By: Jose Torres, Interactive Brokers’ Senior Economist

Demand for services is continuing to keep the labor market tight and drive inflation with job creation in June more than doubling analysts’ expectations and the latest ISM PMI-Services release reporting that economic growth within the category is accelerating. Surprisingly strong results from this morning’s ADP jobs report illustrate that travel, entertainment and restaurant businesses are struggling to meet the robust demand that is supporting persistent inflation. At the same time, job creation is likely to intensify inflation in the services sectors, which are labor intensive, as newly hired individuals spend a portion of their incomes on entertainment, traveling and dining out. Additionally, with an already tight labor market, the new jobs are likely to support, or even intensify, wage pressures and sustain a trend of companies increasing their prices to pass higher compensation costs on to customers.

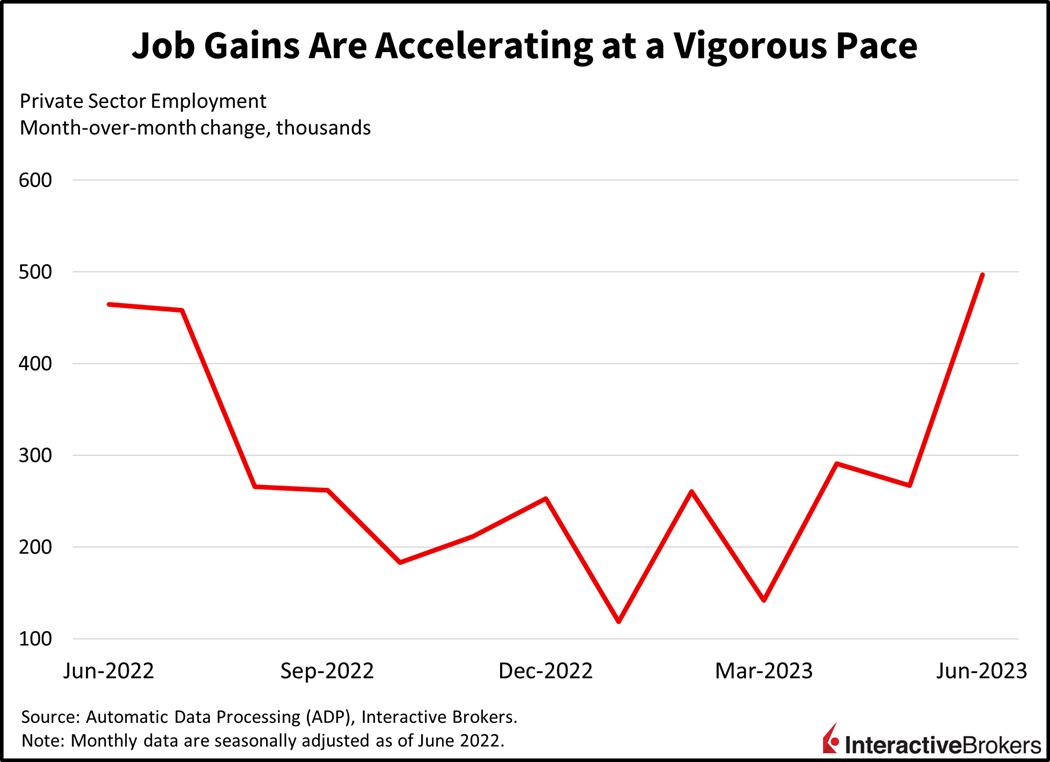

Service Sectors Drive Strong Job Creation

Despite the Federal Reserve’s aggressive monetary policy tightening, the private sector added 497,000 jobs in June, blowing past the analyst expectation of 228,000 and the 267,000 jobs created in May. The data confirms concerns among policymakers about wage pressures fueling inflation. While the year-over-year change in wages for job stayers dropped from 6.6% to 6.4% during the period, it remains far too elevated. These concerns were reinforced in yesterday’s release of minutes from the Fed’s June meeting. The minutes revealed that various members of the Federal Open Market Committee would have voted in favor of raising rates last month because of fears that a tight labor market will support persistent inflation.

The ADP report showed that leisure and hospitality accounted for the largest employment gain, creating 232,000 jobs. In another surprising development, construction accounted for the second-largest gain, with 97,000 jobs created despite a 30-year average residential mortgage fixed rate of 7.22%, up from a historical low of 2.67% in 2021. Additionally, regional banks that have been the mainstay of financing for commercial real estate construction have tightened their lending requirements. Still, onshoring trends and demand for new homes provide bright spots for the ailing real estate sector. Trade, transportation and utilities was the third-largest gainer with 90,000 positions added.

