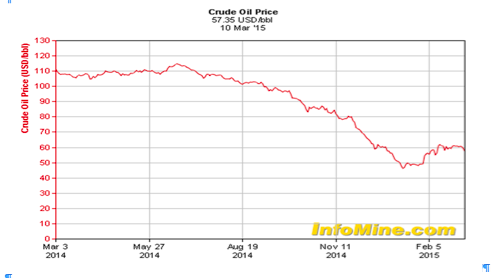

My main premise behind the current positioning of the TenStocks portfolio is this: At some point in the next 18 months, I believe the price of West Texas Intermediate oil (WTI) will sell for $70 to $80 a barrel.

As I write this, WTI is going for around $50 a barrel (as of March 13) after touching a recent low in the mid-40s. The drop from $110 last year has been swift and painful.

Energy Sector

Anyone who has followed my work over the last few years will know, I am well accustomed to pain. In fact, I’m starting to feel like Dustin Hoffman in the Marathon Man dentist scene.

And, just like in the movie, the question, “Is it safe?”, seems apt when considering investments in today’s energy sector. It definitely hasn’t been safe for the last six months or so.

Price Slump

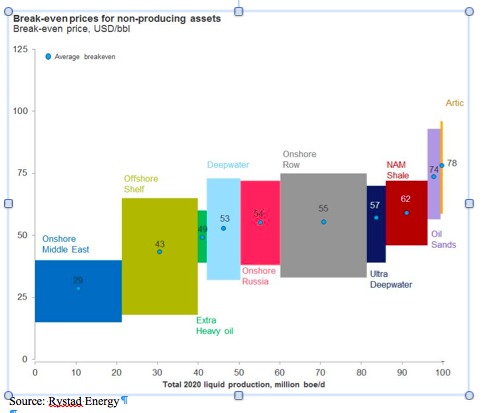

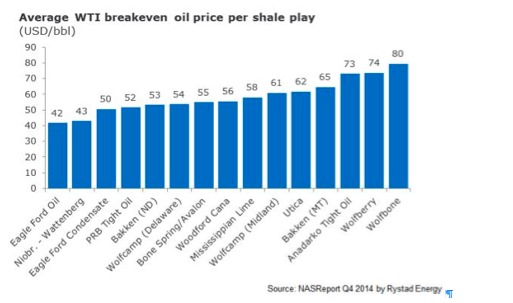

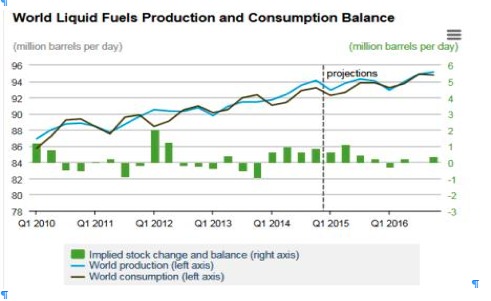

So let’s take a look at the next two charts. At somewhere around $50 a barrel, roughly half of global supply is losing money.

Imbalance

Much has been made of a global oil glut, but the current supply/demand imbalance is only around 2%.

The sudden downdraft in oil pricing was caused mainly by Saudi Arabia and the Gulf States. As the low cost producers at around $30 a barrel, their main aim is to inflict damage on higher cost producers.

Shale Boom

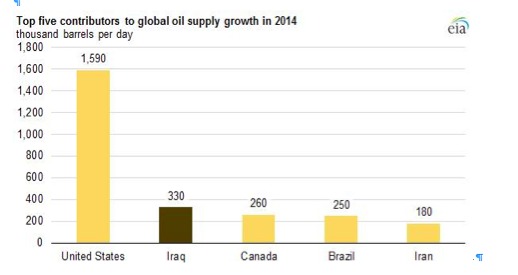

In doing so, they hope to restrict their access to, and raise the cost of, their needed capital. The U.S. shale boom has been the only real global source of recent supply growth.

This boom in U.S. production has been largely financed by cheap capital and easy loan terms.

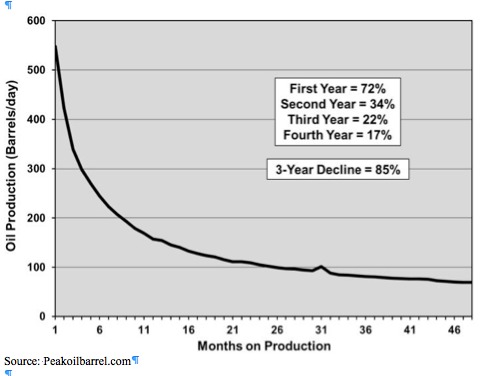

U.S. shale production per well declines roughly 65% in the first year and some think it’s higher than that.

