By: Steve Sosnick, Chief Strategist

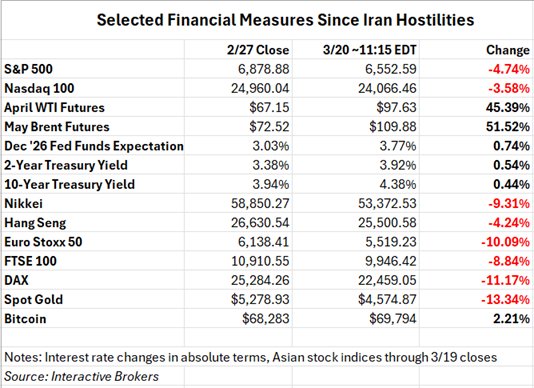

Regular readers should be quite familiar with our ongoing assertion that the stock market reaction to the events in the Persian Gulf is rather subdued, all things considered. In the span of just three weeks, we have seen oil prices spike, other commodities plunge, and interest rates surge as rate cut assumptions have been turned upside down. Nonetheless, in the month of March, US stock indices are down by less than 5%. Their relatively sanguine response might be motivated by a belief either in the “TACO Trade” or a related “Trump Put”. If so, what’s that put’s strike?

Note that US stocks (and bitcoin!) have performed relatively well since the Iran conflict began on Saturday, February 28th, even as we have seen seismic changes in a wide range of factors that traditionally should have greater influences on stock prices than we have seen so far.

The idea of a “Trump Put” is akin to that of the longtime “Fed Put”, where investors assume that the central bank will adopt policies that attempt to stem or reverse adverse market conditions. As we noted in a prior article, I believe that I was present for the birth of the Fed Put. I was a newly minted junior trader at Salomon Brothers during the Crash of 1987, and while Black Monday was bad, things were even worse the next morning. Trading had all but ground to a halt and the system appeared to be on the verge of a meltdown. After a series of tense meetings in an adjacent conference room, we were told to try to clear up any imbalances in stocks we traded. Other firms were given the same orders, and stocks turned around. I learned later that Alan Greenspan’s Fed had arranged to backstop those firms’ purchases. (Much more in this linked piece.)

Because the Fed Put was born in a stock market crisis, stock traders have tended to assume that it is a stock market phenomenon. We have asserted numerous times that it’s an incorrect assumption. The Fed has an explicit duty to maintain the health and stability of the overall financial system, since failing to do so would threaten their dual mandate of stable prices and maximum sustainable employment. If a crisis in the stock market risks metastasizing into a generally systemic problem, as was the case in 1987, then the Fed would and should feel compelled to act. Contrast the difference in the Fed’s response to stock selloffs in 2020 and 2022. The former drop was part of a global economic crisis caused by Covid; the latter fall had few dire consequences outside equity markets and was arguably abetted by Fed that continued to hike rates in order to fight inflation even as stocks fell sharply. It is quite fair to argue that the strike price of the Fed Put cannot be measured in terms of SPX or other stock measures.

Investors, however, have a range of positive experiences from which to base their relative complacency. For starters, dip buying has tended to be a profitable activity, particularly in the post-Covid era. Except for the aforementioned 2022 period, stocks have tended to snap back quickly, reinforcing the notion that “buying the dip” rewards those who do it. A Reuters article published today noted that SPX was higher a month after 42 of the last 59 drawdowns of 5%. Heck, with SPX just 5% from its all-time high, it is quite clear that dip buying has been quite successful over the years – as long as the buyers have sufficiently deep pockets and long time horizons.

Most notably, investors remember what happened 11 months ago in the aftermath of the “Liberation Day” tariff announcement. Stocks plunged but soon recovered all their losses – and then quite a bit more – after the President reversed course on the most egregious parts of that decision. Investors understandably freaked out when a market-friendly President and administration members initially seemed unconcerned about markets’ highly negative reaction. It was only after the President referred to “yippy” bond markets that both stocks and bonds found their footing. While that led many to utilize the acronym “TACO”, for “Trump Always Chickens Out”, I think it is more useful for traders to think of that as the “Trump Put.” He recognized that markets were giving him a huge vote of “no confidence”, so he changed policy in response.

Since then, traders seem to have expected a return of the “Trump Put.” But keep in mind that the mythical put was exercised only when SPX had fallen about 20% from its high. If that is the current strike price, we are likely in for a long, rocky ride.

Remember, we are now down only about one quarter of that 20% drop. Furthermore, bearing in mind that “this time it’s different” is perhaps the most dangerous phrase in investing, this time does seem different. While both events, “Liberation Day”, and the current Iran situation, were triggered by the President’s actions, the former was much more easily reversed. It was an administrative order that had not yet been fully implemented. The current situation is not so easily reversed. For starters, even amidst a wave of military successes, the loser in a military conflict has some say in when it ends. Surrender occurs when the loser gives up, and it is not clear that Iran is yet ready to do that. Also, some of the damage to energy facilities will affect prices for some time, even if the Strait of Hormuz was opened tomorrow.

It behooves all of us to root for a quick but lasting resolution to the current conflict. Stock investors clearly are, as major indices clearly reflect. But if you’re banking on a Trump Put to support your thinking, please be careful about whether the strike is anywhere close to where you think it might be.

Originally posted on March 20, 2026 on Traders’ Insight

PHOTO CREDIT: https://www.shutterstock.com/g/Dilok+Klaisataporn

VIA SHUTTERSTOCK

FOOTNOTES AND SOURCES

https://www.interactivebrokers.com/campus/traders-insight/securities/macro/happy-35th-birthday-fed-put

https://www.interactivebrokers.com/campus/traders-insight/securities/macro/the-fed-put-lives-but-its-never-been-about-stocks

https://www.reuters.com/business/energy-crisis-pulls-stocks-5-below-january-high-path-quick-recovery-remains-2026-03-20

https://www.cnbc.com/2026/03/19/iran-attack-qatar-lng-capacity.html?msockid=1e9ffdd7b3c662a01d01eb51b2506341

DISCLOSURES

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Forecast Contracts Risk

Futures, event contracts and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy visit our Warnings and Disclosures Page.

Disclosure: Precious Metals Risk

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

Disclosure: IBKR Spot Gold

U.S. Spot Gold trading through IB LLC accounts is only available to legal residents of the United States that do not reside in Arizona, Montana, New Hampshire, and Rhode Island.

Disclosure: Digital Assets

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

{kind=link}

{kind=link}