Everyone seems to be a stock market genius nowadays. Cast your eyes toward the Twittersphere, CNBC, Bloomberg, and almost any stock-related website, and it’s not difficult to find some investment managers who appear to be racking up some very impressive returns.

In some ways, I believe that we are witnessing a changing of the guard — the battled-scarred and time-tested investors of old replaced by new kids on the block: young, energetic, tech-savvy, driven, and seemingly invincible.

The problem with the track records of this new generation of investing stars is that, in a lot of cases, these stars have not been tested in heavy battle. When it comes to analyzing the true merits of these latter day saints, it’s not going to be easy to separate the lucky from the smart.

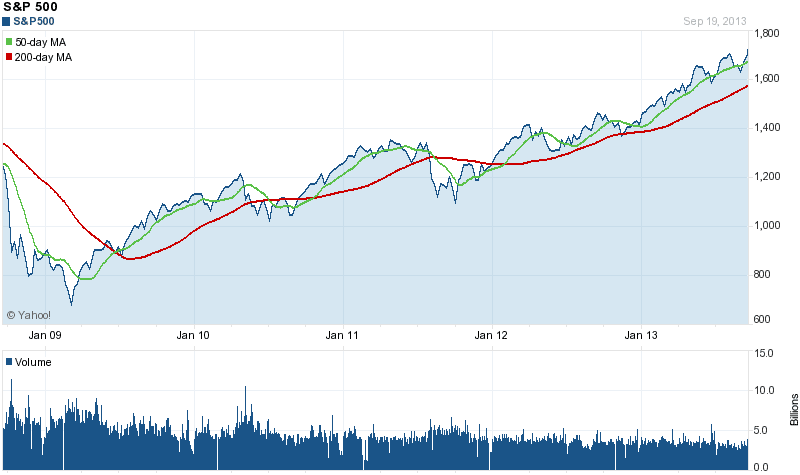

Here’s a chart of the S&P 500 over the last five years:

Source: Yahoo

Quite frankly, when the market displays a persistent upward slope like this, everyone should be able to post good results. Track records showing performance only over the last three or five years are missing an important judgment element: crisis.

Here’s a chart of the S&P 500 going back ten years:

Source: Marketwatch, Bigcharts

Looking at an investor’s performance after the market bottom in March of 2009 tells you nothing about how they are likely to manage crisis. I believe it’s important to consider how they positioned their portfolio in 2007, immediately before the crash. Did they see the storm clouds coming and prepare for heavy weather? And how did they perform during 2008 when global markets fell around 40%?

Given the way the market has been for the last three to five years, with nothing but endless sunny days and forever blue skies, any perusal of investor performance over shorter time frames could produce a false signal.

It’s sad but true; any investor who has spent even a minute thinking about downside risk over the last five years has likely underperformed the profit potential of this market. Anyone fully invested on the long side, and beta-leveraged, has probably outperformed.

Unfortunately—and it grieves us to admit it—we are not a candidate for latter day sainthood. My portfolio is cash-laden, with a small position in the ProShares UltraShort Russell 2000 Fund (TWM), and is underperforming even a dart-throwing, blind monkey.

The problem for us is that to believe in the sustainability of today’s market, one has to believe in the magnificent God-like omnipresence of Ben Bernanke, the current chairman of the Federal Reserve, who recently announced his money-printing and dollar-confetti-tossing party would continue ad infinitum. So far, it has proved to be the height of folly to be a disbeliever.

Old dogs like us, who persistently and naively cling to the idea that greater safety and opportunity comes with buying stocks at a discount to their value, are getting whipped by the young puppies who believe in QE infinity, and their own immortality, in almost equal measure.

Mr. Warren Buffett, of Berkshire Hathaway, and the fourth-richest man in the world, is “having trouble finding things to buy.” Seth Klarman, of Baupost Group, another well-worn market veteran, is returning money to clients because of what he sees as a lack of opportunity and rising risk in today’s market.

Many seasoned value investors, myself included, are moving to the sidelines and raising cash due to the paucity of investable ideas. Meanwhile, of course, intoxicated and overdosed by Benny’s little helpers, the bull market for latter day saints rages on. What a drag it is getting old.

The investments discussed are held in client accounts as of September 30, 2013. These investments may or may not be currently held in client accounts. Certain information contained in this presentation is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The manager believes that such statements, information and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.