Growth in Services Accelerates

This morning’s ISM PMI-Services June score of 53.9 also depicted strong economic growth. The result exceeded the analyst expectation of 51 and climbed substantially from 50.3 for May. The sector has grown in 36 of the last 37 months. Services employment grew at a 53.1 index level, higher than the 49.2 from the previous month. Furthermore, May job openings remained persistently high at nearly 10 million, declining only slightly to 9.82 million from 10.32 million in April. The consensus estimate was closer to 9.94 million.

Impact of Tight Labor Conditions

While a tight labor market is helping employees secure raises as employers compete for workers, UPS and the Teamsters Union are struggling to reach a new contract for some approximately 340,000 full-time and part-time drivers. Negotiations broke down yesterday and the union is believed to be moving closer to striking. Efforts by the union for a more generous contract may represent employees having increased negotiating clout as employers struggle to find and retain workers. If UPS employees eventually win sizable pay increases, other unions may become optimistic that they, too, have more clout for negotiating bigger pay raises then they would with a weak job market.

The tight labor market and wage pressures have been a focus for Fed Chairman Jerome Powell and other central bankers. Minutes from the central bank’s June 13-14 meeting released yesterday reveal that various policymakers supported raising the fed funds rate 25 basis points rather than the agreed upon pause. Policymakers maintained that a strong labor market is supporting price increases, and inflation, as measured by the core Personal Consumption Expenditures Index, which doesn’t include food or energy, hasn’t changed significantly from last December’s 4.6% rate and is significantly above the Fed’s 2% target.

The minutes underscore that the Fed is prepared to raise the fed funds rate 25 bps to a target of 5.25% to 5.50% during its July 25-26 meeting. Powell has said the decision to pause reflects the rapid pace at which the central bank has raised rates rather than a belief that it’s appropriate to back away from a hawkish stance. The fed started its hawkish policy last year with four consecutive 75-bp rate hikes before slowing the pace of its tightening. Due to this fast pace, Powell said it’s appropriate to pause rate increases to give the Fed’s tightening time to work and to better assess the impact of the tightening.

Market Sentiment Tanks

Markets are plunging today as ferocious job growth propels Fed tightening prospects alongside inflation expectations. Yields are higher across the curve led by the mid- to long-ends. The 2- and 10-year Treasury yields are up 12 bps each to 5.07% and 4.06%. The Dollar Index rebounded from lows following this morning’s economic data and is now unchanged on the day. Weighing on the dollar earlier and propping up the euro was an unexpected surge in May factory orders out of Germany. Stocks are tanking with all major indices and sectors in the red. The Russell 2000 Index is leading the way lower, declining 2.6% while other major indices are down about 1.5%. The outlook for higher-for-longer interest rates is weighing on the demand outlook for energy, with WTI crude oil paring recent gains. It’s down 1.2% to $70.90 per barrel.

Markets Face a Bigger Wall of Worry

Today’s data underscore the threat of higher rates to the equity market’s elevated valuations. With inflationary dynamics remaining momentous and sticky, we continue to believe rates will drift higher in the next few weeks, with last Friday’s commentary calling for today’s move on 2 and 10-year yields north of 5% and 4%. Furthermore, tomorrow’s Employment Situation from the BLS will provide additional clarity on employment conditions and be carefully scrutinized by the Fed. Following this morning’s data, odds for a second 25-bp hike in the second half of this year moved up to 38.6%, reaching a terminal mid-point rate of 5.63% at the November meeting.

This post first appeared on July 6th, 2023 on the IBKR Trader’s Insight blog

PHOTO CREDIT: https://www.shutterstock.com/g/Rawpixel

Via SHUTTERSTOCK

DISCLOSURE: INTERACTIVE BROKERS

Information posted on IBKR Campus that is provided by third-parties and not by Interactive Brokers does NOT constitute a recommendation by Interactive Brokers that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with permission from IBKR Macroeconomics. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and IBKR is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation to buy, sell or hold such security. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

In accordance with EU regulation: The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Any trading symbols displayed are for illustrative purposes only and are not intended to portray recommendations.

{kind=link}