By Chelsea Rodstrom, Research Analyst, Global X EFTs

Recently we spoke with Wei Xu and Zhen Wei from MSCI about market developments in China. Read our Q&A to learn more about MSCI’s perspective on China’s performance against developed and developing markets, China Sectors, A shares, and the impact of COVID-19.

How has China’s performance compared to both developed and developing markets over the past 10 years?

There’s little doubt that both China and its equity market have evolved.

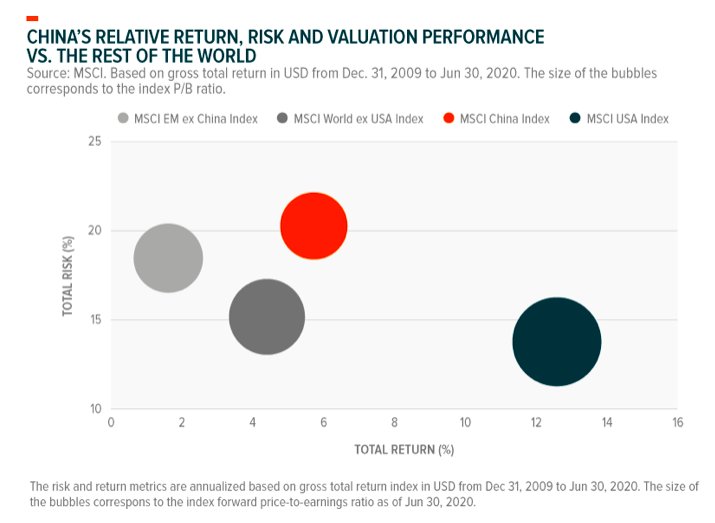

The following chart shows the historical annualized return and volatility of the MSCI China Index and other major global indexes from Dec. 31, 2009 to Jun 30, 2020. During this period, China outperformed both emerging and developed markets (ex U.S.) but experienced higher volatility. Yet, China underperformed the U.S. in equity market performance.1 In addition, the recent index valuation of the MSCI China Index, as measured by the index-level forward Price to Earnings ratio (represented by the size of the bubble below) was lower than that of the MSCI USA Index.

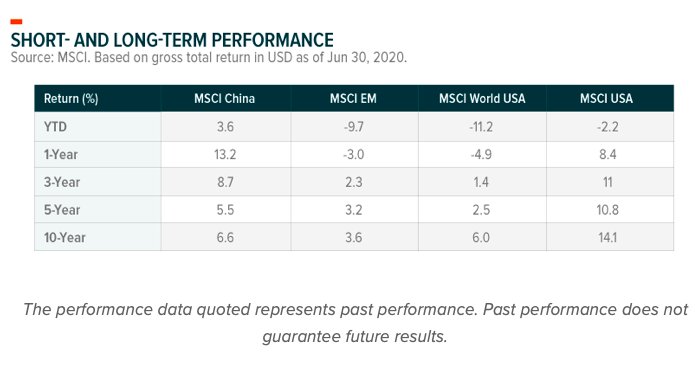

Over the past one to three years, China outperformed global equity markets broadly, with the MSCI China Index having outperformed the MSCI USA Index by almost 10% in the first quarter of 2020.

The performance data quoted represents past performance. Past performance does not guarantee future results.

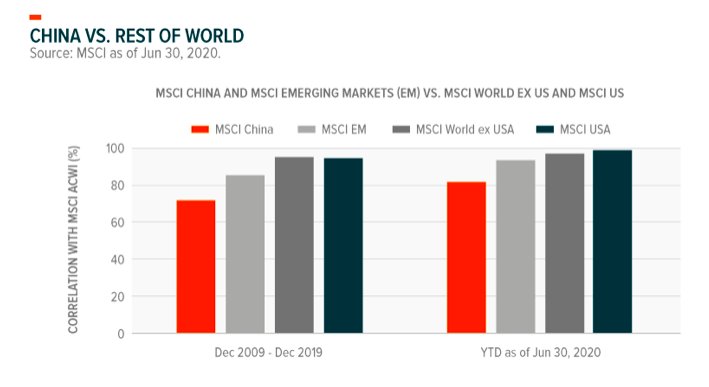

In addition, China continued to demonstrate diversification features in the long-term and near-term. Over the last 10 years through December 2019 and year-to-date, as of June 2020, the MSCI China Index displayed lower correlations with global markets, as represented by the MSCI ACWI Index compared to those of other major markets.