By the third year, production per existing well slows to a trickle. In order to keep production flat, shale drillers need to be constantly drilling new wells, and constantly need new capital to fund them.

They are also drilling the most productive, economical wells first, then moving down the quality ladder with each new well.

Undercutting Shale

When Saudi Arabia and friends send a message to the financiers that with one press conference they can chop the knees out from under the shale guys and endanger their capital.

That matters because the supply of that capital is likely to get harder to find, and the cost and terms of getting that capital will go up.

This in turn will raise the break-even price for the shale drillers who can find capital.

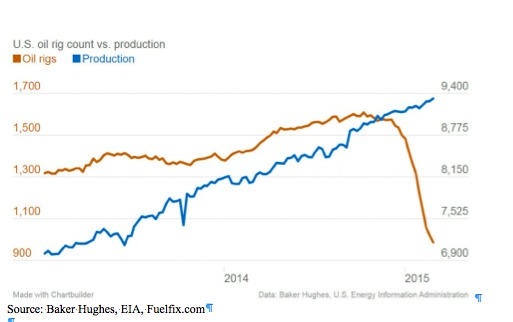

Right now U.S. shale is in supply contraction but falling production numbers probably won’t start showing up in the data for another three months.

But early signs of a pullback in U.S. shale are evident now. Rigs are being laid down.

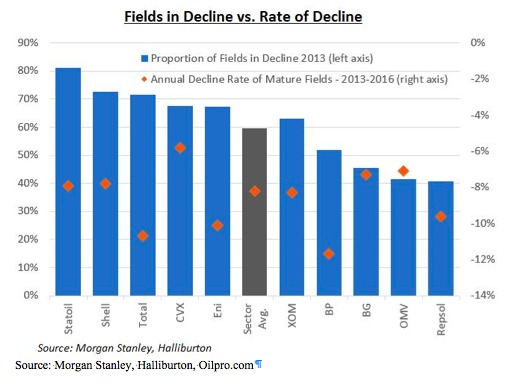

Shrinking Production

Worldwide fields are in decline, according to data in the next chart.

On the demand side, global demand increases, on average, roughly 1% a year.

This is roughly in line with population growth; hence most demand growth comes from emerging countries where there is a higher birth rate.

Historically, as the price of oil comes down, demand increases. In my opinion, we are at, or close to, a tipping point in the supply/demand equation.

New Balance

In my opinion, the global equilibrium price of oil is in the $70-80 area. This is the oil price I think is needed to keep supply and demand roughly in balance.

I have been building positions in Canadian oil and gas reserves through Penn West Energy (PWE). Penn West is in the midst of a negative perfect storm.

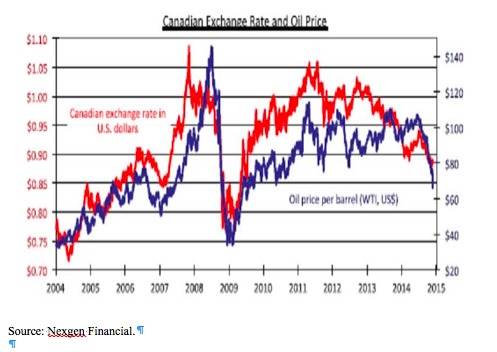

Our ownership position has cost us a couple of root canals and a few wisdom teeth. The Canadian dollar is linked to its resource-backed economy. When oil drops in price so does the Canadian dollar.

Currency Play

A lower Canadian dollar benefits Canadian producers as their costs are in local currency while their product is priced in U.S. dollars.

Also, I’m taking marginally overvalued U.S. dollars (there is a relationship between a rising U.S. dollar and falling oil prices) and investing into both a cheaper currency and a cheaper asset.

PWE is a resource-rich land bank. Right now there are fears PWE will violate their loan covenants. There are a lot of shorts betting against the company and they are driving down the market price by selling borrowed stock.

Contrarian Bet

They will have to buy the stock back if they are wrong. Obviously, I think they are wrong.

While currently close to tripping loan covenants, I think they will be able to renegotiate the terms of their debt and survive to see both a higher oil price and a higher stock price (PWE covenants have since been amended).

Meanwhile, with PWE selling at less than $2 a share, it is vulnerable to a takeover due to the value of its underlying assets.

Ensco

Another holding, Ensco (ESV) is an offshore driller. Again it’s got beaten up due to the sell-off in oil. While shale is short-lived, offshore fields are more durable and can produce for many years.

