By: Kevin Flanagan, Head of Investment and Fixed Income Strategy

Key Takeaways

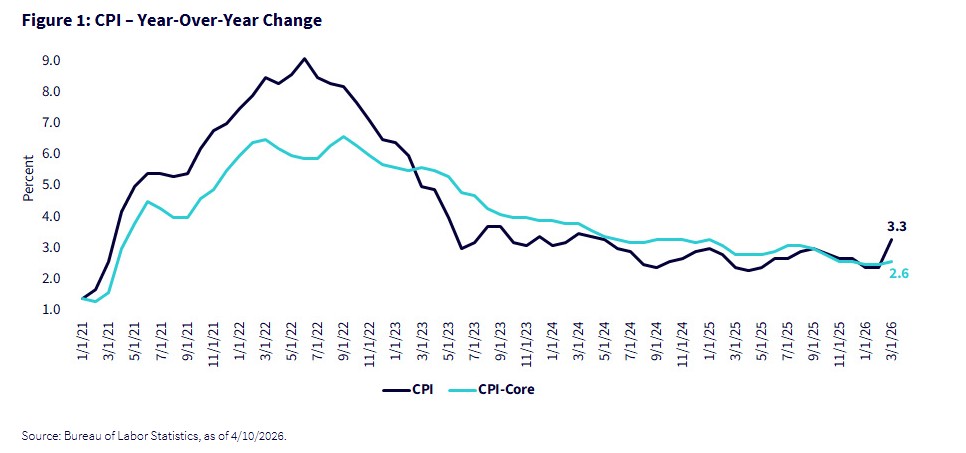

- The March Consumer Price Index (CPI) rose +0.9% month over month—the largest increase since 2022—showing that the war-related surge in gasoline prices is already pushing headline inflation higher and resetting near-term market expectations.

- Core CPI was more contained at +2.6% year over year, but the March reading ended its recent disinflation trend, reminding investors that underlying price pressures remain above the Fed’s comfort zone.

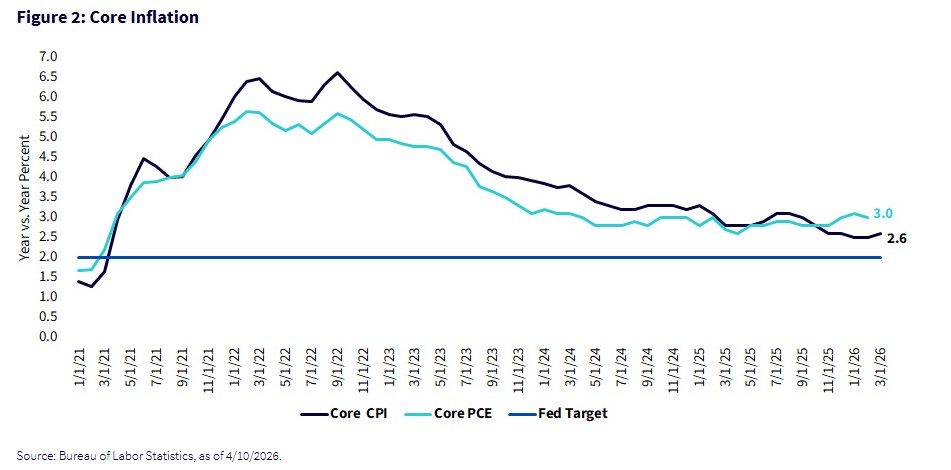

- With core personal consumption expenditures (PCE) already at +3.0% prior to the March energy shock, the Fed appears likely to remain in a holding pattern, looking through energy-driven inflation and leaving rate cuts near the end of this easing cycle.

The Middle East war has replaced tariff-driven inflation concerns with fears of rising energy prices feeding through the economy. On Friday, the Bureau of Labor Statistics (BLS) released its March CPI report, when markets received their first ‘official’ glimpse of how the surge in energy prices has begun to impact the U.S. inflation setting.

The numbers came in close to consensus estimates. But, the elevated headline reading, in particular, marked notable milestones. The monthly gain for overall CPI came in at +0.9%, the largest jump since 2022. Meanwhile, the year-over-year increase registered its highest level in about two years.

This nearly full percentage-point increase in both the monthly and annual readings reflected the war-related surge in crude oil prices, particularly in gasoline prices at the pump. In fact, gasoline prices, as measured in the CPI report, recorded its largest increase since 1967.

Against this backdrop, what about the ‘core’? CPI, excluding food & energy, was far tamer, coming in with a year-over-year gain of +2.6%. However, the March increase interrupted a bout of disinflation for the core gauge and represented the first increase since July.

Extending the core inflation analysis, although core CPI had been returning to a more disinflationary pattern prior to March, it still remained above the Fed’s preference. That brings us to the Fed’s preferred inflation gauge, the core PCE deflator. Unlike core CPI, this measure has actually been trending to the upside on a pre-war basis. Indeed, the year-over-year reading stands at +3.0% as of this writing. This figure is a full percentage point above the Fed’s 2% target. This reading reflects February data, prior to the Middle East war. The March PCE data won’t be released until the end of this month (scheduled for April 30), and it is reasonable to expect not only the headline PCE deflator to jump, but also the core measure remaining above the Fed’s target.

Conclusion

If the Middle East war moves into a more permanent de-escalation phase, or ends, we would expect energy prices to decline meaningfully. However, the scope of disruption has moved higher, and energy prices may not be able to return to pre-war levels in the months immediately ahead.

In our opinion, the Fed will attempt to ‘look through’ the recent surge in energy prices. This development has created a noteworthy shift in inflation fears, but the policymakers, at this point, seem to be operating under the assumption that any elevation in price pressures from higher energy costs will not be a permanent development. Powell & Co. will be loath to use the term ‘transitory’.

Given the war-related uncertainty and the recent jobs and inflation reports, the Fed appears to be in a holding pattern. The most important takeaway is that financial markets will operate in a scenario in which rate cuts are either near or at the end of this easing cycle.

Originally posted on April 15, 2026 on WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/LADYMAYPIX

VIA SHUTTERSTOCK

DISCLOSURES

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Alejandro Saltiel, Andrew Okrongly, Behnood Noei, Bradley Krom, Brendan Loftus, Brian Manby, Christopher Gannatti, David Graichen, Hyun Ku Kang, Jeff Weniger, Jeremy Schwartz, Jonathan Steinberg, Joseph Grogan, Joseph Tenaglia, Kara Dombroski, Kevin Flanagan, Lauren Pfendt, Liqian Ren, Lonnie Jacobs, Matt Wagner, Rick Harper, Ryan Krystopowicz, and Vanya Sharma are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.