What factors have driven performance in China over the last 10 years?

There have been three primary drivers of China’s relative performance.

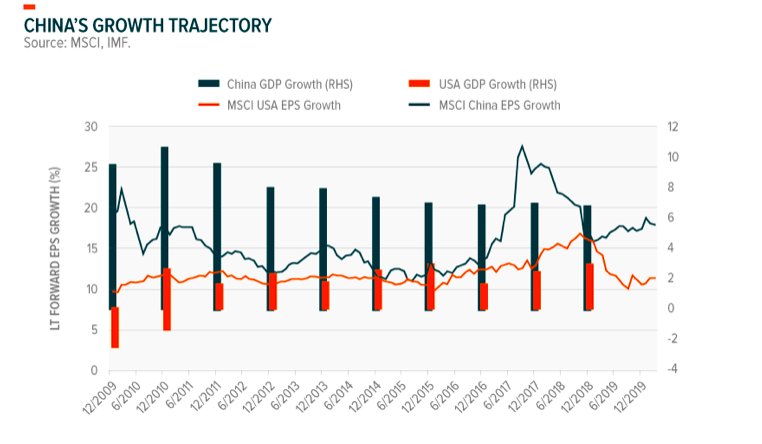

1. Economic and Earnings Growth: Capital market performance is often a reflection of economic growth and earnings growth.2 China enjoyed high levels of economic growth during the past 40 years, making it the world’s second largest economy. Although its annual GDP growth has slowed since 2011, average real GDP growth in China steadied around 8% over the last decade.

2. Evolution of the Sector Composition: As the Chinese equity market evolves, global investors face new choices. They can continue with broad allocations to emerging markets (EM), choose slightly narrower allocations to China and other specific EM countries, or consider targeted investments within China through new means, such as factor-based systematic strategies or sector investing, which have provided diversification in developed markets. In our research, we found that China had the three key attributes we’ve seen sector investors look for in their allocations:

- Low correlation – particularly between cyclical and defensive sectors

- Differences in fundamentals, such as earnings growth and dividend yield

- Geographic differences that reflect differences in firms’ sources of revenue

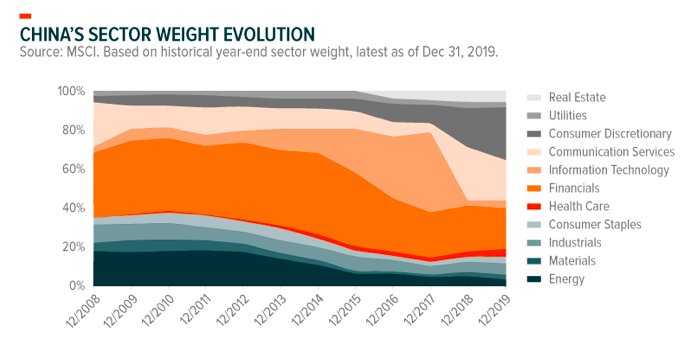

The MSCI China Index has undergone large-scale changes in its sector composition over the past 10 years. Information Technology has increased from 3% to 41% before the Global Industry Classification Standard (GICS®) structure change.3 The Communication Service and Consumer Discretionary sectors rose from 5% and 3% to 21% and 27%, respectively, following the GICS reclassification. Financials and Energy declined from highs of 42% and 18% to 21% and 4%, respectively.

