By:

Simona M Mocuta, Chief Economist

Amy Le, CFA, Investment Strategist

Krishna Bhimavarapu, Economist

Easing geopolitical tensions and weaker pricing power support a limited inflation impact, while stronger Japanese machinery orders point to resilient growth and a plausible April policy hike.

US: Better Iran news supports our house view

By far the biggest news this week was the Friday announcement of the reopening of the Straits of Hormuz to commercial traffic. It would be unwise to take this as the end of uncertainty, and we do not. Nevertheless, the cumulative retreat in global oil prices since the peak about 10 days ago is already meaningful enough to take us into territory we could consider manageable if indefinitely sustained (WTI prices in the $85 range).

Even if no further reductions occur and prices stabilize here, we would consider this consistent with our house view of an inflation hit that is largely contained to headline measures and limited broader spillover.

One key argument supporting that view—independent of oil prices—is our sense that pricing power today is dramatically weaker than it was back in 2022 during the major inflation spike. Real disposable personal income grew just 1.1% YoY in February; given the March inflation jump, whatever boost from tax refunds will likely be wiped away.

Consumer sentiment has plunged—even as the unemployment rate holds at a seemingly unproblematic level. We link this to weak hiring, which is a significant challenge to accelerating consumer spending.

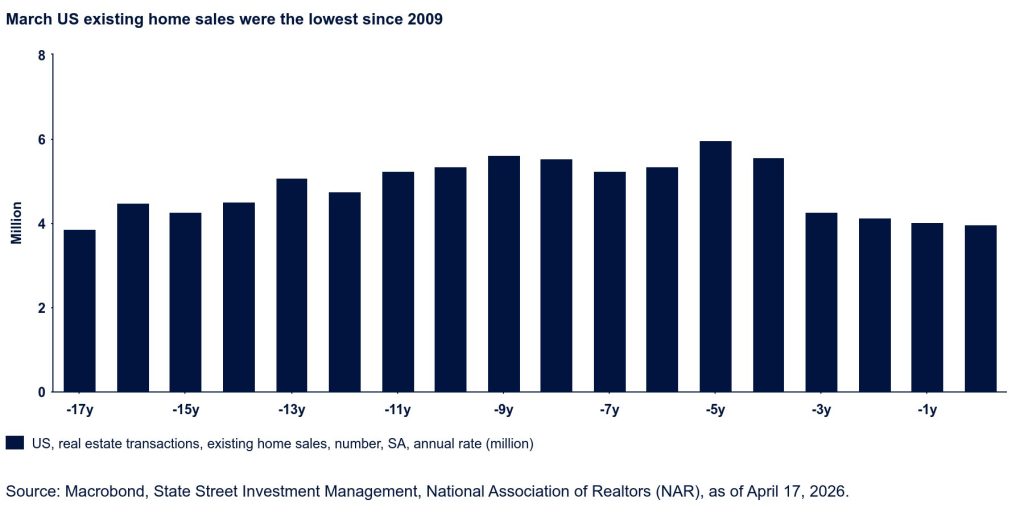

Housing activity reflects consumers’ gloomy mood. At 3.98 million (saar), March existing home sales were the lowest level reported for any March since 2009—a sobering comparison indeed. Homebuilder sentiment dipped further in April to the lowest April reading since 2012 (save for a very brief blip in April 2020).

The consumer is worried about poor employment prospects and poor affordability. The room to push through broad price increases is small in our view, and this should help contain the broader inflationary impact of Middle East hostilities.

Market pricing has shifted once again in favor of a cut late this year (63% for December); we retain our recently adjusted call for two rate cuts (September and December).

BoE: Rate cuts sharply repriced

After an initial oil price spike and market overreaction following the BoE’s March meeting, Governor Bailey called for caution in addressing energy shocks and suggested awaiting more data.

The temporary reopening of the Strait of Hormuz and easing geopolitical tensions led to lower oil prices and revised market expectations, now suggesting less than a full hike from the BoE by year-end. This change has strengthened our view that the BoE policy rate will stay steady throughout 2026.

In our March Quarterly forecast, we expect disruptions to ease in Q2, oil to average $85 per barrel in H2, and inflation to peak at 3.8% in Q3.

The weak UK job market is keeping wage growth low, mitigating secondary inflation risks. Tighter fiscal policy also makes broad energy bill support unlikely. As a result, we expect that the BoE will keep rates unchanged this year unless there are significant energy price fluctuations.

Meanwhile, industrial production rose by 0.5% in February, exceeding market expectations and recovering from prior moderate declines, primarily due to strong growth in the mining and utilities sectors.

This strong performance in industry also contributed to overall economic growth of 0.5% for the same month, also above market expectations.

