By: Jose Torres, Senior Economist

Traders came back from the holidays in high gear with stocks soaring and the Dow Jones Industrial Average reaching a fresh record. An eventful weekend featuring the ousting and arrest of communist Venezuelan dictator Nicolas Maduro is generating outperformance in the energy sector as the US oil majors are poised to benefit from Washington’s control of the crude rich nation. There are risks, of course, that international relations could worsen with Moscow and Beijing, allies of Caracas, especially regarding potential implications for Kyiv and Taipei, but Wall Street isn’t worrying and is instead focusing on a buoyant economic outlook alongside robust corporate-earnings expectations.

Stocks, Treasuries Rally

Not even the weakest ISM-manufacturing print of 2025 could derail the enthusiasm, as benchmarks continued to advance following the release. The publication modestly raised slowdown concerns, however, reversing the greenback’s notable gain while driving bids for Treasuries with the yield curve sinking in bull-flattening motion led by duration. Risk-on attitudes are coinciding with some investors that are wary of potential bumpiness down the road, causing the prices of volatility protection instruments to rise slightly as participants add portfolio hedges. Conversely, though, shares in the defensive utilities, consumer staples and healthcare sectors are selling off. Elsewhere, cryptos are regaining their footing and forecast contracts are experiencing interest while prices of commodities ex natural gas appreciate.

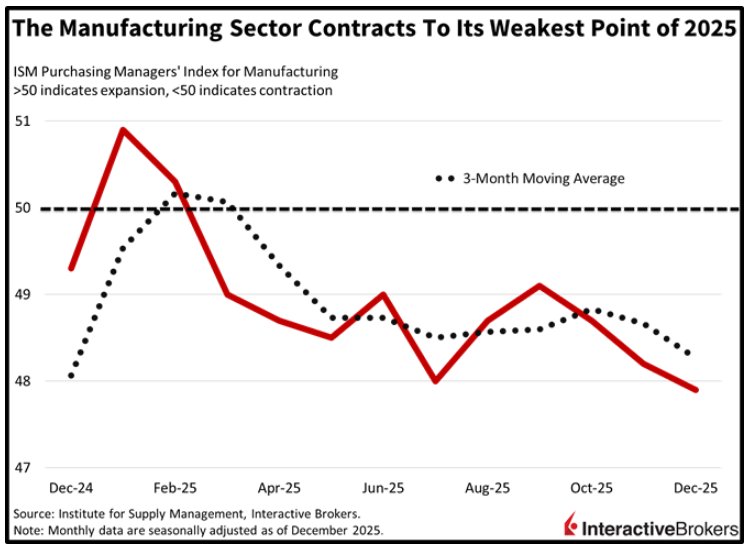

US Manufacturing Sinks to Weakest Level of ’25

Broad manufacturing sector weakness caused the Institute for Supply Management’s (ISM) Purchasing Managers’ Index to sink to its weakest reading of 2025. The headline December score of 47.9 fell below the contraction-expansion threshold of 50, the median estimate of 48.3 and November’s 48.2 result. Persistent losses in employment, new orders, exports and work backlogs continued to weigh on overall performance with those segments reporting dismal figures of 44.9, 47.7, 46.8 and 45.8. Prices increased at the same 58.5 pace as the preceding print, but elevated costs combined with lofty interest rates continued to hamper transaction momentum. However, factory activity could improve significantly because 100% first-year tax depreciation on capital expenditures kicks into gear this year, incentivizing investment, production and hiring.

Maduros’s Capture Is Great for Inflation Expectations

The capture of Maduro over the weekend bodes well for Treasury bulls and Fed doves via lighter inflation expectations as Washington’s actions in Caracas lead to greater control over energy supplies in the Western Hemisphere. The military operation, paired with heavy production and subdued regulations in the US, are supportive of a continuation of low crude oil prices and reduced OPEC+ influence on total available barrels. The events are net positive for global economics and corporate profitability, especially in consideration of the rising power requirements of artificial intelligence. But there are risks associated with potential retaliation from Beijing and Moscow against the backdrop of those regimes craving land expansion of their own and possibly using the developments in Venezuela as a justification to ignore US priorities and warnings.