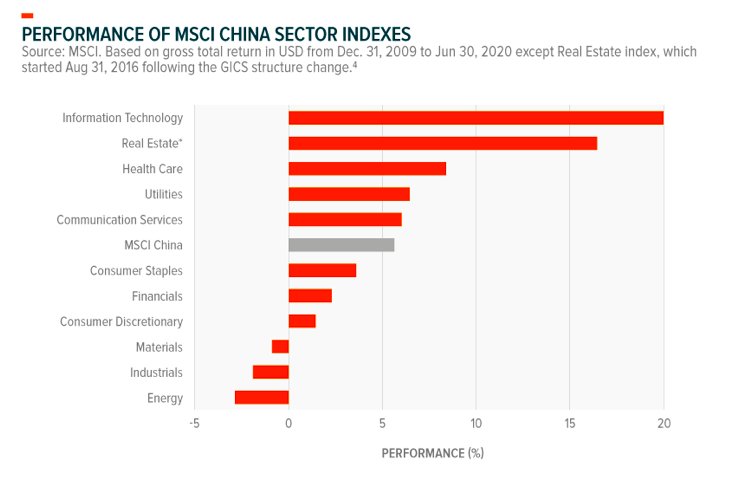

Evolution of the sectors in listed companies reflects the evolving underlying economy: China has been shifting from a government spending-fueled ‘old economy’ to a high-tech and consumption-driven ‘new economy.’ During the past decade, Information Technology, Real Estate, Utilities, and Healthcare were top-performers among all the sectors.

The performance data quoted represents past performance. Past performance does not guarantee future results.

3. Foreign Listings and China A-Share Inclusion:

A distinctive feature of the Chinese equity market is the number of different share classes and exchange listing locations. The MSCI China Index covers all investable share classes and is designed to represent the performance of the integrated Chinese opportunity set.5

In the 2015 November MSCI Semi Annual Index Review, foreign listed companies started to be included from eligible countries into the MSCI China Index. The number and size of U.S. listed Chinese companies is significant. Home-grown Chinese companies like Alibaba, Tencent and Baidu were also added into the MSCI China Index as at the close of November 30, 2015.

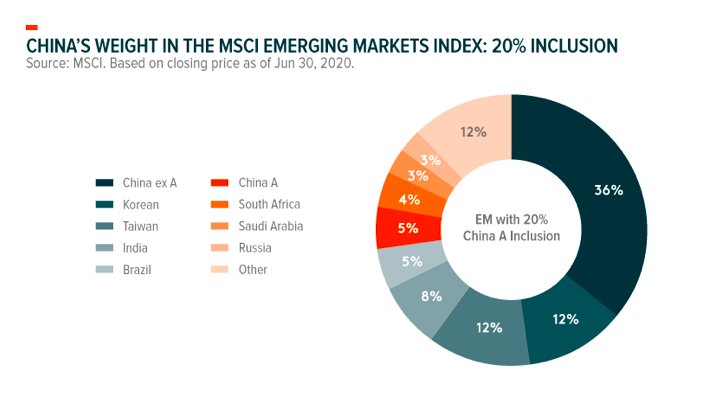

The partial inclusion of China A-shares into the emerging market universe further shaped China and global equity market indexes. China A shares are included at 20% of their free-float market cap. China represented about 28% of the MSCI Emerging Markets Index in June 2017, roughly equal to the total weight of South Korea and Taiwan. With the 20% inclusion of China A shares, China’s constituents’ total weight increased to 41% of the MSCI Emerging Market Index, as of June 31, 2020. This was higher than the weight of South Korea, Taiwan and India combined.

The initial inclusion of China A-shares in the MSCI Emerging Markets Index may have also encouraged foreign institutional investors’ participation in China’s domestic equity market.

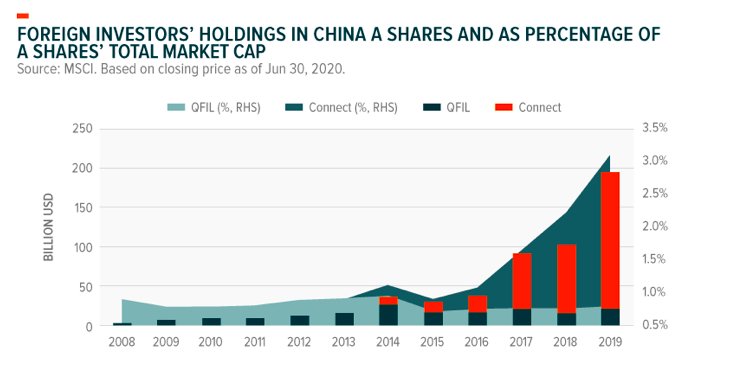

The exhibit below shows that foreign investors’ participation in the market for China A-shares has increased since 2017: Non-Chinese holdings of China A shares rose from USD 38 billion (0.67% of the market total in December 2016) to more than USD 195 billion (3.03% in September 2019). International institutional investors have become more significant participants in the A share market with their increased holding of the share class.

