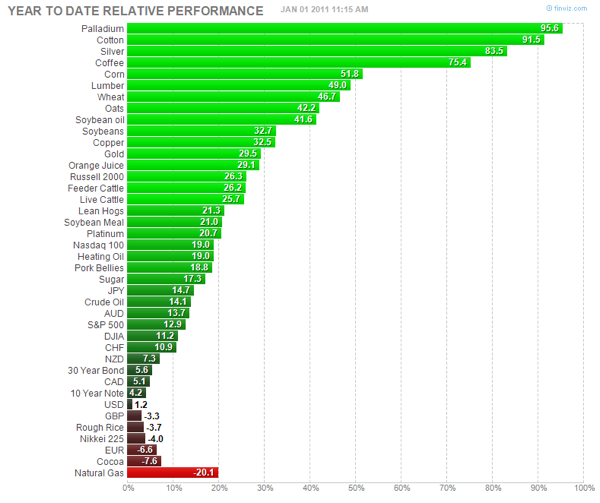

In the Performance with Protection model, manager Leif Eriksen takes a top-down, fundamental approach and generally favors large and mid cap companies. He recently bought the natural gas ETF (UNG), an interesting choice given nat gas’s underperformance in 2010. While most commodities showed considerable strength over the past twelve months and both crude and heating oil outpaced the S&P 500, natural gas was actually at the bottom of the heap in comparison to most of the largest commodities, currencies, treasury debt and U.S. stock market indexes:

Source: Finviz

Paul Ausick surveys the current investment picture in natural gas over on 24/7 Wall Street. As Ausick sees it:

Low [natural gas] prices are a function of booming production from US shale gas fields like the Haynesville, Barnett, and Eagle Ford. Shale gas fields reach peak production very quickly and spit out high daily volumes of gas. Producers have been forced to drill more wells because they are bound by lease agreements that would require them to give up their leased land if they do not develop the lease. The companies drill to maintain their leases, keeping a tight lid on the price of gas. As a result, gas prices are not expected to improve much above $5/thousand cubic feet in 2011.

Leif Eriksen’s model holds 30 positions overall, and his largest positions are in Atheros Communications (ATHR), QUALCOMM (QCOM) and NxStage Medical (NXTM). Here’s the performance of his investable model since inception in March, 2010: