Executive Summary

In our opinion, Teva Pharmaceutical Industries’ (TEVA) stock price seems to be significantly below intrinsic value, no matter how conservatively this is calculated.

Introduction

TEVA is an international pharmaceutical company headquartered in Petah Tikva, Israel. It specializes in generic and proprietary pharmaceuticals and active ingredients. It is the largest generic drug manufacturer and one of the 15 largest pharmaceutical companies worldwide, with sales of $18.3 billion, net income of $560 million and a total staff of 40,000 as of December 31, 2011.

Company’s History

Teva’s DNA is in the generics business, where it focused during the early part of its history scoring considerable success thanks to its cost-conscious corporate culture, focus on efficient operations, advanced technology and an understanding that gains in scale eventually translate into a cost advantage in this industry.

Teva expanded rapidly during the last 10 years through a combination of conservative management and smart acquisitions and achieved 27% earnings growth rate with return on invested capital around 20% as of the last reporting period.

Besides generics, Teva increasingly built up its presence in branded drugs. While not involved in discovery (the identification of effective new compounds), Teva has acquired existing compounds frequently taking advantage of its close relationship with top Israeli scientific institutions, such as the Weitzman Institute. It is from the latter facility that Teva acquired Copaxone, its top selling drug for the treatment of multiple sclerosis or MS.

During the last 3 years Teva’s stock has been under heavy pressure due to a number of concerns. First, the regulatory and competitive environment for the generics business is changing. Second, Teva’s Copaxone franchise is under threat by both generic manufacturers and alternative new branded drugs. Third, a set of operational difficulties involving two of Teva’s plants has temporarily reduced sales on certain product lines.

Industry Overview

Macroeconomic outlook

Teva operates in an industry blessed by generally favorable long-term economic trends. The healthcare sector is expected to continue to benefit from the aging of the world population (older people need extra healthcare) and from increasing adoption rates of western medicine by emerging countries.

The generics segment in particular is also poised to benefit from tightening government healthcare budgets and from the advent of biologics. To counter that, however, tightening budgets may also create pricing pressure on branded drugs, especially in developed countries undergoing a long deleveraging process.

Competitive Scenario

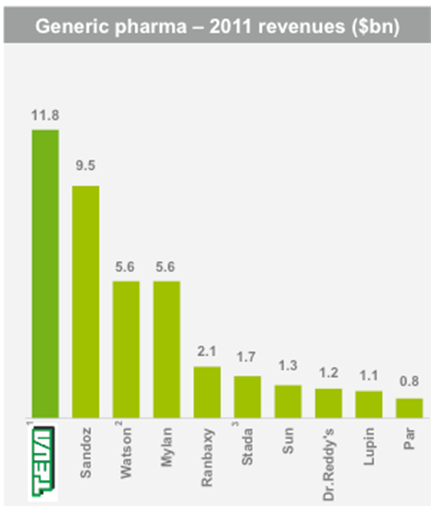

Teva operates and competes in several industry segments. In generics, Teva is one of the leading players, followed by Novartis-owned Sandoz (NOVN), Mylan (MYL) and others. Thanks to efficient manufacturing, logistics and scale, Teva is the low cost producer in its industry.

In my opinion, it is also in the best position within the industry to capture a significant share of the upcoming biologics market, given its technological leadership in generics and proven track record to come out with advanced generics quickly.

In branded drugs, Teva is the #11th world’s largest pharmaceutical company. Teva focuses on CNS (central nervous system), respiratory, women’s health and other lines of business. As customary in this industry, Teva’s revenues are protected by patents and moderately captive customers (more on this later).

A Porter 5-Forces analysis confirms that Teva tends to retain most of the value generated in its lines of business as both customers and suppliers have limited bargaining power, substitute products are few and entry barriers are significant.