Because of the time-frame and investment needed for each new field, they are more often tied to long term, multi-year contracts. These large scale capital-intensive projects don’t get based on short term oil price movements.

They are based on longer term average price expectations. I own ESV because I’m looking past current oil pricing. The world will need more oil in the future and offshore is one place where the big, long-lasting projects will be.

Exco Resources

Exco Resources (XCO) is yet another holding and it enjoys a large energy resource base. Primarily a gas play, it stands to benefit from the export of U.S. gas to Europe and other places in my opinion.

There is a wide spread between U.S. gas prices and the rest-of-world gas price because U.S. gas is currently somewhat land-locked.

I believe that when exports pick up with terminal completions, demand for U.S. gas abroad—especially in Europe—should be high.

Meanwhile XCO’s share price is getting hit along with anything else connected to energy. Exco offers another lesson too: Even famous investors can make big investment mistakes.

XCO’s insider’s roster at the end of the 2015 contained a veritable who’s who of respected and famous investors, all of whom have taken a bath in this stock (so far).

Wilbur Ross of WL Ross and Co. is one, Howard Marks of Oaktree Capital is another, and Fairfax Financial’s Prem Watsa, widely referred to as the Warren Buffett of Canada, is still another.

Brazilian Iron Ore

Vale (VALE) is a Brazilian iron ore producer. Some time ago, Rio Tinto (RIO)—and Vale according to some—decided to drive higher cost producers out of business by flooding the market with iron ore.

Rio and Vale are the pure play low cost producers. If you see similarities to the Saudi actions you’re not alone. Watching RIO may have given the Saudis the idea.

Both oil—and gas as a by-product—and iron ore are currently in a manipulated and artificial price environment. In both cases, the low cost producers don’t want, and cannot afford, lower prices forever; just for long enough to really hurt the higher cost producers.

The aim is to drive some of them from the market completely, and raise the cost and risk of doing business for the others. Interestedly, because of a weaker Brazilian real, and the lower cost of transportation fuel, Vale is now the world’s lowest cost and highest quality supplier of iron ore.

Painful Losses

Because of losses in their oil related investments, many institutions and hedge funds have been forced to sell off other commodities driving down related market prices across the board.

But just as prices can be manipulated down by low cost producers they can also be manipulated up.

Investing in energy introduces a lot of price volatility into the portfolio. People love upward price volatility, but they really don’t like downward price volatility.

And that’s exactly what we’ve seen a lot of recently. It hasn’t been a pleasant ride. But extreme price volatility in energy investments should be expected.

I think its possible oil will break below $40 in the short term but it’s just as possible we have already seen the bottom at around $45.

Coming Shortage

In my opinion, if the price of oil remains at $50 or lower for any reasonable length of time, we will likely see a supply shortage occur in late 2015 or 2016.

The lower the oil price goes now, the higher the potential price bounce-back in the future.

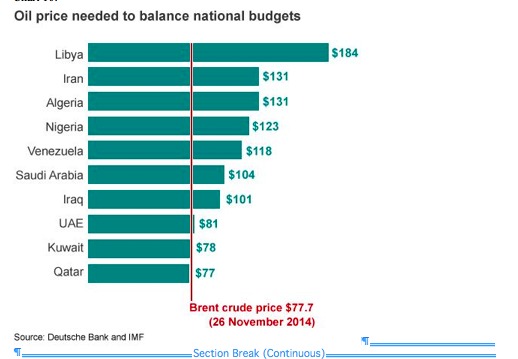

OPEC, and most non-OPEC, countries need much higher oil prices to keep their economies going. John Sfakianakis, an ex-chief economic advisor to Saudi Arabia’s Ministry of Finance, says Saudi Arabia has assumed an $80 a barrel oil price for its 2015 budget.

Jadwa Investment, who follow the Saudi economy closely, calculate the country needs around $93 a barrel to balance their 2015 budget.

Of course Saudi Arabia is more than capable of self-funding any budget shortfall in the short term.

But it’s not just the Saudis who need higher oil prices to balance their budgets. Fitch estimates Russia requires $98 to balance their budget. There are others.

Passing Squall

PWE, XCO, VALE and ESV all have a history of paying dividends during good times and pulling back those dividends during bad times. Right now they are pulling back.

All are conserving cash and doing everything they can to position themselves for survival during this time of low prices. In my opinion this too shall pass.

I believe that when oil and iron ore return to more natural, sustainable pricing, these companies will likely raise their dividends again, providing healthy dividend income, as well as capital gains, to anyone who is a buyer at these currently depressed levels.

Photo Credit: Tsuda via Flickr Creative Commons

The investments discussed are held in client accounts as of March 18, 2015. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable.