By Steven Levine, Senior Market Analyst, Interactive Brokers

GE Corp’s (GE) myriad of headwinds have generally spurred jitters among its creditors, as the beleaguered industrial conglomerate contends with constructing a sound financial strategy.

The market’s perception of Boston-based GE’s creditworthiness has been waning, amid a lack of clarity in its strategic plans to reduce leverage, as well as amid legal probes, leadership change, and cuts to its credit rating.

![]()

The option-adjusted spread (OAS) on the company’s bonds gapped wider by 8 basis points (bps) on Nov. 13 to more than 245 bps, after announcing it was accelerating its planned separation from integrated oil subsidiary Baker Hughes (BHGE).

Selling Stake

Among the terms of the agreement, GE aims to sell part of its stake in BHGE for about $2.1 billion, as well as commit to a share buyback by BHGE for around $1.5 billion.

Through the transactions, GE expects to maintain its ownership interest in BHGE above 50%, with its remaining stake subject to a 180-day lock-up.

Following the announcement, Gimme Credit analyst Carol Levenson noted that GE “demonstrated a new sense of urgency about raising cash, presumably to pay down debt and/or to bolster its cash reserves and liquidity.”

Impressive Feat

She said that raising roughly $4 billion “in a hurry without sacrificing much except for its BHGE dividends is an impressive feat.”

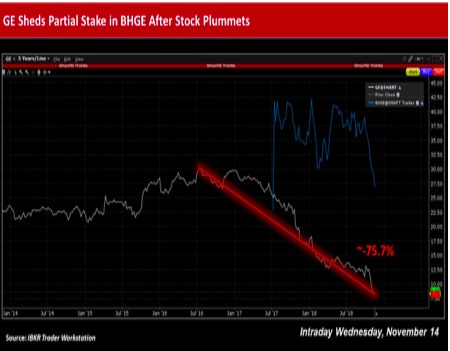

GE’s shares have shed over 75% of their value from their five-year peak of $32.93 set in mid-July 2016, amid other headwinds, including an ongoing probe into its accounting practices by the U.S. Securities and Exchange Commission and Department of Justice.

GE Earnings

Meanwhile, Levenson added that from a bond investor’s perspective, GE’s recently released third quarter earnings report and call were “more noteworthy for what they left out than for what they included.”

She cited, for example, that its management no longer presented a year-end cash target of $15 billion or stated it would reduce industrial net debt by $25 billion by 2020.

Ratings cut

In the three months ended September 30, 2018, GE posted a loss of $2.63 per share, with adjusted EPS down 33% year-on-year to $0.14.

The company recorded a non-cash, pre-tax, goodwill impairment charge of $22 billion, related to GE Power — also subject to SEC and DoJ investigations — and said it plans to cut its quarterly dividend from $0.12 to $0.01 per share in December – enabling annual cash savings of close to $4 billion.

GE also said it intends to restructure its loss-making power business by splitting the unit into two divisions – one for gas products and services, the other for steam, grid solutions, nuclear, and power conversion.

Weaker Performance

The deterioration spurred Moody’s Investors Service to cut the company’s credit rating to ‘Baa1’ from ‘A2’ – a lower echelon of investment-grade, and only three rungs from junk status.

Moody’s said the downgrade was partly based on the adverse impact on GE’s cash flows from the deteriorating performance of its power business, which will be “considerable and could last some time.”

The rating agency attributed the weaker-than-expected performance to not only a “considerable drop in market demand and ensuing heightened competition, but also to GE’s misjudgment of financial prospects and operational missteps.”

GE HealthCare

Moody’s analysts Rene Lipsch, Robert Jankowitz, Mark Wasden and Ana Arsov noted that in addition to weaker earnings, cash flows in GE’s power segment are diminishing “swiftly” due to a decrease in progress collections following a steep decline in equipment orders.

As a result, GE’s post-dividend free cash flow will likely be “very weak” in 2018, even with decent performance at GE Aviation and GE Healthcare.

Moody’s anticipates that a decline in progress collections will continue to hamper cash flows in 2019, as demand for gas turbines will remain “soft,” and GE’s market share has recently come under pressure.

Payment plans

GE CFO Jamie Miller recently said the firm continues to target a leverage ratio of 2.5x net debt-to-EBITDA and expects to make “substantial progress toward this goal in the next few years.”

He said that with respect to excess debt, there will be $7 billion in paydowns, with about $9 billion expected in 2019. He continued that GE Capital also has $16billion worth of long-term debt maturities in 2020.

Overall, Miller added that GE has “significant sources available to delever and derisk the company,” including slashing its dividend, as well as divesting around $20 billion in assets, with an expected close of its distributed power business in the fourth quarter and transportation by early 2019.

Liquidity

Overall, while GE seems to have sufficient liquidity, it continues to need to borrow over $10billion on an intra-quarter basis, compelling it to draw-down on its roughly $40 billion worth of revolvers.

GE at the start of October also shook up its management team, including the installation of new chair and CEO H. Lawrence Culp, who previously helmed Danaher Corp. through it transition from an industrial manufacturer into a science and tech firm from 2001 to 2014. Over that period, Danaher’s market cap and revenue grew five-fold.

However, during GE’s Q3’2018 earnings call, Culp appeared to strike a chord of urgency with respect to raising cash.

Moving Steadily

He said that while the company’s strategy of “derisking and focusing the portfolio is very much intact,” he stressed GE needs to “tend to the balance sheet as quickly as we can. We don’t want to be rushed. We don’t want to be rash, but we need to get after this straight away.”

Culp pointed to the “move on the dividend” as evidence of that intent in action.

Meanwhile, GE’s latest effort to raise cash by offloading a portion of its Baker Hughes stake fell against a backdrop of downbeat sentiment about the energy sector, amid a recent rout in oil prices.

Photo Credit: Jeff Turner via Flickr Creative Commons

The author does not hold any positions in the financial instruments referenced in the materials provided.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR or IBKRAM to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.Certain of the information contained in this article is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. The author believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.