In the Alice-in-Wonderland logic of financial markets these days, bad news is good and good news is bad.

A solid economic recovery would bring the U.S. closer to the day when the Federal Reserve will eventually stop its $85 billion-a-month bond-buying program and start to raise its benchmark interest rate from near-zero levels.

In this environment, disappointing developments such as a slight tick up in jobs claims or a below-expected first quarter GDP number are good for stocks in that the liquid refreshment from the Fed is likely to continue.

The release of the Fed minutes on May 22, which suggested discord among policy members about the wisdom of the central banks current quantitative easing program, sent shivers around global markets. Markets regained their nerve after prepared testimony from Fed Chairman Ben Bernanke soon after signaled that no big changes in monetary policy were in the offing.

In short, there’s an unhealthy dependency problem between the Fed and investors. Bernanke and company will need to tread carefully with their public comments and think long and hard about their exit strategy when they are ready to move. An abrupt or poorly communicated move could easily send global markets into a tailspin.

The uncertainly about the Fed’s future moves is already making itself felt in certain markets. Japanese stocks, which had rocketed up 65% over the last six months, have fallen back more than 10%, the common definition of a correction, thanks in part to nervousness about quantitative easing in the U.S.

^N225 data by YCharts

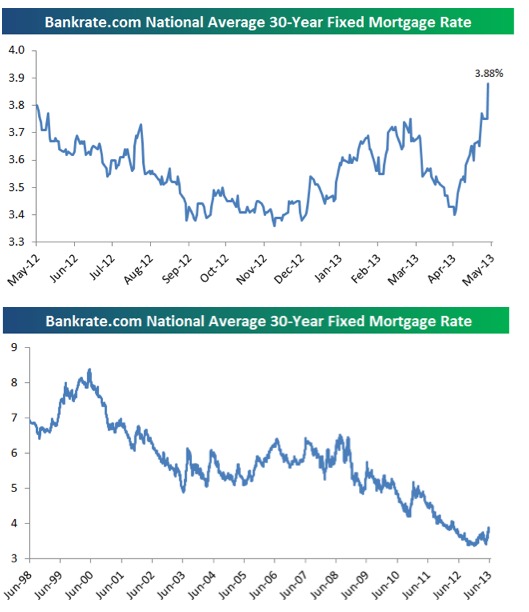

Meanwhile, the national average 30-year fixed mortgage rate tracked by Bankrate spiked 13 basis points yesterday from 3.75% to 3.88% as the bond market sold off across the board, according to the Bespoke Investment Group. Mortgage rates have jumped significantly this month, with the 30-year fixed rate rising 48 basis points from the 3.4% level it was at on May 1st, though it should be noted that home loans are still cheap by historical standards.

And it seems the long-expected selloff in bonds may have commenced. Yields for 10-year U.S. Treasuries touched 2.23 percent yesterday, the highest level since April 5, 2012, amid speculation the Fed will reduce asset purchases. Meanwhile, billionaire investor Warren Buffett told CNBC that bonds are a “terrible” investment right now and “priced artificially” high due to the Federal Reserve’s massive asset buying program.

For a contrary view on bonds, check out this post from Covestor investment adviser John Gerard Lewis, who manages the Stable High Yield portfolio.

{kind=link}

{kind=link}

{kind=link}