RHS refers to the right hand side. The bars in the chart represent the USD dollar amount of A shares held by foreign investors. The blue bar represents foreign holdings through QFII channel, and the red bar represents foreign holdings through the connect channel. The area in the chart represents the percentage of A shares held by foreign investors. The grey area represents foreign holdings percentage through QFII channel, and the green area represents foreign holdings percentage through connect channel.

What were the implications of COVID-19 for China specifically and the global economy more generally?

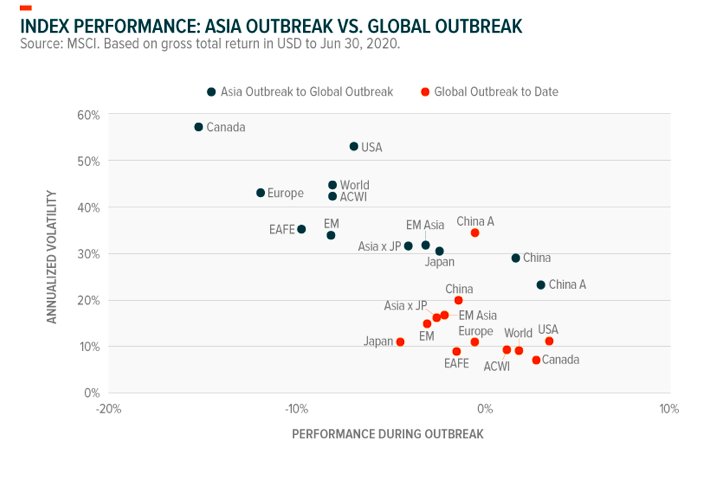

The outbreak of COVID-19 in China became global news in January. From Jan. 10, 2020, to Feb. 21, 2020 (Phase I), the MSCI China Index underperformed the MSCI ACWI Index while the MSCI USA Index and MSCI World Index outperformed.6 Since the global spread of the virus from Feb. 21 (Phase II), we’ve seen the highest global volatility spikes since the 2008 Global Financial Crisis. Regional volatility and performance led to wider dispersion. However, the MSCI China Index outperformed other equity markets after the global outbreak, as new cases decelerated in China.

In the first quarter of 2020, the coronavirus pandemic presented some downside risks to China’s economic growth, as consumption fell because of business closures and travel bans. However, China’s experience with the 2003 SARS pandemic, demonstrated that quarterly GDP growth, retail sales growth, and revenue from tourism, bounced back quickly as businesses resumed operations.

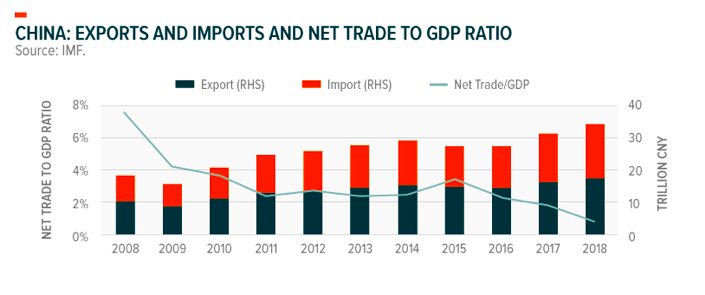

Longer-term, the pandemic could hamper global trade. After China focused on the expansion of its manufacturing output and capabilities for decades, it became known as ‘the world’s factory’, exporting goods and components across the world at competitive prices. In 2008, China’s exports were much higher than its imports and net trade was almost 8% of China’s GDP. But over the past 10 years, China’s imports grew quickly, reducing the net trade-to-GDP ratio and making it less dependent on the export economy. While the impact of the coronavirus on China’s trade could be significant, the net impact to GDP may be lower than expected because of the low net trade to GDP ratio.

