Author: Bristlecone Value Partners

Author: Bristlecone Value Partners

Covestor model: Large Cap Value

On August 5th, after the market closed, Standard & Poor’s downgraded the United States debt rating from AAA to AA+ with a “negative outlook,” meaning a future downgrade is possible. This news comes on the heels of recent, mostly negative, economic data and this combination has led to what is now a sharp selloff in the stock market. Volatile markets like we’ve experienced cause enormous stress, even to long-term investors. We thought it would be helpful to provide some context.

First, regarding the downgrade, S&P is one of three for-profit agencies accredited by the government to provide credit ratings to companies and governments. The other two are Moody’s and Fitch, and they are not downgrading their ratings on U.S. debt yet. A credit rating is a grade measuring a financial entity’s ability to repay its debt. The downgrade means that S&P sees the U.S. government as less credit worthy today, although still very likely to meet its obligations.

It is not our intent to discuss whether the downgrade was deserved or not. No one will contest that our debt situation is getting worse, and that the will to resolve our country’s fiscal imbalance is a victim of partisan bickering within our government. The downgrade had been expected for a while, and Treasury bond price changes following the downgrade suggest that it was already priced in, but the impact of this decision should not be underestimated. It will have both psychological and financial consequences. It is one more chip that erodes investors’ confidence in our economy and our currency.

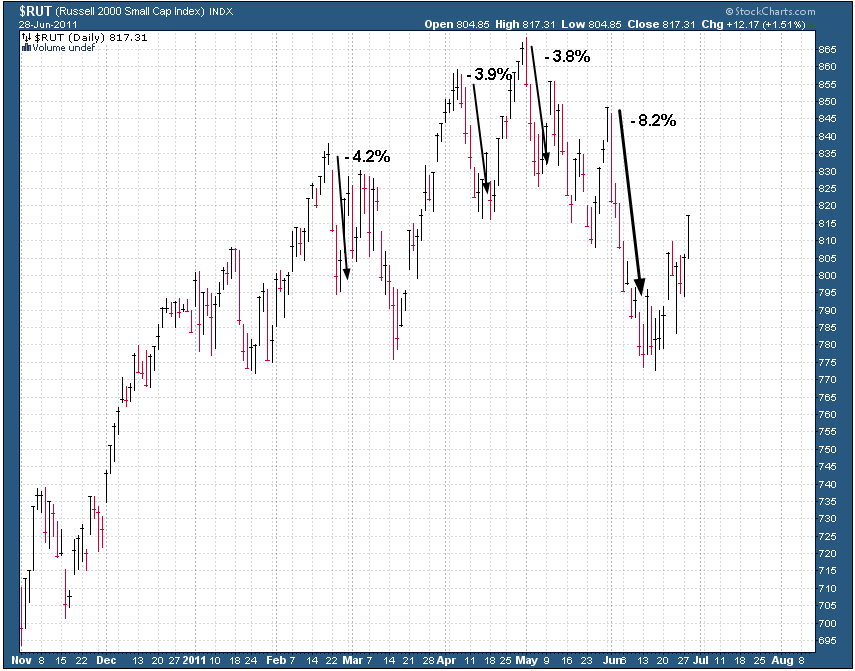

On the other hand, stock markets around the world have reacted negatively, stretching the downward trend of the last three months. Clearly the timing of this unprecedented action could not have been worse, considering that markets were already suffering from increased anxiety. The S&P 500, a broad index of large U.S. companies, is down sharply from its high in April. While painful, this level of correction occurs regularly in the stock market. In fact, a similar drop occurred in the Spring of 2010. It is impossible to know whether markets will quickly recover, as they did last year, or drop further.

The deterioration in our public finances stands in contrast to the health of the average U.S. corporation. Balance sheets are stronger than they were in 2008-2009 and most companies have continued to report higher sales and higher earnings. Although recession remains a possibility, we believe current valuations already somewhat discount that possibility and we remain optimistic about the businesses we own in the portfolio.