Lines of Business

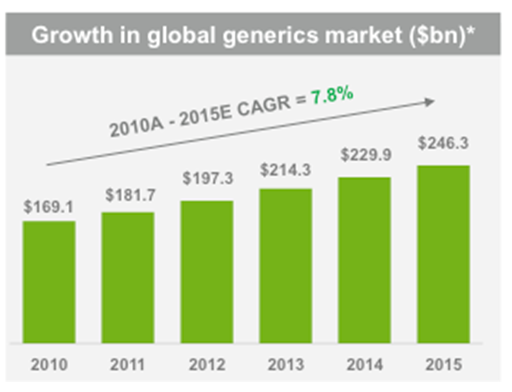

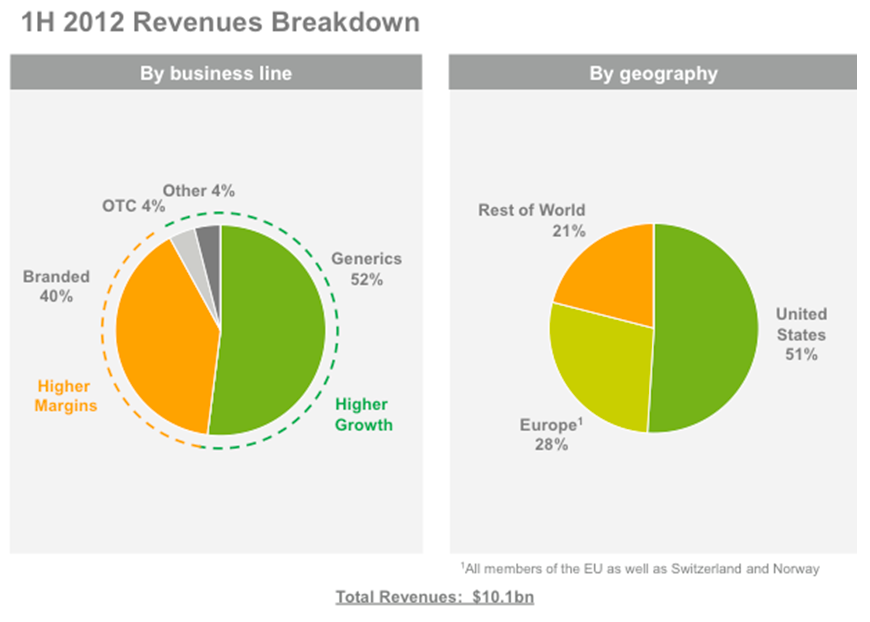

Teva’s sales are approximately divided 50/50 between generics (faster growing at 7.8% expected CAGR) and branded (higher margin). In 2012 sales are expected to reach $20.5 billion, according to consensus estimates posted on Teva’s website.

Sales originate 50% in the US, roughly 30% in Europe and 20% in the rest of the world. There is an existing trend, consistent with the management’s stated strategy, to increase the share of sales coming from emerging markets. About 4% of sales derive from the over-the-counter market, thanks to a recent partnership with Procter & Gamble (PG) (we expect this share to increase in the future).

Outstanding issues

Overview

Teva’s share price has been recently hovering around $40, approximately the price it was trading at in 2005. Considering that between 2005 and 2012 net income tripled, it is clear that the stock is being looked at with extreme skepticism by the market. There are a number of reasons:

Management change

Mr. Shlomo Yannay, Teva’s former CEO, has been replaced by Jeremy Levin. The latter is an extremely experienced executive, but has refused to confirm his predecessor’s guidance pending a thorough strategic review that will be made public in mid December. The market is clearly uneasy for what it perceives as uncertainty and lack of clarity. We believe there will be no big surprises, but following our “investigative” activity we believe the new strategy will focus on the following points, which we think make sense:

- Developing its existing pipeline

- Divesting non-core businesses

- Rationalizing and centralizing R&D, with focus on CNS

- Avoiding larger M&A in favor of smaller transactions

- Focusing on biologics and emerging markets

Changes in the generics industry

The generics industry is going through a period of transition. Volume growth continues to be attractive (high single digit), but a number of adverse changes means that past levels of profitability are unlikely to be maintained for the following reasons:

First-to-file (and its 180-day exclusivity period) are becoming rarer, mostly due to…

- …authorized generics becoming more frequent

- Competition ahead from low cost producers in emerging countries

- European economic downturn

Therefore, we believe that generics sales will continue to grow, but there will be some pricing and margin pressure at some point. The trend could be reversed with the arrival of biosimilars, but the exact timing is uncertain.

Teva experienced some problems in its production facilities in California and Jerusalem, causing a temporary shutdown and consequent decrease in production and sales. According to Teva’s management, those issues have been resolved.

Uncertainty about Teva’s Copaxone franchise probably lies at the core of the stock’s recent underperformance.

Teva’s brand leader is currently the top selling drug for the treatment of multiple sclerosis, with 2011 sales of $3,570 billion or 20% of Teva’s sales. This remunerative franchise is threatened by a number of elements:

- Immediate generic threat due to patent challenges

- Medium-term generic threat following patent expiration in 2015

- Immediate threat from recently-launched competing branded drugs

Because Copaxone clearly represents such a significant share of Teva’s revenue and profit, it is important to quantify the magnitude of these threats and its impact on the bottom line.

1) Immediate generic threat due to patent challenges:

This threat is no longer relevant. For several years now, Teva has engaged in a legal battle against Sandoz, which tried to circumvent Teva’s patents challenging their validity. The issue has been definitively resolved in court with a clear victory for Teva: no generic version of Copaxone will be authorized before 2015.

2) Medium-term generic threat following patent expiration in 2015.

In 2015, Teva’s Copaxone patent will indeed expire. However, it is not yet clear whether this would lead immediately to a generic version. It turns out that, due to the very specific chemical properties of this molecule, any generic version might well need separate clinical trials before receiving approval, thereby sharply increasing time-to-market and costs for competitors. This thesis, repeatedly reiterated by Teva’s management, seems to have found some degree of confirmation by the FDA, according to some of their past statements.

3) Immediate threat from recently-launched competing branded drugs

Novartis and Biogen have both recently come up with their own competing drugs for MS, Gylenia and BG12 respectively, which, unlike Copaxone, are both oral drugs.

Gylenia has recently been put to market and clinical trials indicate it is an effective drug, however, there are serious concerns about its safety profile: Gylenia may impact the heart and in some cases be fatal. (For details, check out this report.)

4) BG-12 too seems to be very effective and appears to be initially safer than Gylenia. However, its FDA approval to market was recently delayed for a further three months.

Copaxone’s main disadvantage vis-à-vis its new competitors is its need to be administered by daily injection. This creates discomfort for the patient and cosmetic concerns since it may cause a rash. Gylenia and BG-12 are both oral drugs. While this difference is indeed important, there are a number of factors that overwhelmingly suggest that any shift away from Copaxone, while unavoidable, is likely to be gradual and moderate, rather than massive and immediate.

Copaxone is currently being approved for a higher dose that can be administered three times a week, rather than daily.

Copaxone has a very long history of effectiveness and safety. Its competitors are new to market and only have clinical trials, which are not error-proof.

Copaxone is a so-called “first line drug”. Its competitors, at least for the moment, are still “second line”. That means that patients receive the drugs of the latter type if, and only if, they did not respond to any of the first line drugs. This has to do both with therapeutic history and costs for health insurance companies.

Most importantly, doctors are extremely reluctant to switch a stable patient to a new drug. This last point is paramount and has been hinted at, a few times by Teva’s management. We have made our own inquiries with neurologists in several countries. It turns out that MS is not just a normal disease, but it is characterized by acute episodes that may strike at any time.

The patient typically recovers after each episode, but never to the original level of functioning. In other words, after each acute episode the patient slides one step further down the disability scale. It is therefore of paramount importance to keep patients from experiencing acute episodes. Copaxone reduces the number of acute episodes experienced by patients. Therefore, it would be a bad idea to switch a patient away from Copaxone into a new drug simply because the new drug is oral: if a previously-stable patient does not respond to the new drug, he might well experience a new acute episode and slide irreversibly into a lower level of functioning. Besides, the patient might have adverse reactions to the new drug. This line of reasoning has been strongly confirmed by each and every neurologist we have interviewed.

