Author: John Frankola, Vista Investment Management

Author: John Frankola, Vista Investment Management

Covestor models: Core Holding, Core Equity

Stock markets around the globe stumbled in the second quarter, primarily due to sovereign debt concerns in Europe and signs of slowing economic growth in the U.S. and major emerging markets. From its April 2 peak to its low point on June 1, the S&P 500 Index fell by 9.9%. Smaller companies and foreign stocks suffered larger corrections as investors perceived these sectors as having more exposure to a weakening economic environment. A strong 4.0% advance in June for the S&P 500 helped to cut the quarter’s losses.

International stock markets suffered the greatest damage during the quarter as Europe’s economy continued to stall and interest rates for Spanish and Italian government bonds rose to levels that would make it difficult to finance their national debt. While still growing, emerging market economies slowed from the rapid pace of the last several years.

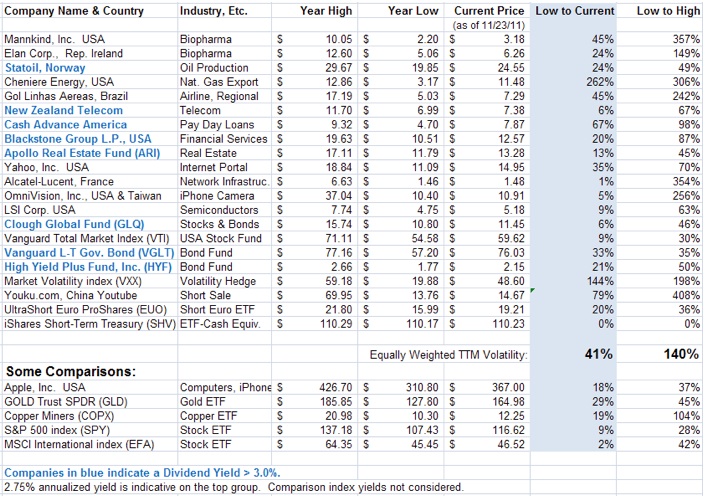

With the best opportunities for growth, the emerging markets and small company sectors offer the highest long-term return potential, but also have the highest risk profile. These two sectors delivered the highest returns over the past 10 years with the emerging markets and small company sectors generating annualized returns of 11.4% and 7.0%, respectively.

However, these same sectors also have higher risk, as demonstrated by the quarter and 1-year returns. Over the past year, the emerging markets and small company sectors have underperformed the S&P 500 by 23.7% and 7.6%, respectively. The dismal performance of developed international markets mainly reflects stagnant economies in Europe and Japan.

During the quarter, equity markets were primarily impacted by news out of Europe. Investors worried about the ability of several European countries to repay their sovereign debt and that a weak European economy could trigger a U.S. recession.

If this scenario sounds familiar, it is a virtual repeat of the conditions that were present in each of the past two summers. And there is some strong likelihood that investors will be worrying about these same concerns next summer. European sovereign debt issues have helped to produce three market corrections in three years.

As various bailout programs are announced, the concerns recede and the markets rally, only to falter again when the problems reappear. No doubt, this situation has caused many equity investors to lose patience, seeing their investments rise and fall with each new headline.

Investors seeking a safe haven from the volatility of equity markets have poured money into U.S. Treasury securities. Demand for Treasuries pushed the yield on the 10-year Treasury bond down to 1.66% at the end of June from 2.22% at the end of March and down from 3.16% one year ago. The BarCap Aggregate Bond Index, which measures the performance of the taxable bond market, generated 2.1% returns during the quarter. The BarCap Municipal Bond Index produced 1.9% returns.

Most of the short-term movement of the stock market is driven by the news of the day. Investors that adhere to a marketing timing strategy attempt to move in and out of stocks based on the expected outcome of near-term events. Recent developments demonstrate how difficult it is to predict the future and also that conventional wisdom is often wrong. Here are some examples:

U.S. Treasuries were downgraded by S&P credit rating services last July from their AAA rating. Normal expectations would be that interest rates would rise on these securities which are now deemed to be riskier. However, the interest rate on the 10-year Treasury bond fell by almost 50% since the downgrade.

Another credit rating agency, Moody’s, announced in February that it was reviewing the credit worthiness of 100 banks around the world. In June, Moody’s downgraded five of the six largest U.S. banks.

Ironically, the Federal Deposit Insurance Corporation recently reported that the U.S. banking industry earned a $35.3 billion profit in the first quarter of 2012, its best quarter since 2007. It was the 11th consecutive quarter that bank profits increased compared to the prior year. The financial sector was a top performing industry sector in the first half of 2012, with total returns of roughly 11%.

The second quarter correction in equity markets came on fears of a global slowdown. The Economist reported that their measurement of global GDP, which includes 52 countries, actually accelerated in the first quarter of 2012 to 2.9%, up 0.1% from the fourth quarter of 2011.

The healthcare care law was upheld by the Supreme Court in a ruling that shocked almost all observers. Chief Justice John Roberts, voting with the four liberals on the court, upheld the individual mandate as a tax, rather than a penalty – an interpretation that no one expected. The ruling caused significant movement in a number of stocks, based on how they were perceived to be impacted by the law going forward.

Just a few months ago, the experts were predicting $5 per gallon gasoline for this summer as the price of oil approached record levels. Instead, according to AAA, gasoline is currently selling at a national average of $3.34 per gallon.

These surprises should teach investors it is almost futile to predict short-term events. As the second half of the year progresses, there is no doubt the market will fret about the outcome of the U.S. presidential election, the expiration of tax cuts, the ongoing problems in Europe, as well as numerous other issues. tocks are likely to exhibit a high level of short-term volatility, due to the many uncertainties and because, more so than in most periods, economic prosperity is dependent on the actions of government officials.

With so many negative headlines, it is often possible to lose sight of the long-term positives for equity investors. However, stocks have excellent long-term return potential when considering that company valuations are very attractive (low price/earnings ratios and high dividend yields), corporate earnings are rising, inflation is low, interest rates are low, corporate and family balance sheets have improved significantly, housing and auto sectors are recovering, and the banking crisis has passed. In addition, alternative investments, such as money market funds and bonds appear to offer unattractive long-term returns.