International Roundup

China’s Service Sector Growth Slows

China’s service sector’s growth in December decelerated to the slowest pace since June with the S&P Global RatingDog General Services PMI falling from 52.1 to 52. The result matched the economist consensus estimate while remaining above the contraction-expansion threshold of 50, thereby extending the expansion to three years.

Declining export orders and tourism from foreigners caused overall sales to slow and strong competition resulted in businesses lowering their output prices. Conversely, input costs climbed due to labor and raw materials becoming more expensive. Despite these challenges, business confidence hit a nine-month high. Nevertheless, restructuring and costs resulted in the fifth consecutive month of staff reductions, which contributed to a slight increase in backorders.

Singapore Retail Sales Were Flat Relative to October

November retail sales in Singapore were flat relative to October but were still up 6.3% year over year (y/y), according to the Singapore Department of Statistics. The monthly metric slowed from 2.3% in October while the y/y result was up from the preceding period’s 4.4% print. Excluding motor vehicles, retail sales grew 0.8% in November, a decline from October’s revised 3% expansion. Cash register activity climbed m/m by the stated amounts in the following groups:

- Petrol services stations, 13.2%

- Wearing apparel and footwear, 6.4%

- Computer and telecommunications equipment, 4.5%

- Furniture and household equipment, 4.5%

- Mini-marts, 3.5%

- Cosmetics, toiletries and medical goods, 2.9%

- Food and alcohol, 2%

- Department stores, 1.9%

However, the following categories and the extent of their declines pushed the headline down:

- Watches and jewelry, 11.4%

- Motor vehicles, 4.9%

- Recreational goods, 5.7%

- Optical goods and books, 1.2%

Despite Tax Angst, UK Consumer Financing Grew in November

The long-awaited Nov. 26 unveiling of the UK’s tax hikes didn’t appear to thwart household outlays with debt issuance during the same month jumping by a net 2.08 billion pounds ($2.79 billion). It was the largest increase in two years, according to the Bank of England. Both mortgage finance and consumer debt increased m/m as follows:

- Mortgage issuance was up £4.5 billion after falling £1.0 billion to £4.2 billion in October. The number of loans for purchases sank by 500 to 64,500 with the bulk of the net increase resulting from remortgaging approvals ascending by 3,200 m/m to 36,000.

- Consumer credit expanded by £2.1 billion following a £1.7 billion jump in October. Credit card financing was £1.0 billion higher in November. The metric climbed £0.7 billion in the preceding month. Other forms of borrowing, such as auto and personal loans, increased by £1.1 billion compared to the £1.0 billion growth in October.

In late November, Chancellor of the Exchequer Rachel Reeves submitted a budget that includes the eventual phase in of £26 billion of tax hikes for plugging funding shortfalls. The changes include fees for online gambling, miles driven by electric vehicles, and charges for owners of properties exceeding £2 million in value. She also slapped a cap on the amount of income that workers can shelter from National Insurance premiums via the country’s pension program. The country’s Office for Budget Responsibility estimates that nearly one in four taxpayers will pay some of the higher levies by 2031.

Originally posted on January 5, 2026 on Traders’ Insight

PHOTO CREDIT: https://www.shutterstock.com/g/DanielTarrago

VIA SHUTTERSTOCK

DISCLOSURES

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Digital Assets

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Disclosure: Forecast Contracts

Forecast Contracts are only available to eligible clients of Interactive Brokers LLC, Interactive Brokers Canada Inc., Interactive Brokers Hong Kong Limited, Interactive Brokers Ireland Limited and Interactive Brokers Singapore Pte. Ltd. Forecast Contracts on US election results are only available to eligible US residents.

Disclosure: Forecast Contracts Risk

Futures, event contracts and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy visit our Warnings and Disclosures Page.

{kind=link}