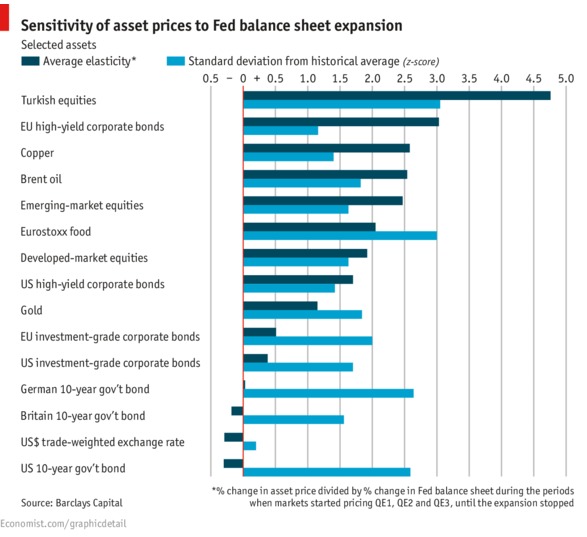

Market volatility is on the rise as investors try to figure out the U.S. Federal Reserve’s next move. The Fed’s various quantitative easing programs and bond buying operations have impacted different asset classes to different degrees. And that will be the case when the central bank starts to wind back its various programs and increase interest rates, which have been edging up of late.

The Economist pulled together a very useful chart that reflects research at Barclays Capital that looks at which asset classes are most sensitive to changes in the size of the Fed’s balance sheet. Barclays came up with its “elasticity” reading, according to the Economist, by dividing the change in the asset prices over periods of QE, by the change in the size of the Fed’s balance sheet.

According to Barclay’s findings, emerging-market equities, which have been getting crushed lately, and European and American high-yield bonds showed high sensitivity to Fed balance sheet changes. Turkish equities may be most at risk. British and German 10-year bonds are among the least sensitive to Fed action.

{kind=link}