In a nutshell, the first quarter performance of the stock market in 2013 was the strongest since 1998. The S&P 500 Index (SPX) was up 10.61% with all industry sectors in the plus column.

This broad based climb was led by healthcare, consumer staples and consumer discretionary companies. Even the relatively steady utility area posted double digit returns. On the weak side were basic material and technology companies, where positive returns did not keep up with the overall market.

Stepping back, a look at sector performance numbers suggests that the rally was not a cyclical event associated with a sharp upturn in the economy. Strong parts of the rally (healthcare, consumer companies and utilities) are better known for being defensive sectors that tend do better during weak periods.

Basic material stocks, a group that lagged, often outperforms in economic upturns. International stocks also failed to keep up with the S&P 500. Given these observations, I believe domestic large cap (S&P 500) investors were largely encouraged by other factors.

One such factor was fiscal cliff legislation signed into law on January 2nd. There have already been low rates for dividends and gains prior to this legislation, but previous legislation always had an expiration date. The new fiscal cliff legislation does not have an expiration date for investment tax rates that remain well below ordinary income rates.

There was a modest increase for high wage earners, but this should affect relatively few. Proof of this market benefit comes in the form of a 2.56% gain in the S&P 500 on the January 2nd signing date that equaled 24% of the quarter’s total return.

It also stands to reason that sectors that hold dividend payers (like the mentioned healthcare, consumer and utility companies) were among the best in the market even though the nature of the economy did not change much.

In my opinion, politics may have also played a role in this too. Most of us are frustrated with government that is divided and dysfunctional. One of the outcomes of this, however, is that there is relatively little chance for near-term passage of any sweeping legislation that will have a high impact on the economy.

Together, I believe investment tax rates and the low probability of major legislation provided some assurances for investors. Outside of the political area, markets were also helped by the perception that the United States appears to have a fundamental outlook favorable to other global players, our markets were and are reasonably valued, our currency is relatively attractive, our energy outlook is improving, our banks are healthy, and our real estate markets appear to be in a sustainable recovery.

At this time it is nice to feel good about what has happened, but it needs to be remembered that investing is mainly about looking ahead. As mentioned, I believe market valuations are reasonable so there is little indication of a bubble. It also appears that many of the current positives have sustainable qualities.

My caution with the current situation is that the first calendar quarter tends to be a seasonally strong economic period and that we may soon see economic numbers that are less robust. Secondly, I believe the market is now positioned with strongly positive expectations for upcoming quarterly earnings.

I am encouraged with where this market is going over the long-term but believe near-term positive news is probably priced into the market already. As such, my performance expectations for the upcoming quarter are modest.

Other important areas are interest rates and the future course of the Fed. Over the past three months, the yield on 10-year Treasury bonds modestly climbed from 1.78% to 1.87% but this was enough to cause overall bond market returns to be negative (-.13% for the Barclays Aggregate).

Looking ahead, I don’t think we are going to see any major rate increases with the Fed openly stating that it must see a sustainable 6.5% unemployment rate before they start to normalize interest rates. Many, however, are very concerned about the day the Fed starts its normalization process.

That is a justifiable concern, but I believe it is already something the Fed has considered and will execute in a very open and methodical fashion. It will be an uncomfortable adjustment period but I don’t think it will be a disaster as many speculate right now.

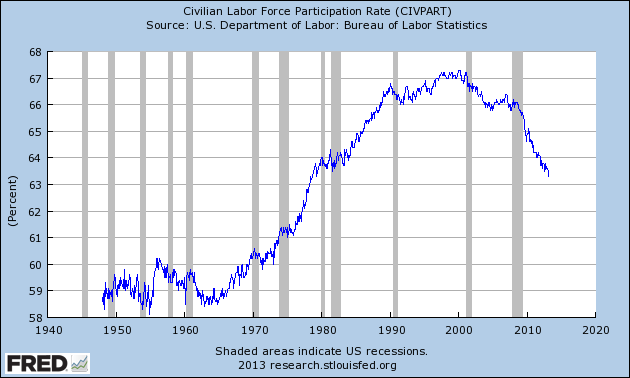

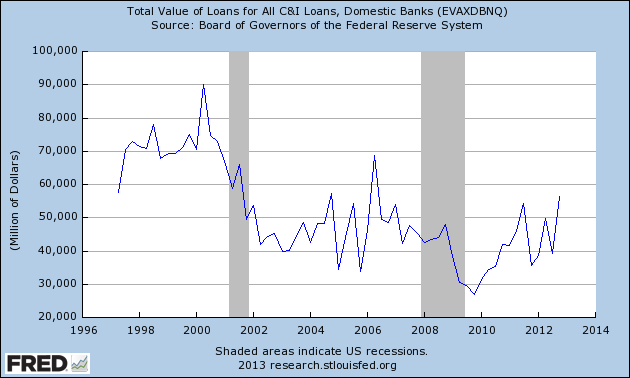

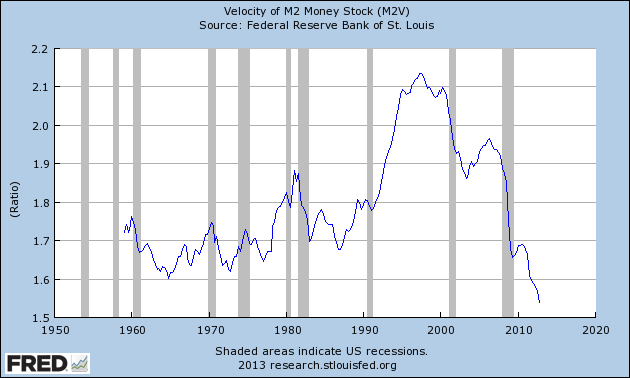

Three key graphs on the macro picture:

1. CIVILIAN LABOR FORCE PARTICIPATION RATE – A concerning trend is seen in a high number of potential workers that are not participating (working or looking for work) in the labor market:

2. COMMERCIAL & INDUSTRIAL LOANS – An increase in commercial lending activity is a good sign:

3. VELOCITY OF MONEY – This probably frustrates the Fed more than anything. More money is in the system but spending (velocity) is very slow. People and businesses are still cautious which contributes to the soft nature of economic growth:

A final topic to close on has to do with long-term investing. There were loud voices during the crisis saying you had to be a trader to make money. After four years, such voices have largely gone quiet and long-term investors have made some handsome gains despite a boatload of issues. Investors that missed this recent and largely unexpected rally may find their investment records to be less than where they would like it to be.

{kind=link}