In the chart above, “RHS” refers to “right hand side” and CNY refers to Chinese Yuan.7

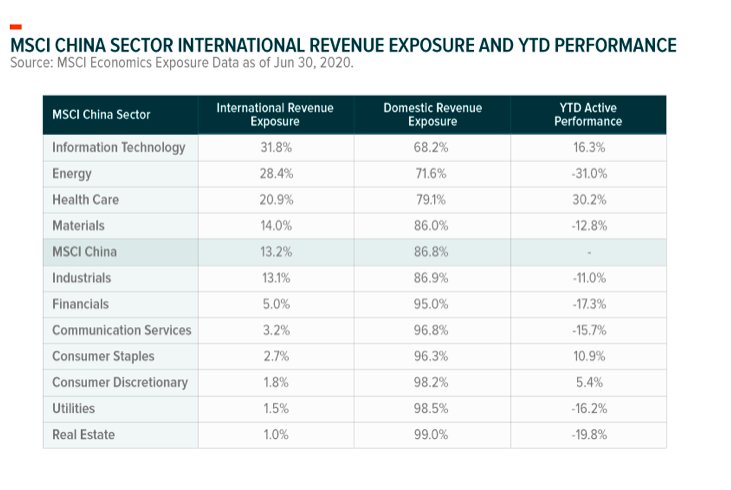

From a revenue exposure perspective, overall China’s international revenue exposure was relatively low: Roughly around 12.6% of its total revenue came from overseas, while the MSCI USA Index and MSCI Europe Index had 30% and 40%, respectively, of revenues generated from the rest of the world. Globally, Information Technology and Energy had the highest foreign exposure among all the sectors, as of Jun 30, 2020.

The performance data quoted represents past performance. Past performance does not guarantee future results.

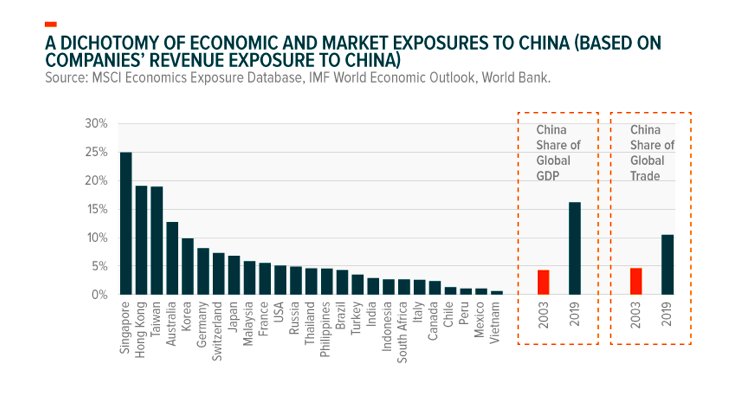

On the flip side, the global economy has become much more dependent on trade with China. Based on statistics from the World Bank, China’s share of global trade rose from 5% in 2003 to 11% in 2019.

Photo Credit: Mathias Apitz (München) via Flickr Creative Commons

FOOTNOTES

1. MSCI China Index outperformed MSCI Emerging Markets Index and MSCI World ex USA by 3% and 1% respectively. The MSCI USA Index outperformed the MSCI China Index by 6.5% over the same period.

2. Effective in 2018 together with the November semi-annual index review, the GICS structure was revised to reflect the evolution in the mode in which people communicate and access entertainment content and other information. This evolution is a result of the integration between telecommunications, media and internet companies. Companies like Google, Facebook, and Baidu moved from IT to communication services; E-bay and Alibaba moved from IT to consumer discretionary. More details of the GICS reclassification in 2018 can be found on the MSCI website: https://msci.com/gics

3. Effective in 2016 together with the August quarterly index review, Real Estate was promoted to a Sector, the first additional Sector to be added to the GICS structure. This change highlights the fact that real estate is viewed as a distinct asset class and a growing part of global economies.

4. Opportunity set refers to different share classes, with overseas listing and A share inclusion, China opportunity set become more complete.

5. WHO issued first situation report on Jan 10; starting from Feb 21, daily new cases outside of China exceeded 200 and started to increase on a daily basis, while daily new cases in China reached their peak. See: WHO, Coronavirus disease Situation Reports, Jun 2020.

6. WHO issued its first situation report on Jan 10; starting from Feb 21, daily new cases outside of China exceeded 200 and started to increase on a daily basis, while daily new cases in China reached its peak. Please see: https://www.who.int/emergencies/diseases/novel-coronavirus-2019/situation-reports/

7. The bars in the chart represent the USD dollar amount of A shares held by foreign investors. The blue bar represents foreign holdings through the QFII channel, and the red bar represents foreign holdings through the connect channel. The area in the chart represents the percentage of A shares held by foreign investors. The grey area represents foreign holdings percentage through QFII channel, and the green area represents foreign holdings percentage through connect channel.