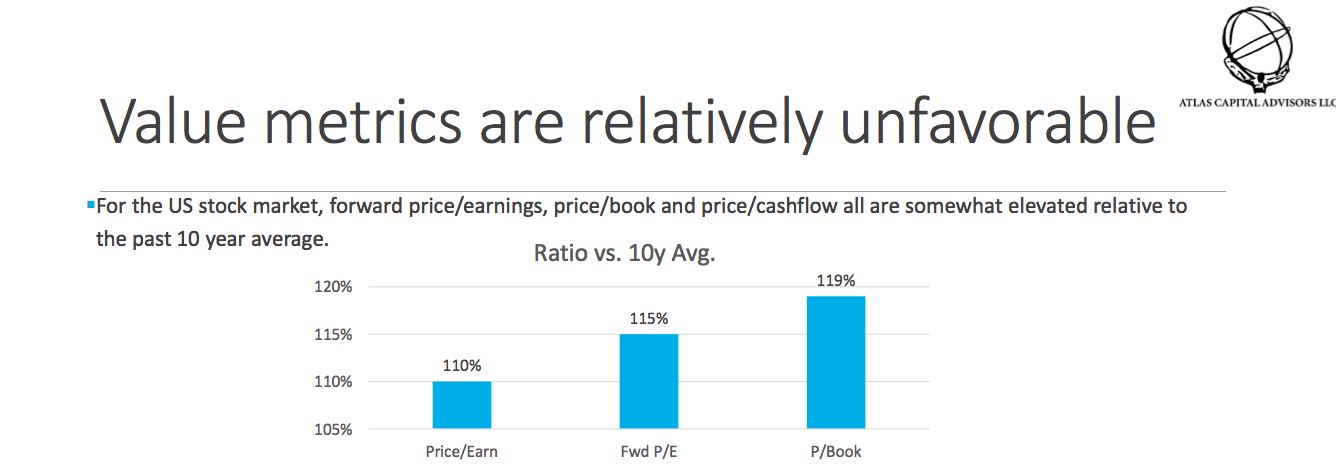

There’s no question stocks are pricey relative to the last 10 years.

Valuations

In the three years ended June 2015, the total cumulative return from the S&P 500 was 70%.

But trailing earnings per share rose only 14%. Most of the 70% resulted from investors accepting a worse price to earnings relationship.

While European stocks were more attractively valued than US stocks last year, European valuations are catching up.

Best Case

I believe emerging market equities have better valuations than developed market equities, but pockets of overvaluation are present there as well.

In my opinion, the likely result is some level of disappointment for stock market investors.

In our opinion, we think the best case for US stock investors is low single digit returns from stocks over the next 10 years, until valuations moderate.

Sell now?

So is it time to sell now?

Reducing stock holdings (particularly US stock holdings) now could be justified, given relatively high stock market valuations.

However, the use of value signals alone can sometimes lead to poorly timed adjustments.

Professor Robert Shiller of Yale was recently awarded the Nobel Prize in economics, in part for his work on developing long-term valuation metrics for financial markets.

CAPE Valuations

His valuation metric for the stock market is the cyclically adjusted price-to-earnings ratio, commonly known as CAPE:

o The CAPE is the ratio of the current stock index price to the average earnings of the index companies over the past ten years.

o High levels of the CAPE are seen as signals that future stock market returns are likely to be disappointing

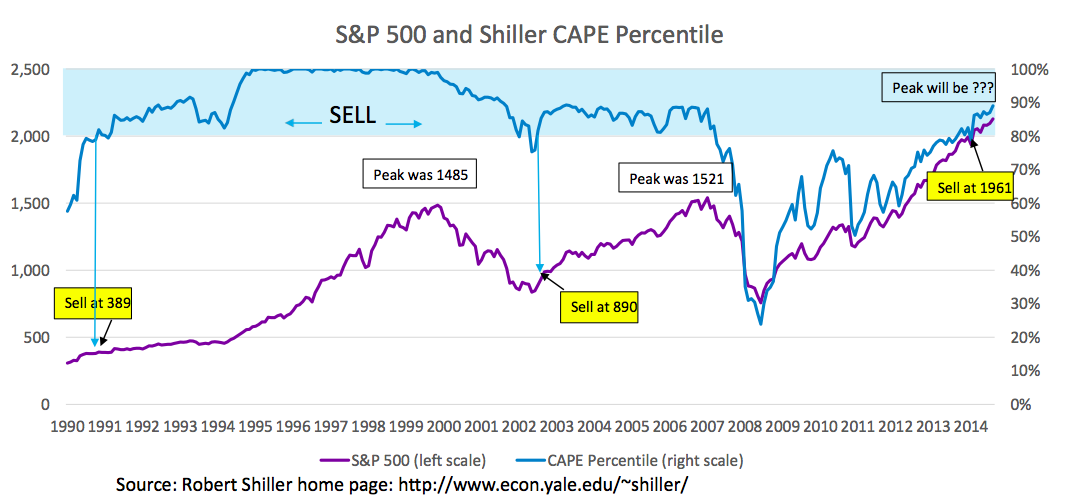

o The current S&P 500 CAPE metric is 26.7. That level is in the 85th percentile of CAPE readings for the past fifty years, meaning that valuations have been worse than now only 15% of the time.