In light of the three arguments above, we believe that Copaxone is not likely to experience a sharp, sudden decline. It is instead expected to decline gracefully over the years. We expect the bulk of the decline to come from pricing pressures, rather than volume drop.

Copaxone economic impact

Like most other pharma companies, Teva does not disclose the EBITDA margin of its branded drugs (presumably for competitive reasons). Our industry interviews however, suggest that the operating margin on a multi-billion dollar blockbuster like Copaxone should be in the neighborhood of 70%. In addition to this, the company can probably save significant amounts of cash reducing marketing expenses as Copaxone sales begin to ease. Therefore, excluding any savings in marketing, the complete annihilation of Copaxone sales could be worth $2.45bn of Ebitda impact.

Valuation

EV/Ebitda Multiples

It may be difficult to assign a precise value to Teva shares at this moment of uncertainty. However, it would be easy to calculate a minimum floor for the company’s present earnings power, giving the limited information we have.

We have normalized (excluding cyclicality and one-off items) Teva’s EBITDA at approximately $7.5 billion. Main contributors to Ebitda are: generics sale, Copaxone, and branded drugs (excluding Copaxone). We believe that Ebitda from generics should not materially decrease in the foreseeable future. Any margin drop due to new competition and decreasing first-to-file should be more than compensated by gains in volume (industry growing at 8% CAGR) and, eventually, the introduction of biosimilars.

Likewise, branded drugs (excl. Copaxone) should not decrease either. There are no upcoming major patent expirations and, on the contrary, there is a significant pipeline of new drugs about to be launched.

Therefore, we can safely use TTM normalized Ebitda and subtract the expected loss from Copaxone. As we saw earlier, Copaxone Ebitda contribution is roughly $2.5 billion. If we assume that Teva loses approximately half of that contribution over time, normalized Ebitda decreases to 6,250.

Teva EV is $47.9 billion so its EV/Ebitda(norm) is equal to: 7.6X. Teva’s close competitors’ multiples range from 7.9X to 9.88X and average 8.8X, which suggest an undervaluation of 14%.

Present Earnings Power Calculation

Using our normalized Ebitda, subtracting taxes and maintenance CAPEX, we reach a net operating profit after tax (NOPAT) of $4.9. Capitalized at 8%, Teva’s operations are worth approximately $61 billion. Subtracting net debt we reach $48.7 billion or $54 per share, suggesting a 26% margin of safety to current pricing, according to our analysis..

Of course, the above valuation excludes any growth. It is likely, however, that Teva will keep growing considerably in the long term, given its rapidly growing industry and its inherent competitive advantages (low cost production, patent protection). Earnings have been growing at 27% CAGR during the last 7 years. Future growth rates are likely to moderate given Teva’s intention to avoid large acquisitions, Copaxone’s slowdown, and generics uncertainty, but we would expect Teva’s earnings to maintain at least a low double-digit pace for the next 5-10 years.

Risks

We are of the opinion that an investment in Teva at this price represents a moderate-risk opportunity. Teva operates in a stable and growing industry, which is relatively insulated by cyclical and macroeconomic factors. The balance sheet is reasonably strong and management seems experienced enough.

The biggest risk remains a larger-than-expected drop in Copaxone sales due to generic and/or branded competition. However, given our analysis above, we believe that risk to be remote. This is probably the market’s greatest misunderstanding about this company. In addition to this, the generics industry is also undergoing changes and the full impact on Teva’s income statement is hard to forecast with precision.

Finally, investors in Teva must be patient, as it might take time for the market to return valuing Teva at the multiples it deserves. At this point, there seems to be an adequate margin of safety to protect investors entering at this level from crippling losses.

Conclusion

While the overall market is still not overvalued in my opinion, there are very few deep value opportunities available with an acceptable risk: this might be one of them.

Disclosure: The author is long Teva stock.

The investments discussed are held in client accounts as of October 31 , 2012. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or that investment decisions we make in the future will be profitable.

Certain of the information contained in this presentation is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The manager believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.