By: Steve Sosnick, Chief Strategist

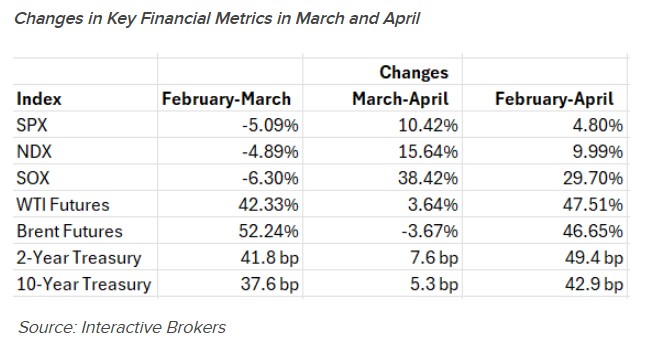

A stupendous April is now behind us.The S&P 500 (SPX) put in its best monthly performance (+10.42%) since November 2020 (+10.75%) and its best April since earlier that same year (+12.68%). The upsurge in the Nasdaq 100 (NDX) was even more stunning. Its +15.64% jump surpassed even its +15.19% jump in April 2020 and was last exceeded by a +18.86% jump in October 2002. Both were abetted by a 38.42% jump in the Philadelphia Semiconductor Index (SOX) – a jump not seen this century!

For reference, the prior records for SOX in the 2000’s were in November 2002 (+26.56%) and October 2002 (+23.89%). Fascinatingly, the moves in SOX in August and November of that year were -20.64% and -22.57%! How about that for some volatility, which indeed resulted in a 4-month gain of 18.22%.

It is stunning to see moves of that magnitude occurring without a significant change in fiscal or monetary policy. We should all remember the massive monetary and fiscal stimuli that occurred in response to the Covid crisis. Stocks bottomed after a sharp drop in March 2020 after the Fed cut its target rate to zero, and then took another leg higher after another bout of fiscal stimulus later that year. In 2002, stocks had been on a downswing for months but bounced when the rate was cut from 2% to 1%.

By contrast, no such monetary stimuli occurred last month. Fed Funds expectations fell sharply in March and didn’t really recover in April. At the end of February, the day before missiles began flying in the Persian Gulf, futures markets were expecting a December Fed Funds target of 3.03%, which is about 60 basis points below the midpoint of the 3.50%-3.75% target. That equates to about 2.4 rate cuts of 25 bp each. By the end of March, that expectation had risen to 3.57%, barely below the current target. As of yesterday, that expectation ticked a little higher to 3.62%, implying no FOMC cuts by year-end.

To be fair, we have seen fiscal stimulus work its way into markets this year, though none of it was new. The effects of the “Big Beautiful Bill” are indeed being felt by companies whose earnings reports are being bolstered by the tax savings that were engineered last year. Of course, we need to consider the fact that this year’s robust earnings expectations already factored in this expense reduction. There was indeed an incremental improvement above and beyond the anticipated first quarter earnings, and apparently investors believe that to be sufficient for stocks to ignore the lack of new monetary and fiscal stimulus that normally powers moves of the magnitude we experienced in April.

The table below shows that stocks rallied despite no marked improvement in key exogenous factors in April. Indeed, the moves in March were quite stunning, with huge jumps in oil futures and bond yields leading to declines in stocks. Yet the rallies in stocks occurred despite no improvement, and in fact a modest worsening, of most of those measures.

Perhaps we can chalk this up to a key feature about market reactions to geopolitics. We have long asserted that stock markets are not particularly adept at pricing in geopolitical risks as compared to their commodity and fixed income counterparts, especially when there is little direct impact from global events upon stocks’ revenues, earnings, and/or cash flows. In the case of the closure of the Strait of Hormuz, we know that outside of a few commodity-related stocks, there is little good news to come from that event. But it is also quite difficult to quantify the negative effects. Higher oil and fertilizer prices could certainly have stagflationary effects, and a disruption in the global helium supply could impede the already tight supply of global semiconductors, but we’ve heard little specifically about those factors from corporate management during earnings calls.

And why should they say anything about them? These factors might eventually affect earnings, but why should a CEO or CFO mention potentially uncomfortable topics before they need to? It seems prudent for investors to consider these factors in advance, but the current upsurge is undoubtedly pushing concerns about an uncertain future to the background in favor of seemingly endless rallies. At some point, if the situation in the Gulf fails to improve, we will all need to reckon with its effects upon stock valuations. But I suppose it seems imprudent for momentum-driven investors to do that now.

Originally posted on May 1, 2026 on Traders’ Insight

PHOTO CREDIT: https://www.shutterstock.com/g/NVA13

VIA SHUTTERSTOCK

DISCLOSURES

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

{kind=link}