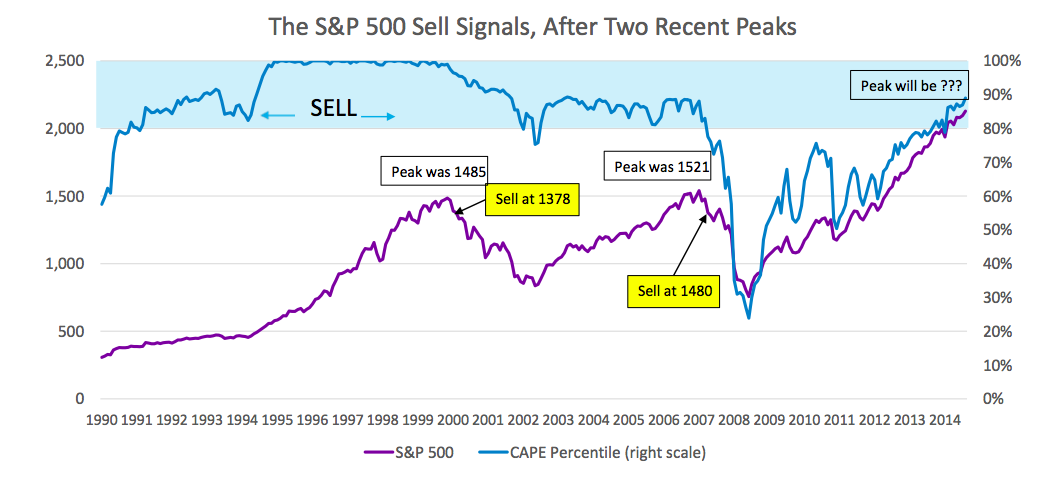

Atlas uses three standard types of technical rules for determining the whether market prices are in an uptrend or downtrend.

They include an exponential moving average rule, a simple moving average rule and a parabolic rule.

Under these rules, the change in direction in the S&P 500 which would have been identified subsequent to the two peaks indicated in next chart would have happened at the times and prices indicated in the chart.

So, let’s look at what happens when we use CAPE as a valuation trigger to sell equities.

Long View

Our 30 years in the markets have taught us to be cautious about being market “pundits.”

Market moves that “should” happen based on reasonable assessments of value can take years to actually occur, if they occur at all.

We expect to get better results using a price momentum signal to confirm our valuation hypothesis, waiting for a downtrend to be established before reallocating our equity holdings.

The next chart shows when we would could have exited the US stock market subsequent to the two major peaks of the past 25 years.

The sell points happen when the Shiller CAPE rises above the 80th percentile. As the chart indicates, one would sell in August 1991 when the CAPE percentile reaches the 82nd percentile.

After August 1991, the first time the CAPE percentile falls below the 80th percentile is the brief period you can see on the chart at the beginning of 2003.

Presuming that you reinvested in the S&P 500 at that time, your rule would take you out of the S&P 500 again quickly, in April 2003 at a price of 890 when the CAPE percentile was 82%.

You would have stayed out of the S&P 500 all the way until January 2008, when the CAPE percentile fell below 80%. Then, the CAPE percentile remained below 80% from January 2008 until August 2014.

Value and Momentum

Just like valuation rules alone are not sufficient, momentum rules don’t always help

o The main challenge arises when a trend is detected in one direction and then the market quickly goes the other way

However, I believe a combination of valuation and momentum may often be able to tell us a more nuanced and reliable story about the market than valuation alone.

These are principles that we use in our stock selection process, and we believe they are valuable in helping us understand the broader markets as well.

Strategy

So what should I do next?

Don’t panic. Valuations are high but volatility is low. There will likely be enough time to make thoughtful decisions. Have a plan.

I recommend, if appropriate, that investors diversify their portfolios outside of the US, particularly if their US holdings are more than half of their total equity holdings.

Emerging markets and certain other pockets still exhibit reasonable valuations. Diversification is still the only ‘free’ lunch.

Atlas has a global equity strategy with an emphasis on seeking strong downside protection combined with a systematic approach to foreign exchange risk management.

We believe that this might be a valuable tool for our clients.

In summary:

— Protect stock market gains – seek to limit losses in any downturn

— Diversify into non-US equity that’s less expensive

— Manage currency volatility in a strong USD environment

Photo credit: The Tire Zoo via Flickr Creative Commons