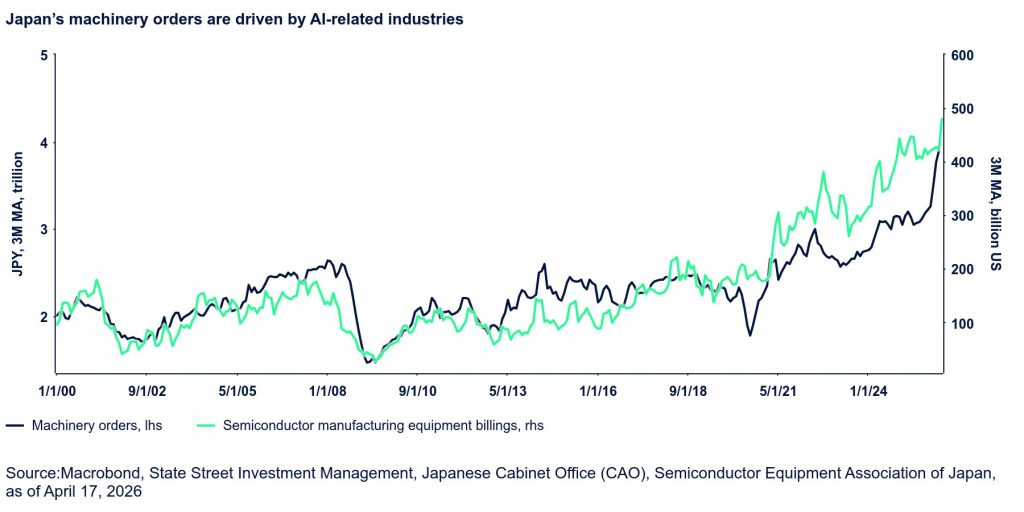

Japan: April hike is still very plausible

Machinery orders in February surprised sharply to the upside, rising 13.6% MoM against a consensus expectation of a 1.1% decline and our own expectation of easing.

On an annual basis, this translated into an eye-catching 24.7% YoY jump. The data reinforce the underlying resilience of the Japanese economy, consistent with our repeated call for stronger nominal growth.

The strength in headline machinery orders was driven primarily by a 30.7% jump in manufacturing orders. Some of this surge likely reflects one-off factors. For instance, nonferrous metal orders surged an extraordinary 419.1% MoM, a magnitude that is unlikely to be repeated consistently. As such, we would caution against extrapolating the monthly pace of growth mechanically.

That said, the broader signal remains constructive. Machinery orders continue to move in lockstep with semiconductor manufacturing equipment orders, an underappreciated but increasingly important strength of the Japanese economy in the 2020s.

What matters here is not short-term volatility in individual order categories, but the persistent comovement between Japan’s capital expenditure cycle and the global semiconductor investment cycle.

This linkage is important because semiconductor activity in Japan operates through a high-multiplier investment channel.

The semiconductor “microeconomy” generates meaningful spillovers into precision machinery, factory automation, robotics, and other capital goods industries where Japan has longstanding competitive advantages.

In effect, semiconductor investment acts as a catalyst that energizes much larger segments of the industrial base.

Concrete examples underscore this mechanism. Tokyo Electron is undertaking capacity expansion with planned capital expenditure of roughly ¥170–240 billion per year at peak through FY2026, focused on etching, deposition, and production facilities.

At the same time, AI-driven demand is lifting capital spending in semiconductor testing, with Advantest expanding capacity to meet rising demand for advanced logic and high-bandwidth memory testing.

In parallel, the Rapidus project represents a large-scale ecosystem buildout, supported by cumulative public–private funding exceeding ¥2.3 trillion for advanced node fabrication and backend capabilities.

Together, these investments are driving demand for ultra-precision machine tools, automated wafer-handling systems, process-control equipment, specialty materials processing, and inspection and metrology tools.

While headline semiconductor capex remains modest relative to total machinery investment at the aggregate level, Japan’s dominance across these upstream and adjacent segments means that semiconductor-led spending propagates through multiple layers of the machinery supply chain.

From a macro perspective, the relevant concept is therefore the capex multiplier embedded in Japan’s industrial ecosystem, rather than the standalone size of semiconductor spending itself.

Originally posted on April 20, 2026 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/ryzhov

VIA SHUTTERSTOCK

DISCLOSURES

Marketing Communication

State Street Global Advisors (SSGA) is now State Street Investment Management. Please go to statestreet.com/investment-management for more information.

State Street Global Advisors Worldwide Entities

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

The views expressed in this material are the views of SSGA Economics Team through the period ended April 17, 2026, and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

{kind=link}